Osseointegration Implants Market Size, Share, Growth Report 2032

Osseointegration Implants Market By Product (Dental Implants, Hip Implants, Knee Implants, and Spinal Implants), by Material (Titanium Implants, Ceramic Implants, Zirconia Implants, and Others), by End-User (Hospitals, Ambulatory Surgical Centers, and Others), and By Region: Global Industry Perspective, Comprehensive Analysis, and Forecast, 2024-2032

| Market Size in 2023 | Market Forecast in 2032 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 8.62 Billion | USD 17.03 Billion | 7.86% | 2023 |

Osseointegration Implants Industry Perspective:

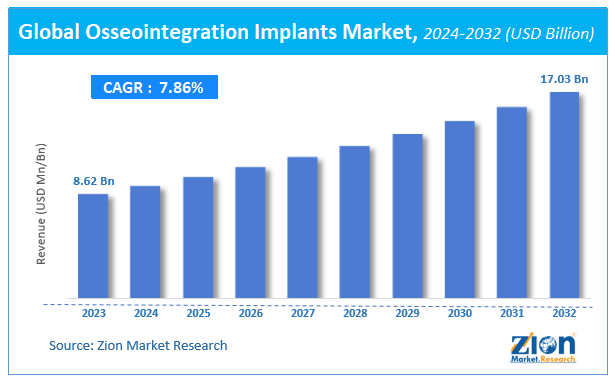

The global Osseointegration Implants market size accrued earnings worth approximately USD 8.62 billion in 2023 and is predicted to gain revenue of about USD 17.03 billion by 2032, and is set to record a CAGR of nearly 7.86% over the period from 2024 to 2032. The study includes drivers and restraints of the osseointegration implants market, along with their impact on the demand over the forecast period. Additionally, the report includes the study of opportunities available in the osseointegration implants market on a global level.

Osseointegration Implants Market: Overview

The attachment of active bones to a metal surface until they become firmer is known as osseointegration. This implant contains pores with cells containing connective tissue and osteoblasts that migrate freely. Osseointegration has various applications in the field of joint replacement techniques, such as improving the amputees’ lifestyles, dental implants, etc. Osseointegration is a widely accepted implant approach used in the healthcare industry today. Other factors impacting the bone's attachment to metal surfaces include the nature of the implant, the biocompatibility of the implant material, the required healing time, and the surgical technique involved in the bone attachment.

Key Insights

- As per the analysis shared by our research analyst, the global Osseointegration Implants Market is estimated to grow annually at a CAGR of around 7.86% over the forecast period (2024-2032).

- In terms of revenue, the global Osseointegration Implants Market size was valued at around USD 8.62 billion in 2023 and is projected to reach USD 17.03 billion by 2032.

- The Osseointegration Implants market is driven by the increasing prevalence of bone-related disorders and demand for advanced implant solutions.

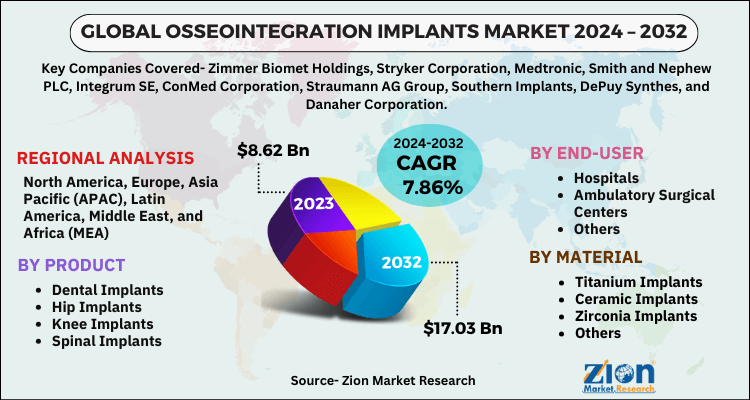

- Based on the product, the dental implants segment dominated the market in 2023 with a share of 48% due to the high incidence of dental caries and growing cosmetic dentistry procedures.

- Based on the material, the titanium implants segment dominated the market in 2023 with a share of 68% owing to superior biocompatibility, strength, and proven long-term integration success.

- Based on the end-user, the hospitals segment dominated the market in 2023 with a share of 62% because of their advanced surgical infrastructure and high volume of complex procedures.

- North America dominated the global market in 2023 with a share of 42%, attributed to a large geriatric population, favorable reimbursement policies, and the strong presence of leading manufacturers.

Market Dynamics

Growth Drivers

Advancements in Implant Technologies and Materials

Continuous innovations in surface treatments and titanium alloys have significantly improved osseointegration speed and implant longevity, encouraging widespread adoption among orthopedic and dental surgeons. These developments reduce healing time and complication rates, making the technology more accessible for a broader patient base. Additionally, supportive insurance coverage and regulatory approvals have lowered financial barriers, particularly for bone-anchored prostheses. Rising awareness among amputees and dental patients has further accelerated demand, positioning osseointegration as a preferred solution over conventional methods.

Restraints

Complications and Surgical Risks

Potential issues such as infection, implant failure, or prolonged healing periods deter some patients and clinicians from choosing osseointegration implants. These risks require careful patient selection and skilled surgical execution, increasing overall procedure complexity. Moreover, the need for specialized training and equipment limits availability in smaller healthcare facilities. Such concerns contribute to cautious adoption rates, especially in cost-sensitive or resource-limited settings.

Opportunities

Rising Demand for Bone-Anchored Prostheses

Growing acceptance of osseointegration among amputees, combined with expanding applications in cosmetic and reconstructive dentistry, opens substantial growth avenues. Improved patient outcomes and quality-of-life benefits drive referrals and repeat procedures. Furthermore, increasing disposable incomes in emerging economies and a global focus on oral hygiene create new markets for dental and orthopedic implants. Manufacturers can capitalize on these trends through targeted product development and regional expansion.

Challenges

High Procedure Costs and Regulatory Hurdles

The elevated cost of implants and associated surgeries restricts access for middle-income patients and smaller clinics. Stringent approval processes across different countries also delay market entry for new technologies. In addition, variability in healthcare infrastructure and reimbursement policies creates uneven growth opportunities. Overcoming these barriers demands cost-optimization strategies and stronger advocacy for broader insurance coverage.

Osseointegration Implants Market: Segmentation

The global osseointegration implants market is segmented into material, product, end-user. and region.

By product, the market is divided into dental implants, hip implants, knee implants, and spinal implants. The most dominant segment is dental implants, which leads due to widespread prevalence of dental caries and strong demand for aesthetic restorations, driving market growth by addressing everyday oral health needs across age groups. The second most dominant is hip implants, favored for joint replacement surgeries in aging populations, contributing to expansion through reliable mobility restoration and long-term durability.

By material, the market is divided into titanium implants, ceramic implants, zirconia implants, and others. The most dominant segment is titanium implants, dominating because of exceptional biocompatibility and mechanical strength that promote faster bone integration, propelling market growth through proven clinical success in high-load applications. The second most dominant is zirconia implants, gaining traction for metal-free aesthetics in dental procedures, boosting the market by appealing to patients seeking natural-looking solutions.

By end-user, the market includes hospitals, ambulatory surgical centers, and others. The hospital is the most dominant segment, leading owing to comprehensive surgical facilities and the ability to handle complex multi-specialty cases, driving overall market advancement through high procedural volumes. The second most dominant is ambulatory surgical centers, expanding access via outpatient convenience and cost efficiency, contributing to growth by serving increasing numbers of elective implant procedures.

Osseointegration Implants Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Osseointegration Implants Market |

| Market Size in 2023 | USD 8.62 Billion |

| Market Forecast in 2032 | USD 17.03 Billion |

| Growth Rate | CAGR of 7.86% |

| Number of Pages | 201 |

| Key Companies Covered | Zimmer Biomet Holdings, Stryker Corporation, Medtronic, Smith and Nephew PLC, Integrum SE, ConMed Corporation, Straumann AG Group, Southern Implants, DePuy Synthes, and Danaher Corporation |

| Segments Covered | By Product, By Material, By End-user, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, the Middle East and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2022 |

| Forecast Year | 2024 - 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Osseointegration Implants Market: Regional Analysis

North America to dominate the global market

North America leads the osseointegration implants market, primarily driven by the United States, where an aging population and high incidence of bone-related disorders create sustained demand for advanced orthopedic and dental solutions. The region benefits from robust healthcare infrastructure, favorable reimbursement policies, and strong collaboration between hospitals and manufacturers. Extensive research activities at academic institutions continue to refine implant designs, while consumer awareness of improved quality-of-life benefits accelerates adoption. Canada supports this dominance through similar trends in joint replacements and dental care, ensuring North America maintains its position at the forefront of innovation and clinical application.

Europe demonstrates significant strength in osseointegration implants, spearheaded by Germany with its well-developed healthcare system and rapid approval of new technologies. The continent emphasizes precision engineering and patient-centric solutions, particularly in dental and hip replacements. Countries such as the United Kingdom and France contribute through active investment in ambulatory surgical centers and cosmetic dentistry. Regulatory harmonization across the EU facilitates smoother market access, while a focus on elderly care drives consistent growth in spinal and knee applications throughout the region.

Asia Pacific is experiencing rapid expansion in osseointegration implants, led by China through urbanization, rising disposable incomes, and government initiatives to improve healthcare access. India and Japan bolster demand with growing dental tourism and orthopedic procedures, supported by local manufacturing capabilities. The region’s large patient pool for trauma and degenerative diseases creates opportunities for both premium and cost-effective implants. Southeast Asian nations are gradually adopting advanced technologies through international partnerships, positioning the Asia Pacific as a high-potential growth engine.

Recent Developments

- In December 2024, Zimmer Biomet Holdings expanded its osseointegration portfolio with a new titanium surface treatment designed to accelerate bone integration in hip and knee implants.

- In October 2024, Stryker Corporation received regulatory clearance for an advanced spinal osseointegration implant featuring enhanced porous architecture for improved stability.

- In September 2024, Integrum SE partnered with leading rehabilitation centers to launch a comprehensive bone-anchored prosthesis program targeting amputee populations.

- In July 2024, Straumann AG Group introduced a zirconia-based dental osseointegration system aimed at metal-sensitive patients in cosmetic dentistry.

- In May 2024, Smith and Nephew PLC invested in R&D to develop next-generation ceramic implants with superior wear resistance for joint replacement applications.

Osseointegration Implants Market: Competitive Analysis

Some leading players of the global osseointegration implants market are

- Zimmer Biomet Holdings

- Stryker Corporation

- Medtronic

- Smith and Nephew PLC

- Integrum SE

- ConMed Corporation

- Straumann AG Group

- Southern Implants

- DePuy Synthes

- Danaher Corporation

This report segments the global osseointegration implants market into:

By Product

- Dental Implants

- Hip Implants

- Knee Implants

- Spinal Implants

By Material

- Titanium Implants

- Ceramic Implants

- Zirconia Implants

- Others

By End-User

- Hospitals

- Ambulatory Surgical Centers

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

HappyClients