Direct Oral Anticoagulants Market Size, Share, Value and Forecast 2034

Direct Oral Anticoagulants Market By Drug Type (Dabigatran, Rivaroxaban, Edoxaban, Apixaban, and Others), By Application (Atrial Fibrillation, Pulmonary Embolism, Deep Vein Thrombosis, and Others), By Distribution Channel (Hospital Pharmacies, Online Pharmacies, Retail Pharmacies, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2026 - 2034

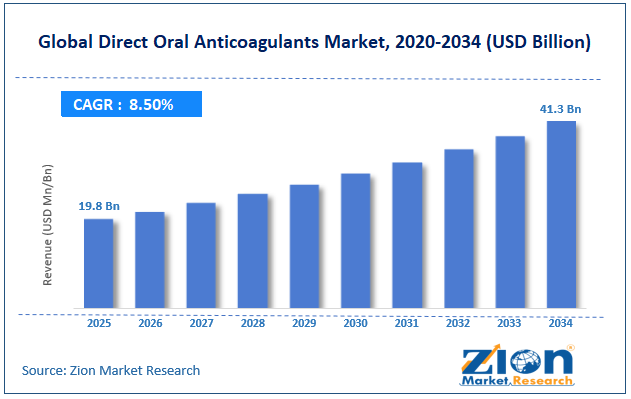

| Market Size in 2025 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 19.8 Billion | USD 41.3 Billion | 8.5% | 2025 |

Direct Oral Anticoagulants Industry Perspective:

What will be the size of the global direct oral anticoagulants market during the forecast period?

The global direct oral anticoagulants market size was worth around USD 19.8 billion in 2025 and is predicted to grow to around USD 41.3 billion by 2034, with a compound annual growth rate (CAGR) of roughly 8.5% between 2026 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global direct oral anticoagulants market is estimated to grow annually at a CAGR of around 8.5% over the forecast period (2026-2034).

- In terms of revenue, the global direct oral anticoagulants market size was valued at around USD 19.8 billion in 2025 and is projected to reach USD 41.3 billion by 2034.

- Healthcare infrastructure improvements in emerging markets are expected to propel the direct oral anticoagulants market over the projected period.

- Based on the drug type, the apixaban segment held the largest market share in 2025 of 33%.

- Based on the application, the atrial fibrillation segment held a prominent market share of 59% in 2025.

- Based on the distribution channel, the hospital pharmacies segment dominates the market.

- Based on region, North America led the market with a revenue share of over 42% in 2025.

Direct Oral Anticoagulants Market: Overview

Direct Oral Anticoagulants (DOACs) are a class of oral anticoagulants that function to prevent and treat blood clots via direct inhibition of one or more than one clotting factors responsible for the formation of the blood clots. The use of conventional anticoagulants such as Warfarin is different from DOACs in a way that they provide predictable anti-coagulation effects, fast onset of action, and no requirement for regular coagulation tests or dosage modification. The mode of action of DOACs involves the inhibition of thrombin (Factor IIa) or Factor Xa, depending on the drug being used. For instance, dabigatran acts by inhibiting thrombin, whereas apixaban, rivaroxaban, and edoxaban inhibit Factor Xa.

Impact of the USA-Israel War on Iran on the Direct Oral Anticoagulants Market

There is a conflict between the U.S. and Israel over Iran that has negatively affected the DOACs market in the short term by disrupting the global pharmaceutical logistics chain, raising shipping and energy costs, and delaying the transport of APIs and drugs. This has led to increases in production and distribution costs, especially for generic DOAC manufacturers and countries that rely on imports. Nevertheless, because DOACs are crucial drugs for managing conditions such as atrial fibrillation and venous thromboembolism, demand for the products has not decreased.

Direct Oral Anticoagulants Market: Dynamics

Growth Drivers

Why does the rising prevalence of atrial fibrillation and venous thromboembolism drive the direct oral anticoagulants market?

The rising incidence of AF and VTE is a key driver of the DOACs market, as these conditions significantly increase the risk of dangerous blood clots; therefore, anticoagulants are needed for long-term treatment. It is advisable to prescribe DOACs for stroke prophylaxis in patients with non-valvular AF and treatment as well as prevention of VTE, which includes DVT and PE. Since the number of patients with such disorders will continue to rise, the target audience in need of anticoagulation will grow, and, accordingly, prescriptions for DOACs will increase, sustaining demand in the market. This is confirmed by the data published by government agencies. For instance, according to the U.S. Centers for Disease Control and Prevention (CDC) – Atrial Fibrillation Facts, 12.1 million people in the country will be diagnosed with atrial fibrillation by 2050; this is due to the increased burden of cardiovascular diseases and the older population in the USA.

Also, according to the report CDC – Venous Thromboembolism Data and Statistics, there are about 900,000 people in the USA suffering from VTE per year; the death toll due to VTE is 60,000–100,000 cases per year. Furthermore, it is stated that many cases of hospital-associated VTE are preventable with adequate treatment by means of anticoagulants.

Restraints

High treatment costs compared with traditional anticoagulants hamper the growth of the direct oral anticoagulants industry

The exorbitant cost of DOACs relative to conventional anticoagulants is a major factor limiting the growth of the direct oral anticoagulant industry, as these medicines are expensive and therefore inaccessible to many people in low-income countries with little or no insurance coverage. Despite numerous benefits, including a standard dosage, minimal interactions with other medicines and food, and no frequent coagulation tests, these medicines are quite expensive compared to conventional anticoagulants such as Warfarin. Thus, acting as a major restraint to the market growth.

Opportunities

How does the growing partnership among key players offer a lucrative opportunity for the direct oral anticoagulants market?

The growing partnership among key market players is expected to create opportunities for the direct oral anticoagulants market. For instance, in September 2025, VarmX, an innovative technology company researching new methods to bypass direct oral anticoagulants targeting factor Xa (FXa DOACs) and inherited coagulation disorders, signed a strategic collaboration agreement with one of the world’s leading biotechnology companies, CSL (ASX:CSL). The purpose of this agreement is to accelerate the development of the company’s lead product, VMX-C001. VMX-C001 is a drug aimed at the restoration of coagulation in case of urgent surgery or massive hemorrhage under FXa DOACs therapy.

In addition, CSL entered into an exclusive option agreement with VarmX’s shareholders to purchase all issued and outstanding stock of the company. According to the terms of the strategic collaboration agreement, CSL will fully finance VarmX’s worldwide clinical phase 3 EquilibriX-S study of VMX-C001 in patients treated with FXa DOACs who require urgent surgery. Also, CSL will finance all late-stage product development, manufacturing, and pre-launch commercial & medical affairs efforts of VarmX.

Challenges

How does the competition from generic products pose a significant challenge to the direct oral anticoagulants market?

The threat of generic competition is a major one for the direct oral anticoagulants industry, as it intensifies price competition and reduces branded companies' revenues. With the patent expiries of dominant DOACs, generics will be launched at much lower prices, motivating hospitals, pharmacies, insurance companies, and government health care programs to opt for more economical options. Generic competition will increase patient access but will bring down the market share and profits of innovator companies. Besides, pricing pressure may limit the financial returns from R&D, thereby hindering market value growth despite rising prescription volumes.

Direct Oral Anticoagulants Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Direct Oral Anticoagulants Market |

| Market Size in 2025 | USD 19.8 Billion |

| Market Forecast in 2034 | USD 41.3 Billion |

| Growth Rate | CAGR of 8.5% |

| Number of Pages | 227 |

| Key Companies Covered | Boehringer Ingelheim GmbH, Johnson & Johnson, Daiichi Sankyo Company, Limited, Pfizer Inc., Bristol-Myers Squibb Company, Gilead Sciences Inc., Bayer AG, Eli Lilly and Company, GlaxoSmithKline plc, AstraZeneca PLC, Sanofi S.A., Takeda Pharmaceutical Company Limited, AbbVie Inc., Teva Pharmaceutical Industries Ltd., Amgen Inc., Roche Holding AG, Novartis AG, Merck & Co. Inc., Biogen Inc., Mylan N.V., and others. |

| Segments Covered | By Drug Type, By Application, By Distribution Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 to 2024 |

| Forecast Year | 2026 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Direct Oral Anticoagulants Market: Segmentation

Drug Type Insights

Why does the apixaban segment hold a prominent position in the direct oral anticoagulants market?

The apixaban segment held the largest market share in 2025 of 33%. This growth in the segment can be attributed to the drug's high efficacy and favorable safety profile, as well as its adoption across various therapeutic uses. As a selective Factor Xa inhibitor, Apixaban is widely used for the prevention of stroke and systemic embolism in non-valvular atrial fibrillation, the treatment and secondary prevention of Deep vein thrombosis (DVT) and Pulmonary embolism (PE), and prophylaxis against thrombosis after major orthopedic surgery. The drug’s lower risk of major and intracranial hemorrhages in comparison to several other anticoagulants has boosted the confidence of physicians in this regard.

Application Insights

How does the atrial fibrillation segment capture the largest share in the direct oral anticoagulants market?

The atrial fibrillation segment held a prominent direct oral anticoagulant market share of 59% in 2025. As AF is the most common type of cardiac arrhythmia, which necessitates prolonged anticoagulation to prevent strokes and systemic embolisms, the rising prevalence of AF, particularly among elderly patients, along with the increasing preference for DOACs over warfarin due to their efficacy, low probability of developing intracranial hemorrhage, and absence of routine monitoring of INR levels, has been adding significantly to the prescription rates.

Additionally, rising prescription volumes in the market are driven by product lifecycle management initiatives and new approvals. For instance, in April 2025, Eliquis (apixaban), marketed by Bristol Myers Squibb and Pfizer, was granted a new indication for use in the pediatric population with recurrent venous thromboembolism, leading to greater utilization and improved overall performance of the DOAC category. Additional investments in access programs and indications will help build physician confidence and drive revenue growth.

Distribution Channel Insights

Does the hospital pharmacies segment capture the largest share in the direct oral anticoagulants market?

The hospital pharmacies segment dominates the direct oral anticoagulants market. This growth in the segment can be attributed to the large number of anticoagulant drugs prescribed and administered under hospital care. Hospitals have been established as the key location for the diagnosis of disorders like atrial fibrillation, Deep vein thrombosis (DVT), and Pulmonary embolism (PE), along with patients undertaking major surgeries of orthopedic and cardiac nature requiring thromboprophylaxis. Hospitals provide DOACs to patients in both inpatient and outpatient settings at discharge.

Regional Insights

Why does North America lead the direct oral anticoagulants market?

North America led the direct oral anticoagulants market with the highest revenue share of over 42% in 2025. The regional growth can be attributed to the prevalence of conditions such as atrial fibrillation and venous thromboembolism, well-established healthcare facilities, good reimbursement policies, and the widespread use of novel anticoagulant products. Revenue growth is also expected to be boosted by ongoing investments by major pharmaceutical players in research, manufacturing, and logistics.

For instance, in May 2025, Bristol Myers Squibb stated that it would spend USD 40 billion over the next five years to build its research, development, technology, and manufacturing capabilities in the US. This investment will increase supply chain efficiency, boost pharmaceutical innovation, and enhance production capabilities for important medications, including heart disease treatments such as the DOAC Apixaban (sold under the trade name Eliquis in collaboration with Pfizer).

Direct Oral Anticoagulants Market: Competitive Analysis

The global direct oral anticoagulants market is dominated by players like:

- Boehringer Ingelheim GmbH

- Johnson & Johnson

- Daiichi Sankyo Company

- Limited

- Pfizer Inc.

- Bristol-Myers Squibb Company

- Gilead Sciences Inc.

- Bayer AG

- Eli Lilly and Company

- GlaxoSmithKline plc

- AstraZeneca PLC

- Sanofi S.A.

- Takeda Pharmaceutical Company Limited

- AbbVie Inc.

- Teva Pharmaceutical Industries Ltd.

- Amgen Inc.

- Roche Holding AG

- Novartis AG

- Merck & Co. Inc.

- Biogen Inc.

- Mylan N.V.

The global direct oral anticoagulants market is segmented as follows:

By Drug Type

- Dabigatran

- Rivaroxaban

- Edoxaban

- Apixaban

- Others

By Application

- Atrial Fibrillation

- Pulmonary Embolism

- Deep Vein Thrombosis

- Others

By Distribution Channel

- Hospital Pharmacies

- Online Pharmacies

- Retail Pharmacies

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Direct Oral Anticoagulants (DOACs) are a class of oral anticoagulants that function to prevent and treat blood clots via direct inhibition of one or more than one clotting factors responsible for the formation of the blood clots.

The direct oral anticoagulants market is primarily driven by the rising prevalence of atrial fibrillation and venous thromboembolism, increasing preference for DOACs over traditional anticoagulants due to their predictable efficacy and reduced need for routine monitoring, and the growing global aging population.

The direct oral anticoagulants market faces several growth challenges, including the high cost of treatment compared with traditional anticoagulants, which limits adoption in cost-sensitive markets, and increasing competition from generic products, which puts pressure on pricing and revenues.

Based on the application, the atrial fibrillation segment is expected to dominate the direct oral anticoagulants market growth during the projected period.

Key emerging trends and innovations in the direct oral anticoagulants market include the expansion of approved indications, increasing use in special patient populations such as pediatric and cancer-associated thrombosis patients, and the growing adoption of personalized anticoagulation strategies.

According to the report, the global direct oral anticoagulants market size was worth around USD 19.8 billion in 2025 and is predicted to grow to around USD 41.3 billion by 2034.

The global direct oral anticoagulants market is expected to grow at a CAGR of 8.5% during the forecast period.

The global direct oral anticoagulants industry growth is expected to be led by North America over the forecast period.

The global direct oral anticoagulants market is dominated by players like Boehringer Ingelheim GmbH, Johnson & Johnson, Daiichi Sankyo Company, Limited, Pfizer Inc., Bristol-Myers Squibb Company, Gilead Sciences, Inc., Bayer AG, Eli Lilly and Company, GlaxoSmithKline plc, AstraZeneca PLC, Sanofi S.A., Takeda Pharmaceutical Company Limited, AbbVie Inc., Teva Pharmaceutical Industries Ltd., Amgen Inc., Roche Holding AG, Novartis AG, Merck & Co., Inc., Biogen Inc., and Mylan N.V., among others.

The direct oral anticoagulants market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients