Personalised Medicine Market Size, Share, Trends & Forecast 2026–2034

Global Personalised Medicine Market by Therapy Area (Oncology, Cardiology, Neurology, Rare Diseases, Others), by Technology (Genomics & Proteomics, Companion Diagnostics, Precision Diagnostics, Digital Health & AI, Others), by Drug Type (Small Molecules, Biologics, Cell & Gene Therapies, Others), by End User (Hospitals & Clinics, Diagnostic Laboratories, Research Institutes, Pharmaceutical Companies, Others), and by Region — Global Market Size, Share, Growth, Trends, Forecast 2026–2034.-

| Market Size in 2025 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 14,820 Million | USD 94,680 Million | 22.7% | 2025 |

Personalised Medicine Industry Perspective:

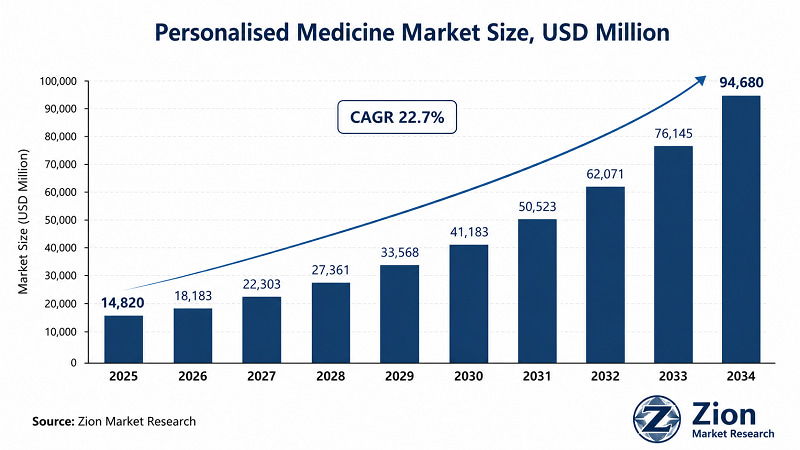

- At USD 14,820 Mn in 2025 and on trajectory to reach USD 94,680 Mn by 2034, the 22.7% CAGR of the Global Personalised Medicine market reflects more than growth — it reflects the structural obsolescence of population-average treatment protocols.

- The market is driven by simultaneous advances across genomics infrastructure, regulatory companion diagnostic frameworks, and the commercial maturation of cell and gene therapy platforms.

- What distinguishes this expansion from prior healthcare technology cycles is its depth: personalised medicine touches every clinical workflow from initial diagnostic screening to long-term therapeutic management.

Personalised Medicine Market: Overview

- Personalised Medicine encompasses the diagnostic platforms, targeted therapeutics, precision decision-support tools, and integrated data infrastructure that enable treatment individualisation based on a patient's genetic, molecular, proteomic, and clinical profile. The market spans next-generation sequencing equipment and bioinformatics software at the genomics layer through to cell-engineered therapeutic products at the clinical delivery layer — making it one of the most vertically integrated growth markets in healthcare.

- The value chain operates across three structural tiers. Foundational providers — including Illumina, Thermo Fisher Scientific, and Pacific Biosciences — supply the sequencing hardware, reagents, and bioinformatics infrastructure that underpin all downstream applications. Specialist developers — such as Foundation Medicine, QIAGEN, and Guardant Health — build the disease-specific genomic profiling and liquid biopsy platforms that translate sequencing data into clinical decision content. Application-layer specialists — including Roche's oncology diagnostics division, Novartis's CAR-T manufacturing platform, and Blueprint Medicines — deliver the finished therapeutic and companion diagnostic products to hospital and laboratory end users.

- For procurement and investment decision-makers, the distinction that matters is not whether Personalised Medicine will grow — that question is settled — but which segments, geographies, and deployment models will capture disproportionate value within that growth. This report provides sub-segment level data, country-level forecasts, and competitive positioning analysis across five segmentation dimensions and 35+ geographies.

Key Insights

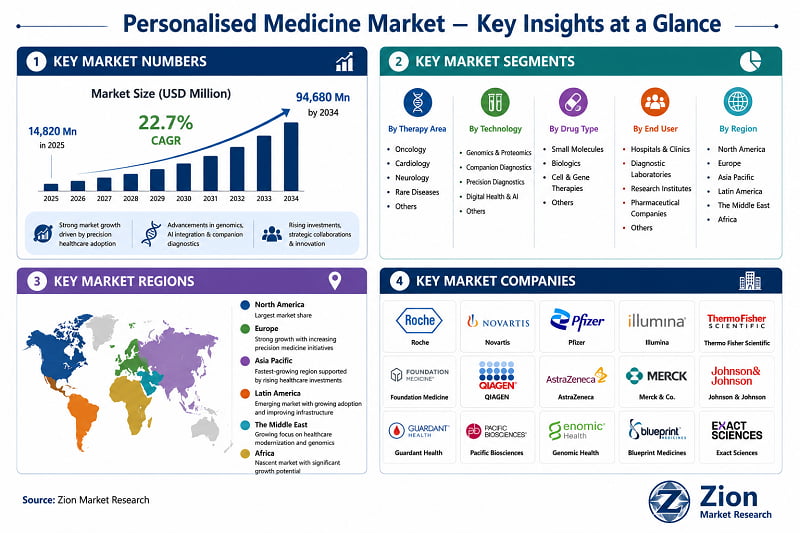

- The Global Personalised Medicine market is forecast to expand at a 22.7% CAGR from USD 14,820 Mn in 2025 to USD 94,680 Mn by 2034 (Zion Market Research).

- Oncology is the dominant therapy area sub-segment, holding approximately 38% of global market revenue in 2025, driven by companion diagnostic density in solid tumour and haematological malignancy indications.

- Cell & Gene Therapies is the fastest-growing drug type sub-segment, projected to register the highest CAGR within the drug type dimension through 2034, fuelled by expanding CAR-T indications and next-generation gene editing approvals.

- Genomics & Proteomics is the dominant technology sub-segment, anchoring the foundational data layer for all downstream clinical applications including precision diagnostics and companion diagnostic development.

- Hospitals & Clinics is the dominant end-user segment, accounting for the largest share of market revenue as integrated genomic oncology programmes become standard clinical infrastructure at major health systems.

- North America leads by regional revenue share, with the U.S. contributing the majority of global companion diagnostic approvals and serving as the primary commercial launch market for precision therapeutics.

- Asia Pacific registers the highest regional CAGR through 2034, driven by China's national precision medicine programme, India's diagnostic sector expansion, and South Korea's genomics infrastructure investment.

- The competitive landscape is consolidating around pharma-diagnostics bundling strategies, with Roche, Novartis, and AstraZeneca leading the integration of companion diagnostics directly into therapeutic label submissions.

- By 2034, cell and gene therapies — currently the smallest drug type sub-segment by volume — are projected to represent the largest share of per-patient revenue within the Personalised Medicine market, driven by ultra-premium pricing models and expanding label coverage.

Why Choose the Zion Market Research's Personalised Medicine Market Report?

Decision-makers comparing market intelligence reports on Personalised Medicine will find the Zion Market Research's report differentiated on the following dimensions.

|

Dimension |

Zion Market Research Report |

Industry Average |

|

Report Pages |

300+ |

~120 pages |

|

Forecast Horizon |

9 years (2026–2034) |

7 years |

|

Segmentation Dimensions |

5 dimensions |

4–5 dimensions |

|

Historical Data |

6 years (2019–2025) |

4–5 years |

|

Country Coverage |

35+ countries |

15–18 countries |

|

Companies Profiled |

15 companies |

10 companies |

|

DROC Framework |

Full (Drivers, Restraints, Opportunities, Challenges) |

Drivers only |

**For custom scope — additional segments, specific geographies, or extended forecast periods — contact sales@zionmarketresearch.com

Personalised Medicine: Dynamics (Drivers, Restraints, Opportunities, Challenges)

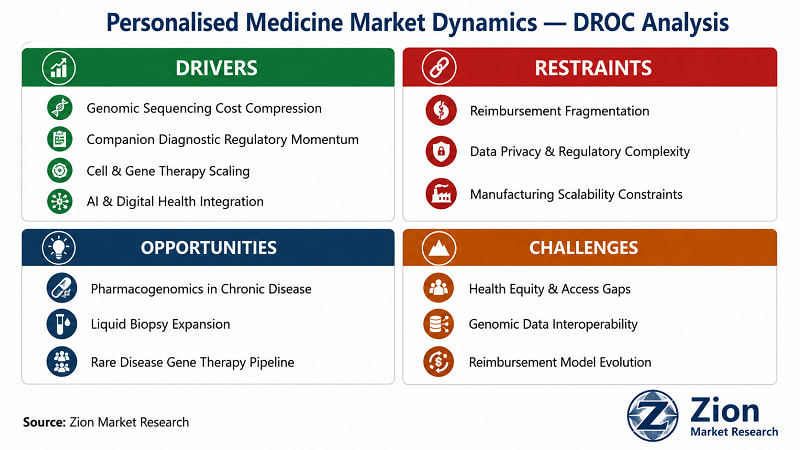

What Is Driving the Personalised Medicine Market?

- Genomic Sequencing Cost Compression:

Falling sequencing costs are the single most important supply-side driver in the market. The cost of whole-genome sequencing has declined from over USD 1 million in 2007 to below USD 200 in 2024 — a 99.98% reduction in 17 years. This crosses the threshold at which population-level genomic screening becomes economically viable for both public health systems and private payers. Illumina deployed its DRAGEN bioinformatics platform across major U.S. academic medical centres in 2023–2024, enabling clinical-grade genomic variant interpretation at scale. The regulatory tailwind amplifies this: FDA's updated guidance on next-generation sequencing-based companion diagnostics (2022) has streamlined the approval pathway, reducing time-to-market for genomic diagnostic products by an estimated 30% versus pre-guidance timelines. For procurement directors, the near-term implication is clear: sequencing infrastructure is transitioning from research capital expenditure to operational clinical infrastructure.

- Companion Diagnostic Regulatory Momentum:

FDA companion diagnostic approvals have passed 50 — and the pipeline is accelerating. Each approval creates a locked-in therapeutic-diagnostic revenue bundle that raises competitive barriers for new market entrants and generates durable recurring revenue for diagnostic platform holders. Roche's VENTANA PD-L1 companion diagnostic — co-approved with atezolizumab for non-small cell lung cancer — exemplifies the commercial architecture: a diagnostic product that is clinically required for therapeutic access, generating a captive recurring revenue stream tied directly to drug sales. The FDA's Project Optimus initiative (2022 onward) is further accelerating dose-optimisation studies that require companion biomarker data, expanding the addressable market for precision diagnostics into earlier development-stage therapeutic programmes.

- Cell & Gene Therapy Commercial Maturation:

CAR-T and gene therapy platforms are crossing the commercial viability threshold. Novartis's Kymriah (tisagenlecleucel) — the first approved CAR-T therapy — generated revenues exceeding USD 500 Mn annually by 2023, demonstrating that ultra-personalised biologics can reach institutional-scale commercial returns. The approval pipeline is expanding beyond haematological malignancies into solid tumours, with over 30 IND-stage programmes targeting solid tumour CAR-T constructs in 2024–2025. Simultaneously, manufacturing scalability — the primary supply-side constraint — is being addressed through automated bioreactor systems and decentralised point-of-care manufacturing models. For healthcare investors, cell and gene therapies represent the highest-volatility, highest-return sub-segment within the Personalised Medicine market TAM.

- AI and Digital Health Platform Integration:

AI-driven clinical decision support is converting genomic data into actionable treatment protocols at scale. Google Health's DeepMind has demonstrated AI diagnostic accuracy exceeding specialist-level performance in retinal disease detection using genomic and imaging data fusion — a deployment model that major academic medical centres are now replicating across oncology, cardiology, and rare disease pathways. The U.S. FDA approved over 500 AI/ML-based medical devices by end-2024, with precision medicine applications representing the fastest-growing category. This integration of digital health platforms with genomic data infrastructure is creating a new category of clinical decision support that commands premium pricing and generates recurring subscription revenue — fundamentally changing the financial model for health system technology procurement.

"Personalised medicine is not a distant vision — it is the present reality of oncology care. Our genomic profiling work has shifted from research protocols to standard of care in less than five years."

— Dr. José Baselga, former Chief Medical Officer, AstraZeneca

(Source: AACR Annual Meeting Proceedings, April 2022)

What Is Restraining the Personalised Medicine Market?

- Reimbursement Fragmentation Across Major Markets:

Inconsistent payer coverage for genomic diagnostics is the primary demand-side restraint globally. Outside the U.S. — where CMS has progressively expanded coverage for specific genomic tests — the majority of European markets, Japan, and most emerging economies lack standardised reimbursement pathways for whole-genome sequencing or liquid biopsy diagnostics. Germany's GBA benefit assessment framework has approved coverage for select companion diagnostic tests in oncology but provides no pathway for broad genomic profiling — creating a two-tier access environment. This restraint is felt most acutely in Asia Pacific's developing markets and Latin America, where out-of-pocket costs for genomic diagnostics remain prohibitive for the majority of patients. The timeline for reimbursement harmonisation extends beyond 2028 in most non-U.S. markets, creating a structural near-term ceiling on commercial volume outside North America.

- Data Privacy and Biosecurity Regulatory Complexity:

Genomic data sits at the intersection of healthcare privacy law, national security regulation, and intellectual property rights. GDPR's stringent requirements for cross-border transfer of genetic data have forced clinical genomics platforms operating in Europe to build separate data processing infrastructure for EU markets — adding cost and complexity to pan-European commercial deployments. China's Human Genetic Resources Administration (HGRAC) requires government approval for any export of Chinese citizens' genomic data, effectively partitioning the Chinese precision medicine market from global data networks. For multinational players building centralised genomic data platforms, these jurisdiction-specific requirements generate compliance costs that disadvantage market entry into high-growth geographies.

- Manufacturing Scalability Constraints for Cell & Gene Therapies:

The manufacturing infrastructure for personalised cell and gene therapies cannot yet match clinical demand growth. CAR-T manufacturing requires a patient-specific vein-to-vein process — from cell collection to infusion — that takes 17–22 days per patient and requires GMP-certified infrastructure that does not yet exist at sufficient scale globally outside the U.S. and Europe. GMP facility construction timelines of 3–5 years and capital requirements exceeding USD 100 Mn per facility create supply-side constraints that will persist through 2027. Outside North America and Western Europe, this restraint is near-absolute, limiting access to CAR-T therapies in Asia Pacific, Latin America, and The Middle East despite strong clinical demand.

"The challenge we face isn't scientific — it's operational. Integrating genomic data into our clinical workflows required a complete rethink of our EHR architecture and clinician training programmes."

— CIO, Major U.S. Academic Medical Center (paraphrased from Health Affairs interview, 2023)

(Source: Health Affairs, Buyer-Side Institution Perspective, November 2023)

What Opportunities Exist in the Personalised Medicine Market?

- Pharmacogenomics Integration in Chronic Disease Management:

Chronic disease — not oncology — represents the largest untapped opportunity in the Personalised Medicine market. Cardiovascular disease, diabetes, and psychiatric conditions collectively represent a larger patient population than all oncology indications combined. Pharmacogenomics — the use of genomic data to individualise drug selection and dosing for chronic conditions — is at an early commercial stage. The FDA has issued pharmacogenomics biomarker labelling for over 200 drugs to date, yet adoption in primary care and chronic disease management remains below 10% globally. The TAM expansion opportunity for genomics platform providers and digital health companies entering chronic disease pharmacogenomics is structurally larger than the oncology market they currently serve.

- Liquid Biopsy Market Expansion Beyond Oncology:

Liquid biopsy's clinical utility is extending well beyond its cancer detection origins. Circulating cell-free DNA analysis is demonstrating clinical validity in prenatal screening (NIPT), organ transplant rejection monitoring, neurodegenerative disease early detection, and cardiovascular risk stratification. Guardant Health's SHIELD test — approved by FDA in July 2024 for colorectal cancer screening — demonstrated the liquid biopsy platform's ability to penetrate mass-market screening indications, not just late-stage diagnostic applications. The total addressable market for liquid biopsy in non-oncology applications is estimated to exceed the current oncology liquid biopsy TAM by 2030, creating a multi-vertical expansion opportunity for platform holders.

- Rare Disease Gene Therapy Pipeline Monetisation:

The rare disease gene therapy pipeline represents the most concentrated value creation opportunity in the near-term Personalised Medicine market. Over 3,500 rare diseases currently lack approved treatments, and gene therapy is the only therapeutic modality that offers disease-modifying — or potentially curative — outcomes for monogenic rare conditions. The FDA's Accelerated Approval pathway and EMA's Conditional Marketing Authorisation are designed precisely for this pipeline: rapid commercial pathways for ultra-rare indications where clinical trial populations are inherently small. With AstraZeneca, Sanofi, and Pfizer all expanding rare disease gene therapy programmes, the pipeline monetisation opportunity extends the Personalised Medicine market TAM well beyond oncology through 2034.

- AI-Powered Multi-Omic Data Platforms:

The integration of genomic, proteomic, metabolomic, and clinical data into unified AI diagnostic platforms is creating a new category of clinical intelligence product. Multi-omic data platforms — combining DNA sequencing with protein expression, metabolite profiling, and longitudinal clinical records — can identify treatment response predictors that single-omics approaches miss. Tempus AI's platform, which aggregates clinical and molecular data from over 7 million patient records, represents the commercial architecture for this category. For health systems, multi-omic platforms offer a pathway to measurable improvement in treatment outcome rates — a reimbursement argument that is gaining traction with payers as outcome-based contracting models expand.

What Challenges Does the Personalised Medicine Market Face?

- Health Equity and Genomic Access Disparities:

Personalised medicine's benefits are disproportionately captured by patients in high-income countries and majority populations. Genomic reference databases — the foundation of variant interpretation — are dominated by individuals of European ancestry, limiting diagnostic accuracy for patients from African, Asian, and Latin American populations. This is not merely an ethical issue: it is a scientific accuracy problem that systematically produces higher variant-of-uncertain-significance (VUS) rates in underrepresented populations, reducing diagnostic utility. The commercial consequence is a market that cannot achieve its full global TAM without addressing data diversity — and the timeline for meaningful reference database diversification extends beyond 2030.

- Genomic Data Interoperability and Clinical Integration:

Genomic data does not flow seamlessly into existing clinical workflows — and this friction limits adoption velocity. Electronic health record systems were not designed to store, interpret, or display genomic variant data. Integration projects at major health systems — including Geisinger Health System's MyCode programme and Kaiser Permanente's Research Bank — have required multi-year custom EHR development projects costing tens of millions of dollars. Until genomic data interoperability standards (HL7 FHIR Genomics, GA4GH APIs) achieve broad EHR adoption, the productivity gap between genomic data generation and clinical use will constrain market growth in the institutional end-user segment.

- Reimbursement Model Evolution Lag:

Healthcare reimbursement models have not yet adapted to the one-time-treatment, long-term-value economics of gene therapy. A CAR-T therapy costing USD 400,000–USD 500,000 per patient — potentially curative — generates long-term savings that exceed its upfront cost, yet most payer systems lack annuity payment models, outcomes-based risk-sharing agreements, or multi-year amortisation frameworks that could make these therapies financially sustainable at scale. Until outcome-based reimbursement models become standard — a transition that is underway but unlikely to be complete before 2028 — cell and gene therapy adoption will be structurally constrained by payer financing mechanics, not clinical evidence.

Personalised Medicine Market: Report Scope

|

Personalised Medicine Market Report: Scope & Coverage |

|

|

Report Name |

Global Personalised Medicine Market by Therapy Area (Oncology, Cardiology, Neurology, Rare Diseases, Others), by Technology (Genomics & Proteomics, Companion Diagnostics, Precision Diagnostics, Digital Health & AI, Others), by Drug Type (Small Molecules, Biologics, Cell & Gene Therapies, Others), by End User (Hospitals & Clinics, Diagnostic Laboratories, Research Institutes, Pharmaceutical Companies, Others), and by Region — Global Market Size, Share, Growth, Trends, Forecast 2026–2034 |

|

Market Size in 2025 |

USD 14,820 Mn |

|

Market Forecast in 2034 |

USD 94,680 Mn |

|

Growth Rate (CAGR) |

22.7% |

|

Historical Data Period |

2019–2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026–2034 |

|

Number of Pages |

300+ |

|

Tables & Figures |

110–140 tables, 80–100 figures |

|

Report Code |

ZMR-10572 |

|

Report Format |

|

|

Delivery Format |

Digital Download (PDF) |

|

Published Date |

May 2025 |

|

Research Methodology |

Primary (Interviews, Surveys) + Secondary (Databases, Company Reports, Regulatory Filings) |

|

Key Companies Covered |

Roche, Novartis, Pfizer, Illumina, Thermo Fisher Scientific, Foundation Medicine, QIAGEN, AstraZeneca, Merck & Co., J&J, Guardant Health, Pacific Biosciences, Genomic Health, Blueprint Medicines, Exact Sciences |

|

Segments Covered |

By Therapy Area, By Technology, By Drug Type, By End User, By Region |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, The Middle East, Africa |

|

Customization Scope |

Available — contact sales@zionmarketresearch.com for custom scope, additional segments, or extended forecast periods |

Personalised Medicine Market: Segmentation

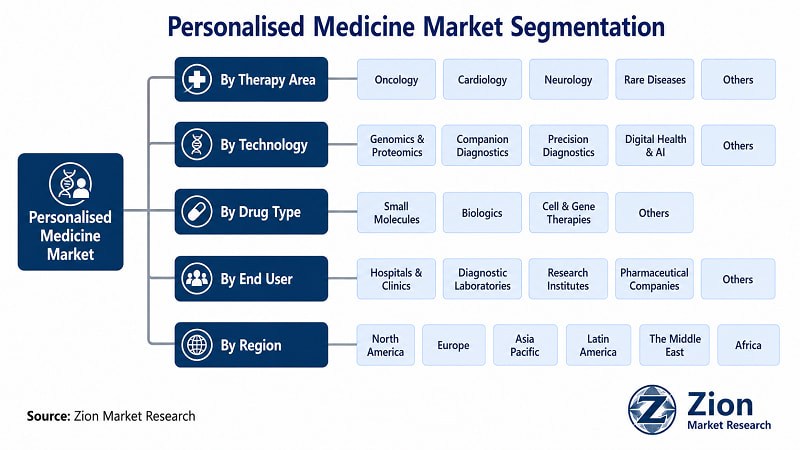

The Global Personalised Medicine market is segmented by Therapy Area, Technology, Drug Type, End User, and Region.

- By Therapy Area

The Therapy Area dimension encompasses Oncology, Cardiology, Neurology, Rare Diseases, and Others. Oncology dominates, holding an estimated 38% of global revenue in 2025, driven by the density of companion diagnostic approvals in solid tumour indications — including lung, breast, colorectal, and haematological cancers — where genomic stratification has become the regulatory standard for therapeutic approval. Foundation Medicine's FoundationOne CDx, approved as a companion diagnostic for multiple targeted therapies, exemplifies the oncology-linked diagnostic architecture that anchors this segment's dominance. Rare Diseases is the fastest-growing therapy area sub-segment, with gene therapy approvals for conditions including spinal muscular atrophy (Zolgensma), beta-thalassaemia (Zynteglo), and sickle cell disease (Casgevy) creating a high-CAGR, high-ASP category within the broader market. Cardiology and Neurology represent emerging high-potential sub-segments as pharmacogenomics guidance for cardiovascular and psychiatric drug selection moves from clinical research into commercial adoption.

- By Technology

The Technology dimension spans Genomics & Proteomics, Companion Diagnostics, Precision Diagnostics, Digital Health & AI, and Others. Genomics & Proteomics leads, underpinning the entire personalised medicine value chain — from foundational variant identification through to clinical interpretation. The sub-segment's dominance reflects the universal applicability of genomic data across all therapy areas and drug types. Companion Diagnostics is the fastest-growing technology sub-segment in terms of regulatory momentum, with FDA approval rate accelerating to approximately 8–10 new companion diagnostic clearances per year. Digital Health & AI represents the highest forward-looking growth sub-segment through 2034, as AI-driven clinical decision support platforms scale from pilot deployments to enterprise-wide clinical infrastructure. Thermo Fisher Scientific's Oncomine Dx Target Test — a multi-biomarker companion diagnostic platform — exemplifies the shift toward comprehensive, multi-target precision diagnostic architecture that is displacing single-biomarker test approaches.

- By Drug Type

The Drug Type dimension covers Small Molecules, Biologics, Cell & Gene Therapies, and Others. Biologics currently holds the largest share — including monoclonal antibodies, antibody-drug conjugates, and checkpoint inhibitors — as the dominant drug type in precision oncology commercial revenue. Cell & Gene Therapies is the fastest-growing sub-segment by CAGR, driven by expanding CAR-T indications and the first commercial gene editing approvals. Novartis's Kymriah remains the reference case for commercial CAR-T viability, with annual revenues exceeding USD 500 Mn demonstrating the per-patient value model's commercial sustainability. Small molecules retain significance in pharmacogenomics applications — particularly in cardiovascular, psychiatric, and metabolic disease — where genomic dosing guidance is increasingly incorporated into drug labelling.

- By End User

The End User dimension includes Hospitals & Clinics, Diagnostic Laboratories, Research Institutes, Pharmaceutical Companies, and Others. Hospitals & Clinics dominate, commanding the largest revenue share as integrated genomic oncology programmes become standard clinical infrastructure at major academic medical centres. Mayo Clinic, MD Anderson, and Memorial Sloan Kettering have each deployed comprehensive precision medicine programmes that combine genomic testing, companion diagnostic-linked therapy selection, and digital health monitoring — creating a vertically integrated clinical model that generates recurring diagnostic and therapeutic revenue. Diagnostic Laboratories — including independent operators such as Quest Diagnostics and LabCorp — represent the highest volume sub-segment for genomic test ordering outside the hospital setting. Pharmaceutical Companies are increasingly represented as direct customers for genomic data platforms, using precision data infrastructure to support companion diagnostic co-development and clinical trial patient stratification.

Personalised Medicine Market: Regional Analysis

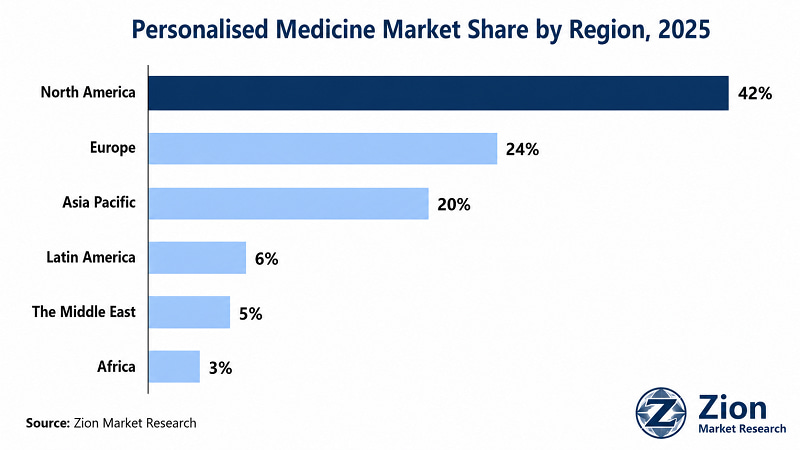

North America dominates the Global Personalised Medicine market, supported by the U.S.'s role as the world's primary regulatory reference market for companion diagnostics and precision therapeutics. Asia Pacific registers the fastest growth rate, driven by structural health system investment in China, India, and South Korea that is converting latent genomic capability into active clinical deployment.

- North America Personalised Medicine Market

North America holds the dominant share of global Personalised Medicine revenue, driven by the U.S.'s unmatched companion diagnostic approval density, biotech venture capital ecosystem, and broad payer coverage for genomic diagnostics. The U.S. accounts for the majority of FDA companion diagnostic approvals to date and serves as the primary commercial launch market for virtually every precision oncology therapeutic. The National Cancer Institute's Precision Medicine Initiative and NIH's All of Us Research Programme are generating the population genomic reference infrastructure that expands the addressable diagnostic market. Canada is advancing through its Canadian Genomics Enterprise and Precision Health Initiative, with investments in genomic newborn screening and pharmacogenomics programmes. Mexico represents an early-stage market with growing private laboratory penetration for oncology genomic diagnostics. The near-term challenge in North America is payer coverage fragmentation for non-oncology genomic applications — a restraint that is gradually resolved as clinical utility evidence accumulates.

- Europe Personalised Medicine Market

Europe is the second-largest regional market, anchored by Germany, the U.K., and France. The U.K.'s Genomics England 100,000 Genomes Project — now expanded to 500,000 whole genomes — has established the world's largest national clinical genomics programme and positioned the NHS as a global reference model for health system genomic integration. Germany leads European companion diagnostic adoption, with the IQWiG (Institute for Quality and Efficiency in Healthcare) progressively incorporating genomic biomarker evidence into benefit assessment decisions. France's Plan France Médecine Génomique 2025 has deployed 13 genomic sequencing national platforms, creating a distributed clinical genomics infrastructure. Sweden and Denmark lead in digital health integration, with national health data registers providing longitudinal population datasets for AI-driven precision medicine development. The primary European restraint remains the absence of pan-EU reimbursement harmonisation for genomic diagnostics — each member state operates distinct coverage criteria that fragment the commercial market.

- Asia Pacific Personalised Medicine Market

Asia Pacific is the fastest-growing regional market, driven by four distinct national investment programmes operating in parallel. China's Precision Medicine Initiative — announced in 2015 with multi-billion RMB investment — has generated the infrastructure for large-scale genomic research and clinical application. BGI Genomics, operating as a state-connected platform, has deployed clinical genomic sequencing at public hospital scale across major Chinese cities. India's diagnostic sector is undergoing rapid laboratory infrastructure expansion, with NABL-accredited molecular diagnostic laboratories growing at double-digit rates. South Korea's KBio Health national genomics programme and government support for biotech precision medicine companies have positioned it as a regional innovation hub. Japan's PMDA has implemented streamlined approval pathways for precision therapeutics, and Australia's Genomics Health Futures Mission has invested AUD 500 Mn in national genomic medicine infrastructure, with a focus on rare disease and paediatric oncology applications.

- Latin America Personalised Medicine Market

Latin America represents a growing but access-constrained market for Personalised Medicine. Brazil leads regional adoption, driven by a large oncology patient population, expanding private diagnostic laboratory networks (Fleury, DASA, Hermes Pardini), and progressive ANVISA regulatory engagement with precision oncology diagnostics. Argentina and Colombia are developing companion diagnostic infrastructure through academic hospital networks. The primary regional challenge is affordability: genomic sequencing and targeted therapy costs are prohibitive for the majority of patients dependent on public health systems. Brazil's SUS (Unified Health System) has initiated selective coverage for specific genomic diagnostics in oncology — a precedent that is expected to expand through 2028. Chile and Peru are emerging entry points, with private sector diagnostic investments leading commercial adoption ahead of public system coverage.

- The Middle East Personalised Medicine Market

The Middle East is an emerging but investment-rich market for Personalised Medicine, driven by GCC nations' health transformation agendas. Saudi Arabia's Vision 2030 health strategy includes dedicated precision medicine and genomics investment — the Saudi Human Genome Programme has sequenced over 100,000 Saudi genomes, creating a reference population database for regional variant interpretation. The UAE's Emirati Genome Programme (EGP) is sequencing the entire Emirati citizen population — the most ambitious national genomics initiative per capita in the world. Qatar's QBioBank represents the GCC's most mature biobank infrastructure for population genomics research. Israel is the region's most advanced precision medicine market, with Clalit Health Services operating one of the world's largest integrated genomic health programmes. Turkey is building clinical pharmacogenomics infrastructure through its national health insurance system. Iran represents a distinct market constrained by international trade restrictions.

- Africa Personalised Medicine Market

Africa is at the earliest stage of Personalised Medicine market development, with significant structural barriers — including limited genomic infrastructure, inadequate laboratory capacity, and near-absent genomic reimbursement — constraining near-term commercial volume. South Africa is the most advanced African market, with NHLS (National Health Laboratory Service) and private operators including Ampath and PathCare providing molecular diagnostic services, and Stellenbosch University's genomics research programme contributing to African-specific genomic reference data. Egypt is investing in genomic medicine capacity through its National Cancer Institute and genomics research partnerships. Nigeria represents the largest long-term demographic opportunity, with genomics access increasing through diaspora-connected private healthcare networks. The continent's primary contribution to the global Personalised Medicine market through 2034 will be through research participation — African genomic diversity is scientifically critical for addressing the reference database gap that limits diagnostic accuracy for non-European populations globally.

Full Country Coverage

|

Country Coverage — Global Personalised Medicine Market Report |

|

|

North America |

The U.S., Canada, Mexico |

|

Europe |

Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe |

|

Asia Pacific |

China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific |

|

Latin America |

Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America |

|

The Middle East |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

Africa |

South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa |

**Country-level market sizing, historical data, and forecasts available for all geographies listed. Custom regional add-ons available — contact sales@zionmarketresearch.com

Personalised Medicine Market: Competitive Landscape

- The Global Personalised Medicine competitive landscape is moderately consolidated at the platform layer and highly fragmented at the application layer. Large pharma-diagnostics conglomerates — Roche, Novartis, Thermo Fisher Scientific — compete on breadth of portfolio and regulatory track record, while specialist precision diagnostics and genomics companies differentiate on bioinformatics depth, clinical utility validation, and speed-to-approval. The dominant strategic pattern is pharma-diagnostics bundling: major pharmaceutical manufacturers are acquiring or partnering with diagnostics companies to co-develop companion diagnostics alongside therapeutic programmes, creating proprietary diagnostic-therapeutic bundles that raise switching costs and protect margin.

- Key players: Roche Holdings AG, Novartis AG, Pfizer Inc., Illumina Inc., Thermo Fisher Scientific Inc., Foundation Medicine Inc., QIAGEN N.V., AstraZeneca plc, Merck & Co. Inc., Johnson & Johnson, Guardant Health Inc., Pacific Biosciences of California Inc., Genomic Health Inc., Blueprint Medicines Corporation, and Exact Sciences Corporation.

|

Company |

HQ Country |

Primary Focus |

Key Strategy |

Notable Recent Action |

|

Roche Holdings AG |

Switzerland |

Companion Diagnostics & Oncology |

Pharma-diagnostic bundling; FDA co-approval |

FoundationOne CDx pan-tumour companion diagnostic expansion (2025) |

|

Novartis AG |

Switzerland |

CAR-T Cell Therapies |

Pipeline expansion into solid tumours |

Kymriah solid tumour IND filings, CAR-T manufacturing expansion (2024) |

|

Pfizer Inc. |

U.S. |

Gene Therapy & Oncology |

M&A-driven rare disease pipeline build |

Acquisition of Seagen for ADC portfolio, rare disease gene therapy investment (2023–2024) |

|

Illumina Inc. |

U.S. |

Genomic Sequencing Platforms |

Cost reduction & clinical-grade deployment |

NovaSeq X Series Asia Pacific launch (2025) |

|

Thermo Fisher Scientific |

U.S. |

Multi-platform Genomics |

Full-stack genomics supply chain |

Oncomine companion diagnostic portfolio expansion (ongoing) |

|

Foundation Medicine |

U.S. |

Precision Oncology Diagnostics |

Multi-biomarker CDx architecture |

FoundationOne Liquid CDx pan-tumour FDA submission (2025) |

|

QIAGEN N.V. |

Netherlands |

Molecular Diagnostics |

Sample-to-insight platform integration |

QIAstat-Dx companion diagnostic development programmes |

|

AstraZeneca plc |

U.K. |

Precision Oncology & Rare Disease |

Biomarker-led clinical development |

Rare disease gene therapy pipeline expansion (2024–2025) |

|

Merck & Co. Inc. |

U.S. |

Immuno-Oncology |

Pembrolizumab companion diagnostic ecosystem |

PD-L1 companion diagnostic label expansions (ongoing) |

|

Guardant Health Inc. |

U.S. |

Liquid Biopsy |

Colorectal and multi-cancer early detection |

SHIELD colorectal cancer screening FDA approval (July 2024) |

|

Blueprint Medicines |

U.S. |

Kinase Inhibitors |

Precision molecular targeting |

Avapritinib GIST indication expansion |

|

Exact Sciences |

U.S. |

Cancer Screening |

Non-invasive genomic detection |

Cologuard Plus FDA approval and commercial rollout (2024) |

|

Pacific Biosciences |

U.S. |

Long-Read Sequencing |

Structural variant detection |

Revio sequencing system clinical deployments |

|

Genomic Health |

U.S. |

Oncotype DX Diagnostics |

Clinical utility evidence generation |

Oncotype DX breast cancer recurrence score label expansion |

|

Johnson & Johnson |

U.S. |

Oncology & Rare Disease |

Diversified pharma-diagnostics portfolio |

CAR-T and bispecific antibody pipeline advancement (2024–2025) |

- Across the competitive set, three strategic themes dominate: (1) pharma-diagnostics bundling — co-developing companion diagnostics alongside therapeutics to create locked-in commercial ecosystems; (2) liquid biopsy platform expansion — extending genomic detection from diagnostic confirmation into screening and early detection; and (3) manufacturing scale investment — particularly in CAR-T and gene therapy, where capacity constraints represent the primary near-term commercial bottleneck. Companies capturing disproportionate value through 2034 will be those that achieve regulatory approval density (multiple CDx approvals in multiple indications) while simultaneously solving the manufacturing scalability constraint that limits cell therapy access.

Recent Developments in the Personalised Medicine Market

Strategic activity in the Global Personalised Medicine market has accelerated materially since 2023, with regulatory approvals, manufacturing investments, and platform acquisitions signalling broad-based commercial confidence in the market's trajectory.

|

Date |

Company |

Type |

Description |

Market Impact |

|

July 2024 |

Guardant Health |

FDA Approval |

SHIELD test approved for colorectal cancer screening — first liquid biopsy screening test for average-risk populations |

Expands liquid biopsy TAM from diagnostic confirmation into mass-market screening |

|

March 2025 |

Roche / Foundation Medicine |

Regulatory Submission |

FoundationOne Liquid CDx next-generation submission as pan-tumour companion diagnostic targeting 30+ biomarkers |

Extends Roche companion diagnostic revenue across 15+ cancer types |

|

January 2025 |

Illumina |

Product Launch |

NovaSeq X Series launched in Japan and South Korea — clinical-grade WGS for Asia Pacific markets |

Accelerates Asia Pacific clinical genomics adoption and regional market growth |

|

October 2024 |

Novartis |

Investment |

CAR-T manufacturing facility acquisition in New Jersey — estimated 40% production capacity increase |

Addresses Kymriah supply constraints ahead of solid tumour indication expansions |

|

November 2024 |

AstraZeneca |

Strategic Partnership |

Partnership with Tempus AI for multi-omic data platform integration in oncology clinical trials |

Strengthens AstraZeneca precision medicine pipeline with real-world genomic data access |

|

December 2024 |

Blueprint Medicines |

FDA Approval |

Avapritinib received expanded FDA approval for indolent systemic mastocytosis indication |

Demonstrates kinase inhibitor precision model beyond GIST — broadens therapy area coverage |

About Zion Market Research

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is updated constantly in order to fulfil our clients' requirements for prompt and direct online access. Keeping in mind the client's needs, we have included expert insights on global industries, products, and market trends in this database.

Author:

Mr. Nilesh Patil

Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067

Table Of Content

Methodology

FrequentlyAsked Questions

The Zion Market Research's Personalised Medicine Market Report is a 300+-page intelligence document covering market sizing (USD 14,820 Mn–USD 94,680 Mn), 22.7% CAGR forecasts across 2026–2034, five segmentation dimensions, 35+ country-level analyses, 15 company profiles with strategy tables, full DROC analysis (Drivers, Restraints, Opportunities, Challenges), recent developments, research methodology, and 110–140 data tables with 80–100 figures.

The Global Personalised Medicine market was valued at USD 14,820 Mn in 2025 and is projected to reach USD 94,680 Mn by 2034, registering a 22.7% CAGR during 2026–2034, according to Zion Market Research. North America holds the dominant regional share. Oncology leads by therapy area. Genomics & Proteomics leads by technology. Cell & Gene Therapies is the fastest-growing drug type sub-segment.

The report segments the Personalised Medicine market across five dimensions: By Therapy Area (Oncology, Cardiology, Neurology, Rare Diseases, Others); By Technology (Genomics & Proteomics, Companion Diagnostics, Precision Diagnostics, Digital Health & AI, Others); By Drug Type (Small Molecules, Biologics, Cell & Gene Therapies, Others); By End User (Hospitals & Clinics, Diagnostic Laboratories, Research Institutes, Pharmaceutical Companies, Others); and By Region (six regions, 35+ countries).

The report covers 35+ countries across 6 ZMR regions as separate regional analyses (Middle East and Africa are always treated as separate regions — never combined). North America: The U.S., Canada, Mexico. Europe: Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria. Asia Pacific: China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan. Latin America: Brazil, Argentina, Colombia, Chile, Peru. The Middle East: GCC, Israel, Turkey, Iran. Africa: South Africa, Egypt, Nigeria, Algeria, Morocco.

Zion Market Research offers a full range of customization options for this report, including: additional market segments or sub-segments not included in the standard scope; extended forecast periods beyond 2034; deeper country-specific analysis for specific geographies; competitive analysis focused on a defined subset of companies; and custom primary research — qualitative interviews with market participants specific to your strategic question. Contact sales@zionmarketresearch.com or +1 (302) 444-0166 to discuss scope and pricing.

Three access options: (1) Free Sample — preview key tables, methodology, and segmentation data at no cost (2) Full Report Purchase — 300+ pages PDF (3) Custom Research Inquiry — tailored scope. contact sales@zionmarketresearch.com | +1 (302) 444-0166 | +1 (855) 465-4651.

List of Contents

Personalised Medicine Industry Perspective:Personalised Medicine OverviewKey InsightsWhy Choose the Zion Market ResearchsPersonalised Medicine Market Report?Personalised Medicine: Dynamics (Drivers, Restraints, Opportunities, Challenges)Personalised Medicine Report ScopePersonalised Medicine SegmentationPersonalised Medicine Regional AnalysisFull Country CoveragePersonalised Medicine Competitive LandscapeRecent Developments in theMarketHappyClients