Non-Woven Textile For Composites Market Size, Trend, Growth, Industry Analysis 2034

Non-Woven Textile For Composites Market By Product Type (Non-Crimp Textiles, CSM/CFM), By Material Type (Glass Fiber, Carbon Fiber, Natural Fiber, and Others), By End-Use Industry (Wind Energy, Transportation, Marine, Construction, Aerospace and Defense, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

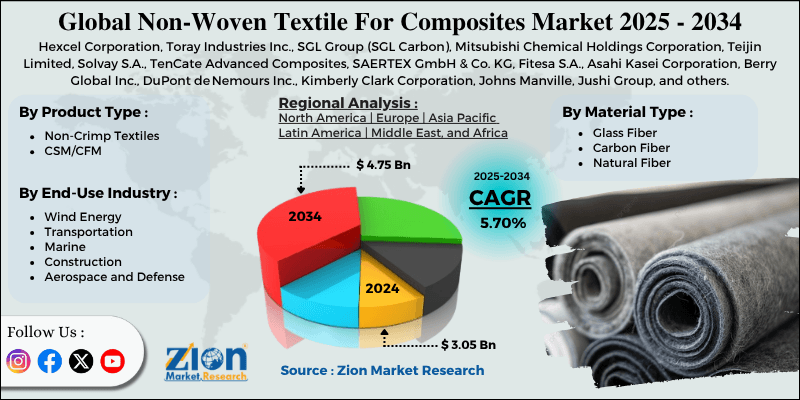

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 3.05 Billion | USD 4.75 Billion | 5.70% | 2024 |

Non-Woven Textile For Composites Industry Perspective:

What will be the size of the global non-woven textile for composites market during the forecast period?

The global non-woven textile for composites market size was around USD 3.05 billion in 2024 and is projected to reach USD 4.75 billion by 2034, with a compound annual growth rate (CAGR) of roughly 5.70% between 2025 and 2034.

Key Insights:

- As per the analysis shared by our research analyst, the global non-woven textile for composites market is estimated to grow annually at a CAGR of around 5.70% over the forecast period (2025-2034)

- In terms of revenue, the global non-woven textile for composites market size was valued at around USD 3.05 billion in 2024 and is projected to reach USD 4.75 billion by 2034.

- The non-woven textile for composites market is projected to grow significantly owing to growth in the infrastructure and construction sector, expansion of the wind energy sector, and the growing leisure and sports equipment market.

- Based on product type, the non-crimp textiles segment is expected to lead the market, while the CSM/CFM segment is expected to grow considerably.

- Based on material type, the glass fiber segment is the largest, while the carbon fiber segment is projected to record sizeable revenue over the forecast period.

- Based on end-use industry, the wind energy segment is expected to lead the market, followed by the transportation segment.

- Based on region, the Asia Pacific is projected to dominate the global market during the estimated period, followed by North America.

Non-Woven Textile For Composites Market: Overview

Non-woven textiles for composites are engineered fiber mats made by entangling or bonding fibers instead of weaving, offering uniformity, high porosity, and directional strength. They serve as reinforcement in metal, polymer, or ceramic matrices, improving mechanical properties, lightweight performance, and impact resistance. The global non-woven textile for composites market is poised to expand rapidly, driven by growing demand for automotive lightweighting, expansion in aerospace applications, and growth in the renewable energy sector. The automotive industry’s push for lightweight vehicles to reduce emissions and enhance fuel efficiency is driving increased use of nonwoven textile composites. These materials allow major weight savings while maintaining safety standards and strength. As OEMs adopt hybrid and electric platforms, demand for high-performance non-wovens continues to grow.

Moreover, interior components and airframe increasingly employ non-woven composites for their high strength-to-weight ratios. Improved fatigue resistance and vibration damping make these materials appealing for the next-gen aircraft. Stringent fuel-efficiency targets and long aircraft lifespan are fueling adoption. Furthermore, structural components and wind turbines increasingly use nonwoven composites to enhance performance and durability. Large fiber mats help enhance fatigue and reduce maintenance costs. As global renewable installations grow, composite nonwovens are gaining notable market share.

Despite growth, the global market is constrained by factors such as complex processing requirements, recycling challenges, and end-of-life issues. Composite manufacturing with nonwoven textiles often requires dedicated equipment and expertise. High setup and maintenance investments deter small manufacturers. Process variability may affect quality, negatively impacting wide acceptance. Likewise, thermoset composites, common in non-woven applications, are difficult to recycle. Limited infrastructure for composite recycling increases environmental concerns. Regulatory pressure towards circular-economy models may hamper their use.

Nonetheless, the global non-woven textile for composites industry stands to benefit from several key opportunities, such as the electrification of transportation and the integration of smart textiles. EV production growth generates demand for low-weight composites to increase range and enhance efficiency. Non-woven reinforcements for battery enclosures and body panels offer fresh applications. Long-term growth in the EV market drives material demand. Embedding functional additives and sensors into non-woven composites allows smart structural health monitoring. Industry 4.0 trends increase material differentiation. Smart composites unveil fresh premium application segments.

Non-Woven Textile For Composites Market: Dynamics

Growth Drivers

How is the non-woven textile for composites market growth augmented by the rapid electrification of automobiles?

As EV production accelerates worldwide, OEMs prioritize lightweight components to maximize battery range and efficiency. Non-woven textile reinforcements allow weight reduction while maintaining crashworthiness and structural integrity in composite components. According to reports, the expanding use of composites in battery housings, EV chassis, and interior structural elements is evident. The automotive shift to EVs, hence, significantly escalates demand for tailored nonwoven composite materials. Regulatory pressure to cut transport emissions further reinforces this trend.

How are advancements in manufacturing technologies fueling the non-woven textile for composites market?

Continued innovation in nonwoven production methods, such as layering, improved bonding, and hybridization techniques, improves material performance and reduces processing costs. Technological progress has driven process consistency, enhanced delamination resistance, and streamlined integration into composite molding. Industry analysts cite ongoing R&D as a vital growth catalyst, allowing bespoke textile reinforcement solutions for complex composite geometrics. This fuels wider adoption in emerging and traditional end uses, propelling the non-woven textile for composites market.

Restraints

Raw material price volatility negatively impacts the market progress

Price fluctuations in essential raw materials such as resins, fiberglass, and specialty polymers increase production costs for nonwoven composites. Worldwide supply chain interruptions, such as disruptions to petrochemical feedstock, amplify cost unpredictability. Small manufacturers experience margin compression, limiting expansion and advancement. Cost volatility also discourages OEMs from making long-term procurement commitments. This financial uncertainty is a major limitation in market desirability.

Opportunities

How do customization & tailored composite solutions present favorable prospects for the non-woven textile for composites market?

There is a growing demand for bespoke non-woven textile configurations that match specific functional and mechanical requirements in advanced applications. Composite manufacturers actively seek tailored reinforcements to optimize performance, such as wind-turbine-specific or aerospace-grade textiles. Collaboration between OEMs and suppliers reveals high-value, premium materials. Customized solutions enhance pricing power and differentiation. The push for application-specific innovation offers lucrative niche markets, thereby fueling the global non-woven textile composites industry.

Challenges

Technological complexity & need for a skilled workforce restrict the market growth

Advancing non-woven composite technology demands dedicated production processes and engineering proficiency. Retaining and recruiting talent with advanced composite design and processing skills remains difficult in some regions. Workforce development and training increase operational overheads. Smaller companies face barriers to scaling technical capabilities. This talent gap complicates efficient scaling and innovation.

Non-Woven Textile For Composites Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Non-Woven Textile For Composites Market |

| Market Size in 2024 | USD 3.05 Billion |

| Market Forecast in 2034 | USD 4.75 Bllion |

| Growth Rate | CAGR of 5.70% |

| Number of Pages | 228 |

| Key Companies Covered | Hexcel Corporation, Toray Industries Inc., SGL Group (SGL Carbon), Mitsubishi Chemical Holdings Corporation, Teijin Limited, Solvay S.A., TenCate Advanced Composites, SAERTEX GmbH & Co. KG, Fitesa S.A., Asahi Kasei Corporation, Berry Global Inc., DuPont de Nemours Inc., Kimberly Clark Corporation, Johns Manville, Jushi Group, and others. |

| Segments Covered | By Product Type, By Material Type, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Non-Woven Textile For Composites Market: Segmentation

The global non-woven textile for composites market is segmented based on product type, material type, end-use industry, and region.

Why is the Non-Crimp Textiles segment projected to dominate the non-woven textile for composites market?

Based on product type, the global non-woven textile for composites industry is divided into non-crimp textiles and CSM/CFM. The non-crimp textiles segment captured a dominant 60% market share. Their tailored fiber orientation and high-strength-to-weight ratio make them suitable for automotive, aerospace, and wind energy applications. Superior performance and ease of integration sustain their industry leadership.

Nonetheless, the CSM/CFM segment ranks second, accounting for nearly 45% of the total market. These mats are favored in conventional, cost-sensitive processes such as spray-up and hand lay-up. They offer easier handling and isotropic reinforcement, maintaining a steady demand despite lower performance than non-crimp textiles.

What factors help the Glass Fiber segment lead the non-woven textile for composites market?

Based on material type, the global non-woven textile for composites market is segmented into glass fiber, carbon fiber, natural fiber, and others. The glass fiber segment leads the market with over 60% market share, backed by its versatility and cost-effectiveness. It is broadly used in wind energy, automotive, construction, and marine applications for its adequate strength and durability. Its affordability and well-developed supply chain help maintain its leading rank.

However, the carbon fiber segment holds the second-largest market share, at around 25%, due to its superior strength and high stiffness. It is largely preferred in high-end automotive, aerospace, and premium sporting goods where performance is crucial. Despite high costs, demand is growing amid electrification and lightweighting trends.

What are the key reasons for the leadership of the Wind Energy segment in the non-woven textile for composites market?

Based on end-use industry, the global market is segmented into wind energy, transportation, marine, construction, aerospace and defense, and others. The wind energy segment holds leadership with over 40% market share. It is backed by extensive use of high-strength composites in structural components and turbine blades. Mounting global investments in renewable energy and more efficient and larger turbines fuel demand. Advanced composites replace traditional materials to improve performance and durability while reducing maintenance.

Conversely, the transportation segment ranks second at 30% of the total market. Lightweighting requirements in rail, automotive, and commercial vehicles are driving the adoption of nonwoven textile composites. These materials help enhance fuel efficiency, meet strict regulatory standards, and reduce emissions. Growing sustainability initiatives and electrification further support growth in this segment.

Non-Woven Textile For Composites Market: Regional Analysis

Why is Asia Pacific outperforming other regions in the global Non-Woven Textile For Composites market?

Asia Pacific is anticipated to retain its leading role in the global non-woven textile for composites market, with over 8% CAGR, driven by rapid infrastructure development and industrialization, growth in transportation and automotive sectors, and expansion of renewable energy. Asia-Pacific nations are undergoing massive industrial expansion and urbanization, driving demand for durable, lightweight, and cost-effective composite materials. Non-woven textile composites are largely used in transportation, construction, and energy projects. Infrastructure growth accelerates regional adoption and production capacity. The region also houses major automotive manufacturing hubs, mainly in India, China, and Japan, where fuel efficiency and lightweighting are increasingly mandated. Non-woven composites are used for interior and structural parts to meet these requirements. Growing vehicle production and EV adoption drive industry demand.

Furthermore, APAC leads in solar and wind installations, needing high-performing composites for structural components and turbine blades. Government incentives and sustainability initiatives promote the development of renewable infrastructure. This energy transition fuels steady demand for nonwoven textile composites.

Why does North America rank second in the global Non-Woven Textile For Composites Market?

North America ranks as the second-largest region in the global non-woven textile for composites industry, with a 5-7% CAGR, driven by advanced defense and aerospace, automotive lightweighting, EV adoption, and technological innovation and R&D investments. North America has a strong aerospace and defense sector that demands high-performing composites for military vehicles, aircraft, and structural components.

Nonwoven textiles offer a superior strength-to-weight ratio, which is crucial for these applications. Continuous innovation in aerospace fuels regional industry dominance. Moreover, the region is speedily adopting lightweight composite materials to meet stringent emission and fuel-efficiency regulations. Non-woven textile composites are used in interior automotive, and structural components. Surging electric vehicle production further stimulates demand for advanced composites.

Additionally, strong R&D infrastructure allows the development of high-performance fibers, smart composite solutions, and automated production methods. Private companies, labs, and universities collaborate to enhance the efficiency and properties of non-woven composites. Technological dominance supports early adoption in industries.

Non-Woven Textile For Composites Market: Competitive Analysis

The leading players in the global non-woven textile for composites market are:

- Hexcel Corporation

- Toray Industries Inc.

- SGL Group (SGL Carbon)

- Mitsubishi Chemical Holdings Corporation

- Teijin Limited

- Solvay S.A.

- TenCate Advanced Composites

- SAERTEX GmbH & Co. KG

- Fitesa S.A.

- Asahi Kasei Corporation

- Berry Global Inc.

- DuPont de Nemours Inc.

- Kimberly Clark Corporation

- Johns Manville

- Jushi Group

What are the key trends in the global Non-Woven Textile for Composites Market?

Growth of sustainable and bio‑based fiber solutions:

There is a growing interest in recyclable, natural, and bio-derived fibers to address end-of-life and environmental concerns. Manufacturers are developing eco-friendly non-woven composites with low carbon footprints. The demand for sustainability from regulators and consumers drives innovation in this domain.

Integration of automated and high‑precision manufacturing

Advanced automation, digital fabrication techniques, and robotics are actively integrated into composite production. These technologies reduce waste, enhance consistency, and lower labor costs. Increased efficiency strengthens manufacturers’ ability to scale the output of nonwoven textiles.

The global non-woven textile for composites market is segmented as follows:

By Product Type

- Non-Crimp Textiles

- CSM/CFM

By Material Type

- Glass Fiber

- Carbon Fiber

- Natural Fiber

- Others

By End-Use Industry

- Wind Energy

- Transportation

- Marine

- Construction

- Aerospace and Defense

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Nonwoven textiles for composites are engineered fiber mats made by entangling or bonding fibers rather than weaving, offering uniformity, high porosity, and directional strength. They serve as reinforcement in metal, polymer, or ceramic matrices, improving mechanical properties, lightweight performance, and impact resistance.

The global non-woven textile for composites market is projected to grow due to increasing demand from the automotive industry, rising use in aerospace applications, and technological advancements in composite manufacturing.

According to study, the global non-woven textile for composites market size was around USD 3.05 billion in 2024 and is expected to grow to around USD 4.75 billion by 2034.

The CAGR for the non-woven textile for composites market is expected to be around 5.70% during 2025-2034.

Market trends and consumer preferences are shifting toward high-performance, lightweight, and sustainable non-woven textile composites with eco-friendly materials and advanced automation.

The value chain of the global non-woven textile for composites industry includes sourcing of raw material, fiber processing, manufacturing non-woven fabric, composite fabrication, and distribution to end-use industries.

Asia Pacific is expected to lead the global non-woven textile for composites market during the forecast period.

The key players profiled in the global non-woven textile for composites market include Hexcel Corporation, Toray Industries, Inc., SGL Group (SGL Carbon), Mitsubishi Chemical Holdings Corporation, Teijin Limited, Solvay S.A., TenCate Advanced Composites, SAERTEX GmbH & Co. KG, Fitesa S.A., Asahi Kasei Corporation, Berry Global Inc., DuPont de Nemours, Inc., Kimberly Clark Corporation, Johns Manville, and Jushi Group.

Stakeholders should focus on sustainable materials, innovation, advanced manufacturing technologies, strategic partnerships, and expansion into high-growth end-use industries to stay competitive.

The report examines key aspects of the non-woven textile for composites market, including a detailed analysis of current growth factors and restraints, as well as future growth opportunities and challenges that will affect the market.

List of Contents

Non-Woven Textile For CompositesIndustry Perspective:Key Insights:OverviewDynamicsReport ScopeSegmentationRegional AnalysisCompetitive AnalysisWhat are the key trends in the global Non-Woven Textile for Composites Market?The global non-woven textile for composites market is segmented as follows:HappyClients