Pharmaceutical Suppositories Market Size, Share, Value and Forecast 2034

Pharmaceutical Suppositories Market By Formulation Type (Glycerin Suppositories, Polyethylene Glycol Suppositories, Cocoa Butter Suppositories and Gelatin Suppositories), By Therapeutic Application (Pain Management, Hormonal Therapies, Laxatives and Antiemetics), By End User (Hospitals, Pharmacies, Home Care Settings and Clinics), By Distribution Channel (Online Pharmacies, Hospital Pharmacies and Retail Pharmacies) and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 9.5 Billion | USD 13.4 Billion | 3.5% | 2024 |

Pharmaceutical Suppositories Industry Perspective:

What will be the size of the global pharmaceutical suppositories market during the forecast period?

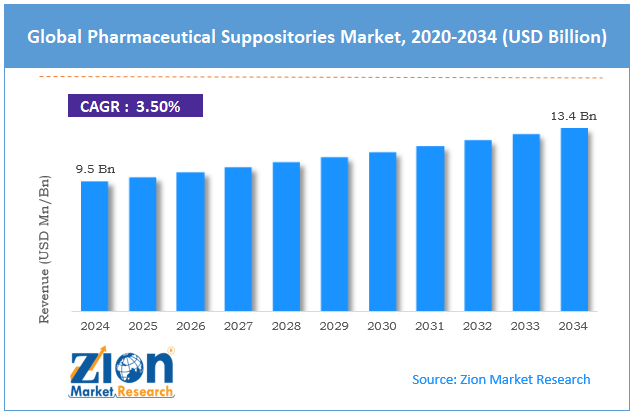

The global pharmaceutical suppositories market size was worth around USD 9.5 billion in 2024 and is predicted to grow to around USD 13.4 billion by 2034 with a compound annual growth rate (CAGR) of roughly 3.5% between 2025 and 2034.

Key Insights

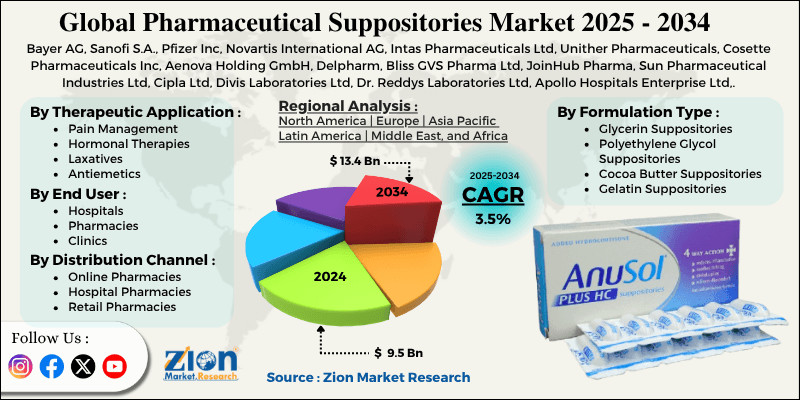

- As per the analysis shared by our research analyst, the global pharmaceutical suppositories market is estimated to grow annually at a CAGR of around 3.5% over the forecast period (2025-2034).

- In terms of revenue, the global pharmaceutical suppositories market size was valued at around USD 9.5 billion in 2024 and is projected to reach USD 13.4 billion by 2034.

- Increasing geriatric population is expected to propel the pharmaceutical suppositories market over the projected period.

- Based on the formulation type, the glycerin suppositories segment captures the largest market share in 2024.

- Based on the therapeutic application, the pain management segment captures the largest revenue share in 2024.

- Based on the end user, the hospitals segment captures the largest revenue share in 2024.

- Based on the distribution channel, the retail pharmacies segment captures the largest revenue share in 2024.

- Based on region, North America accounted for the largest market share of 39% in 2024.

Pharmaceutical Suppositories Market: Overview

The term "pharmaceutical suppositories" refers to solid preparations that are intended to be administered through body cavities, including the rectum, vagina, or urethra. Suppositories disintegrate, dissolve, or soften when exposed to body temperature, releasing the medicinal substance locally or systemically. The main ingredients used for producing suppositories include cocoa butter, glycerinated gelatin, and polyethylene glycol. Suppositories are particularly valuable in situations when patients are unable to take medication orally, owing to vomiting, unconsciousness, dysphagia, or irritation of the stomach lining. By avoiding first-pass metabolism and, in certain instances, the first-pass effect, suppositories allow for higher bioavailability of the drug substance and an accelerated onset of its clinical activity. Suppositories are frequently used to treat several conditions, including constipation, hemorrhoids, infections, pain, and fever.

Impact of the USA-Israel War on Iran on the Pharmaceutical Suppositories Market

The USA-Israel-Iran war, which continues to this day, has greatly influenced the market of pharmaceutical suppositories indirectly through supply chain interruptions in the pharmaceutical industry and cost hikes during manufacturing. The war situation has disrupted key supply routes, including the Strait of Hormuz, through which most of the raw materials, petrochemicals, and APIs transit.

Thus, the manufacturers of pharmaceutical drugs have experienced supply shortages of base substances for making suppositories, such as glycerin and polyethylene glycol, and have also incurred additional shipping expenses due to increased costs associated with shipping and insuring the cargo. According to experts, transportation expenses have increased by 30%.

Pharmaceutical Suppositories Market: Dynamics

Growth Drivers

Why does the rising prevalence of chronic & gastrointestinal disorders drive the pharmaceutical suppositories market?

Several factors are driving the growth of the pharmaceutical suppositories market. Firstly, the prevalence of chronic and GI disorders is increasing, which can be evidenced by the impressive global statistics provided by reputable organizations. According to epidemiological studies and global health statistics, digestive diseases were reported to cause approximately 443.5 million cases in 2019, underscoring the substantial patient population requiring treatment. Secondly, the number of DALYs caused by digestive diseases is close to 88.99 million. This factor makes the prevalence of digestive diseases the most significant, placing these illnesses among the major causes of global disease burden. Thirdly, the prevalence of digestive diseases, such as constipation, IBS, and dyspepsia, affects the vast majority of the world's population at over 40%. Finally, in Europe alone, more than 300 million people suffer from digestive diseases.

Moreover, national data collected by reliable organizations, such as the Centers for Disease Control and Prevention, provide information on millions of annual doctor visits for the treatment of digestive diseases. These facts illustrate the prevalence and severity of the problem, contributing to increased drug consumption. It means there is increased demand for suppositories, as this form of medication is especially effective in treating various diseases, including those affecting the stomach and intestines. In particular, suppositories can serve as an alternative form of treatment in case of digestive issues, including constipation, hemorrhoids, and inflammatory bowel diseases, as well as other conditions characterized by high levels of irritation of the gastrointestinal tract. Suppositories are an alternative drug-delivery system, allowing patients to obtain the required dose in a relatively short time without causing discomfort to others.

Restraints

Patient discomfort & social stigma hindering the pharmaceutical suppositories industry growth

It has also been highlighted that patient discomfort and social stigma pose significant barriers to the development of the pharmaceutical suppositories market. While the drugs are very effective, they are seen as being inconvenient and embarrassing due to the method through which they are used, particularly those used rectally. Patients are reluctant to use them, which means they are unlikely to follow the prescribed regimen. This issue is most pronounced in cultures that avoid discussing such matters, resulting in very low market penetration rates. As a result, most patients opt for other methods of administration that are socially acceptable, such as taking the drugs orally as pills. Despite their efficacy, the drugs' tendency to leak when inserted makes patients wary of using them.

Opportunities

Why does the rising demand for alternative drug delivery systems offer a lucrative opportunity for the pharmaceutical suppositories market?

There is no doubt that the increasing need for alternative methods of drug delivery offers a strong growth opportunity for the pharmaceutical suppositories market, but this is true only in specific cases where suppositories are superior to traditional methods of delivering medicine. There are several factors driving interest in developing this product, all of which are associated with the drawbacks of other drug-delivery methods. First, there is a problem related to gastrointestinal limitations and the impact of the first-pass effect on the efficiency of medication. The first-pass effect is a common term used by scientists to describe the phenomenon of reduced bioavailability of orally administered medicines because they are metabolized before entering the bloodstream.

Therefore, suppositories, particularly rectal suppositories, could be an effective way to increase drug delivery and the speed of achieving maximum efficacy in cases when oral delivery is difficult and ineffective. Second, there are more people who have problems with taking oral medications due to vomiting, serious gastrointestinal diseases, surgical interventions, or other reasons connected with problems with oral administration.

Thus, suppositories could become an alternative drug delivery system to help these patients. Such situations usually occur among children and elderly people. Finally, nowadays, the healthcare field is focused on developing drug delivery systems that are less invasive, more convenient for patients, and more patient-centered. Suppositories can be considered one such means, even though they are less preferred by patients.

Challenges

Why does the preference for oral drug delivery pose a significant challenge to the pharmaceutical suppositories market?

One key challenge for the pharmaceutical suppositories market is the prevalence of oral drug delivery systems, which affects patients, prescribing physicians, and overall demand. Tablets, capsules, and other oral dosage forms are regarded as the most convenient, non-invasive, and familiar options for drug administration. The ease with which patients consume drugs using these dosage forms, along with the reduced risk of complications associated with their use, makes them more appealing than suppositories that are administered rectally or vaginally, resulting in a higher tendency to follow the treatment regimen.

Hence, most patients will choose oral dosage forms over suppositories, even though the latter have several advantages. Prescribing physicians prefer oral drugs not only for their simplicity but also because they are less likely to be misused by patients. This is especially true in cases where there is no clear instruction regarding how the drug must be taken and stored. Finally, pharmaceutical firms prefer to develop oral dosage forms because of their high commercial value, ease of manufacturing, and wide applicability.

Pharmaceutical Suppositories Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Pharmaceutical Suppositories Market |

| Market Size in 2024 | USD 9.5 Billion |

| Market Forecast in 2034 | USD 13.4 Billion |

| Growth Rate | CAGR of 3.5% |

| Number of Pages | 229 |

| Key Companies Covered | Bayer AG, Sanofi S.A., Pfizer Inc, Novartis International AG, Intas Pharmaceuticals Ltd, Unither Pharmaceuticals, Cosette Pharmaceuticals Inc, Aenova Holding GmbH, Delpharm, Bliss GVS Pharma Ltd, JoinHub Pharma, Sun Pharmaceutical Industries Ltd, Cipla Ltd, Divis Laboratories Ltd, Dr. Reddys Laboratories Ltd, Apollo Hospitals Enterprise Ltd, Torrent Pharmaceuticals Ltd, Chiesi Farmaceutici, CSPC Pharmaceutical Group, Esteve Química, Humanwell Healthcare (Group) Co, Jiangsu Hengrui Pharmaceutical, GlaxoSmithKline (GSK), Nordic Pharma Group, Phoenix Pharma Group, DocMorris, Medpex, AstraZeneca, Mylan, Abbott Laboratories, Zentiva, and others. |

| Segments Covered | By Formulation Type, By Therapeutic Application, By End User, By Distribution Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Pharmaceutical Suppositories Market: Segmentation

Formulation Type Insights

Why does the glycerin suppositories dominate the pharmaceutical suppositories market?

The glycerin suppositories segment captures the largest market share in 2024. The major driver of growth is its extensive use as a safe, efficient, and quick-acting remedy for constipation. As glycerin suppositories are absorbed via osmosis, which draws water into the bowels, softening the feces and facilitating defecation, they are highly suitable for children, the elderly, and post-operative patients. With the growing prevalence of constipation around the globe, linked to sedentary lifestyles, improper eating habits, and the increasing population of elderly people, the demand for OTC laxatives has risen considerably.

Therapeutic Application Insights

Do the pain management capture the largest market share in the pharmaceutical suppositories market?

The pain management segment captures the largest revenue share in 2024. This expansion is driven by the rising need for efficient pain relief treatments when the consumption of drugs orally is impossible. Suppositories containing analgesic medicines, such as NSAIDS and opioids, have been widely used for the management of pain after surgery, pain due to cancers, and acute pain when patients are not able to swallow or suffer from vomiting. The advantage of suppositories being able to bypass the first pass effect makes them highly efficacious and more effective compared to some oral drugs.

End User Insights

Why do hospitals capture the largest market share in the pharmaceutical suppositories market?

The hospitals segment captures the largest revenue share in 2024. The demand arises from the high number of inpatients requiring treatment, as well as the requirement for dependable drug delivery in the context of acute care and post-surgery. Patients admitted to hospitals are often unable to consume oral medication because of surgery, being unconscious, vomiting, or digestive problems, so suppositories offer an effective solution when administering analgesic, anti-fever, and antiemetic drugs. The speed of absorption and the partial circumvention of the first-pass effect further increase their effectiveness.

Distribution Channel Insights

Do retail pharmacies capture a significant revenue share in the pharmaceutical suppositories market?

The retail pharmacies segment captures the largest revenue share in 2024. This rise is mostly attributed to the increased availability of OTC products and the growing tendency among consumers to self-medicate. For instance, common illnesses like constipation, hemorrhoids, fever, and even some infections can be treated by using available suppository medicines bought directly from pharmacies. Some of the most commonly sought-after products include those containing glycerin and analgesics. The pharmacies act as convenient sources that ensure availability at once.

Regional Insights

Why does North America lead the pharmaceutical suppositories market?

North America accounted for the largest market share of 39% in 2024. This growth is due to the region's highly developed healthcare infrastructure, high disease incidence, and the use of alternative modes of drug administration. In North America, the United States and Canada are the main drivers of growth in this market, as they have well-developed hospital systems, high healthcare spending, and advanced formulations of medicines. The increased cases of gastrointestinal diseases, chronic pain syndromes, and an elderly population, which often experiences problems taking oral medications, are leading to an increase in demand for suppositories.

Also, good awareness of the advantages of alternative modes of drug delivery, such as improved bioavailability due to the avoidance of the first-pass effect, contributes to market growth. It should also be noted that there are highly developed retail pharmacies and over-the-counter drugs that are used to treat constipation and hemorrhoids.

Pharmaceutical Suppositories Market: Competitive Analysis

The global pharmaceutical suppositories market is dominated by players like:

- Bayer AG

- Sanofi S.A.

- Pfizer Inc

- Novartis International AG

- Intas Pharmaceuticals Ltd

- Unither Pharmaceuticals

- Cosette Pharmaceuticals Inc

- Aenova Holding GmbH

- Delpharm

- Bliss GVS Pharma Ltd

- JoinHub Pharma

- Sun Pharmaceutical Industries Ltd

- Cipla Ltd

- Divis Laboratories Ltd

- Dr. Reddys Laboratories Ltd

- Apollo Hospitals Enterprise Ltd

- Torrent Pharmaceuticals Ltd

- Chiesi Farmaceutici

- CSPC Pharmaceutical Group

- Esteve Química

- Humanwell Healthcare (Group) Co

- Jiangsu Hengrui Pharmaceutical

- GlaxoSmithKline (GSK)

- Nordic Pharma Group

- Phoenix Pharma Group

- DocMorris

- Medpex

- AstraZeneca

- Mylan

- Abbott Laboratories

- Zentiva

The global pharmaceutical suppositories market is segmented as follows:

By Formulation Type

- Glycerin Suppositories

- Polyethylene Glycol Suppositories

- Cocoa Butter Suppositories

- Gelatin Suppositories

By Therapeutic Application

- Pain Management

- Hormonal Therapies

- Laxatives

- Antiemetics

By End User

- Hospitals

- Pharmacies

- Home Care Settings

- Clinics

By Distribution Channel

- Online Pharmacies

- Hospital Pharmacies

- Retail Pharmacies

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

The term "pharmaceutical suppositories" refers to solid preparations that are intended to be administered through body cavities, including the rectum, vagina, or urethra. Suppositories disintegrate, dissolve, or soften when exposed to body temperature, releasing the medicinal substance locally or systemically. The main ingredients used for producing suppositories include cocoa butter, glycerinated gelatin, and polyethylene glycol.

Key growth drivers for the pharmaceutical suppositories market include the rising prevalence of gastrointestinal and chronic disorders, increasing demand for alternative drug delivery systems, and a growing geriatric population requiring non-oral medication options.

Major challenges restraining the growth of the pharmaceutical suppositories market include low patient acceptance due to discomfort and social stigma, strong preference for oral drug delivery, stability and storage issues (especially in warm climates), formulation and dosing limitations, and increasing competition from more convenient advanced drug delivery systems.

Based on the end user, the hospitals segment is expected to dominate the pharmaceutical suppositories market growth during the projected period.

One of the most notable trends is the integration of advanced technologies such as artificial intelligence (AI) in drug development and formulation design, which is accelerating R&D and enabling the creation of more effective suppository products.

According to the report, the global pharmaceutical suppositories market size was worth around USD 9.5 billion in 2024 and is predicted to grow to around USD 13.4 billion by 2034.

The global pharmaceutical suppositories market is expected to grow at a CAGR of 3.5% during the forecast period.

The global pharmaceutical suppositories industry growth is expected to be led by North America over the forecast period.

The global pharmaceutical suppositories market is dominated by players like Bayer AG, Sanofi S.A., Pfizer Inc, Novartis International AG, Intas Pharmaceuticals Ltd, Unither Pharmaceuticals, Cosette Pharmaceuticals Inc, Aenova Holding GmbH, Delpharm, Bliss GVS Pharma Ltd, JoinHub Pharma, Sun Pharmaceutical Industries Ltd, Cipla Ltd, Divis Laboratories Ltd, Dr. Reddys Laboratories Ltd, Apollo Hospitals Enterprise Ltd, Torrent Pharmaceuticals Ltd, Chiesi Farmaceutici, CSPC Pharmaceutical Group, Esteve Química, Humanwell Healthcare (Group) Co, Jiangsu Hengrui Pharmaceutical, GlaxoSmithKline (GSK), Nordic Pharma Group, Phoenix Pharma Group, DocMorris, Medpex, AstraZeneca, Mylan, Abbott Laboratories and Zentiva among others.

The market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients