Point-of-Care Diagnostics Market Size, Share, Trends & Forecast 2026–2034

Global Point-of-Care Diagnostics Market by Product (Glucose Testing, Infectious Disease Testing, Cardiac Markers, Coagulation Testing, HbA1c Testing, Pregnancy & Fertility Testing, Drug-of-Abuse Testing, Others), by Technology (Lateral Flow Assays, Molecular Diagnostics, Immunoassay Analyzers, Biochemistry), by Mode of Purchase (Prescription-Based, Over-the-Counter), by End User (Hospitals, Clinics, Home Settings, Diagnostic Centres, Ambulatory Care Centres), and by Region (North America, Europe, Asia Pacific, Latin America, The Middle East, Africa) — Global Analysis & Forecast, 2026–2034-

| Market Size in 2025 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 42,180 Million | USD 98,640 Million | 9.9% | 2025 |

Point-of-Care Diagnostics Industry Perspective:

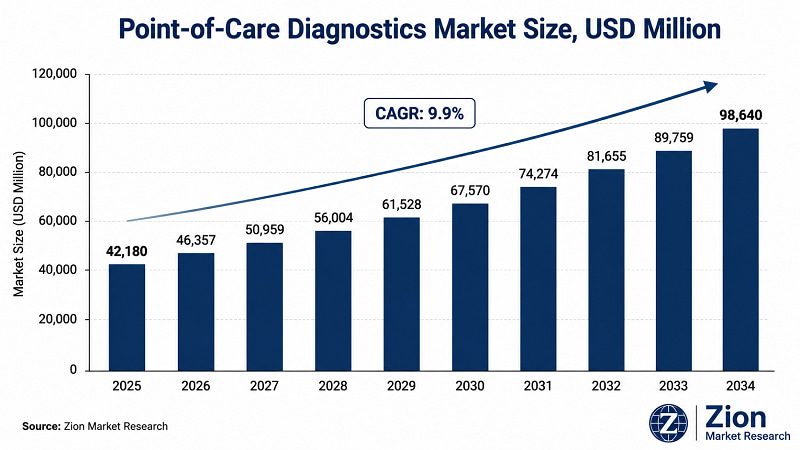

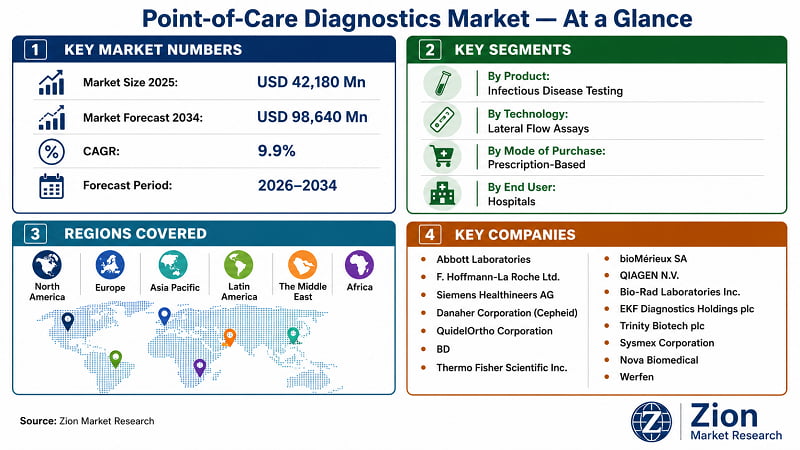

- The Global Point-of-Care Diagnostics market stood at USD 42,180 Mn in 2025 and will reach USD 98,640 Mn by 2034 at a 9.9% CAGR — a rate that exceeds the overall in vitro diagnostics sector's growth trajectory by a significant margin.

- This differential isn't accidental. POC diagnostics are capturing the structural tailwind created by health system economics that increasingly penalise centralised laboratory dependency: longer turnaround times, specimen transport costs, and delayed therapeutic decisions.

- The convergence of CLIA-waived molecular clearances, AI-enhanced result interpretation, and cloud-connected device management has eliminated the historical accuracy trade-off between central labs and near-patient testing. What Zion Market Research identifies as the inflection point is not merely market expansion — it's category redefinition: POC diagnostics are transitioning from a supplementary testing channel to a primary care diagnostic infrastructure.

Point-of-Care Diagnostics Market: Overview

- Point-of-Care Diagnostics encompasses a diverse portfolio of in vitro diagnostic tests, devices, and connected systems designed to generate actionable clinical results at or near the patient's location. The scope extends from simple lateral flow immunoassay strips for pregnancy and infectious disease detection to molecular PCR platforms that deliver results in under 20 minutes — accuracy levels previously achievable only in centralised reference laboratories. The product categories span glucose monitoring, HbA1c testing, cardiac biomarker assays (troponin, NT-proBNP, D-dimer), coagulation monitoring (PT/INR), drug-of-abuse testing, and a growing menu of multiplex respiratory and STI molecular panels.

- The POC diagnostics value chain operates across three distinct tiers. The foundational infrastructure layer — platforms, reagent manufacturing, and connectivity middleware — is dominated by Abbott Laboratories (i-STAT, ID NOW, ARCHITECT), F. Hoffmann-La Roche Ltd. (cobas Liat, cobas h 232, CoaguChek), and Siemens Healthineers AG (CLINITEST Rapid COVID-19 Antigen Test, Xprecia Stride coagulation system). The specialist integration layer includes Danaher Corporation through Cepheid (GeneXpert platform, Xpert Xpress assay menu) and QuidelOrtho Corporation (Sofia 2, VITROS), which bridge platform capability into specific disease-area networks. The application-layer specialists — EKF Diagnostics, Nova Biomedical, Werfen, and Sysmex — target high-precision clinical niches including hematology, blood gas analysis, and immunohematology in acute care settings.

- For procurement and investment decision-makers, the distinction that matters is not whether the Point-of-Care Diagnostics market will grow — that question is settled — but which segments, geographies, and deployment models will capture disproportionate value within that growth. This report provides sub-segment level data, country-level forecasts, and competitive positioning analysis across five segmentation dimensions and 35+ geographies, enabling precise allocation of procurement budgets, investment theses, and market-entry strategies.

Key Insights

- The Global Point-of-Care Diagnostics market registers a 9.9% CAGR over 2026–2034, growing from USD 42,180 Mn to USD 98,640 Mn, according to Zion Market Research — outpacing the broader IVD sector growth rate.

- Infectious disease testing is the dominant product segment, accounting for an estimated 30–35% of 2025 global revenue, driven by sustained post-pandemic demand for rapid respiratory, STI, and vector-borne disease detection assays.

- Molecular diagnostics is the fastest-growing technology sub-segment, expanding at approximately 10–12% CAGR as CLIA-waived PCR panels reach physician offices and urgent care clinics previously served only by antigen-based tests.

- Hospitals are the dominant end-user category, holding an estimated 40%+ revenue share in 2025 through their role in acute care delivery, ICU-based critical biomarker monitoring, and emergency medicine diagnostic workflows.

- Home settings are the fastest-growing end-user segment, driven by aging populations, chronic disease self-management trends, and rising consumer acceptance of direct-to-consumer glucose, pregnancy, and STI testing formats.

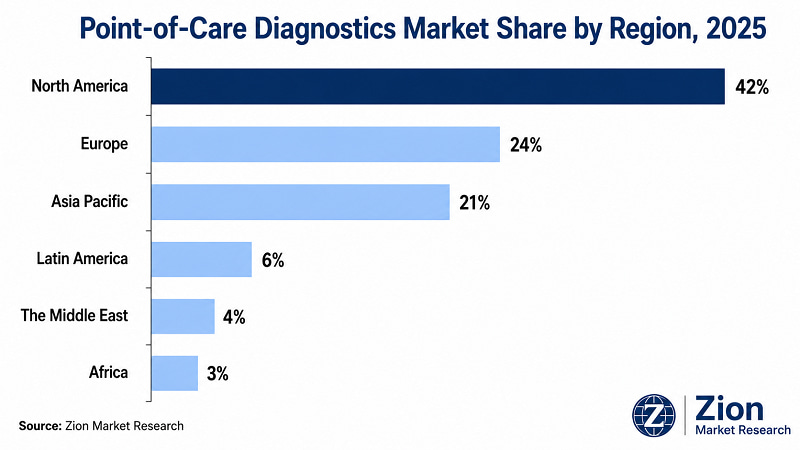

- North America leads by regional revenue share at approximately 42% in 2025, supported by advanced reimbursement infrastructure, FDA expedited clearance pathways, and a concentrated manufacturing and R&D base.

- Asia Pacific is the fastest-growing region at approximately 10.7% CAGR through 2034, driven by China's 36,000-unit township clinic network expansion, India's national health mission procurement programmes, and rising healthcare consumerism across ASEAN markets.

- The competitive landscape is semi-consolidated: Abbott and Roche jointly hold an estimated 30–35% combined revenue share, while the broader top-10 cohort is intensifying M&A activity around high-margin molecular POC platforms.

- By 2034, molecular POC assays — enabled by CLIA-waived status and cloud-connected device management — are expected to represent the largest incremental revenue category within the overall POC diagnostics market.

Why Choose the Zion Market Research's Point-of-Care Diagnostics Market Report?

Decision-makers comparing market intelligence reports on Point-of-Care Diagnostics will find the Zion Market Research's report differentiated on the following dimensions.

|

Dimension |

Zion Market Research Report |

Industry Average |

|

Report Pages |

300+ |

~120 pages |

|

Forecast Horizon |

9 years (2026–2034) |

7 years |

|

Segmentation Dimensions |

5 dimensions |

4–5 dimensions |

|

Historical Data |

6 years (2019–2025) |

4–5 years |

|

Country Coverage |

35+ countries |

15–18 countries |

|

Companies Profiled |

15 companies |

10 companies |

|

DROC Framework |

Full (Drivers, Restraints, Opportunities, Challenges) |

Drivers only |

**For custom scope — additional segments, specific geographies, or extended forecast periods — contact sales@zionmarketresearch.com

Point-of-Care Diagnostics Market: Dynamics (Drivers, Restraints, Opportunities, Challenges)

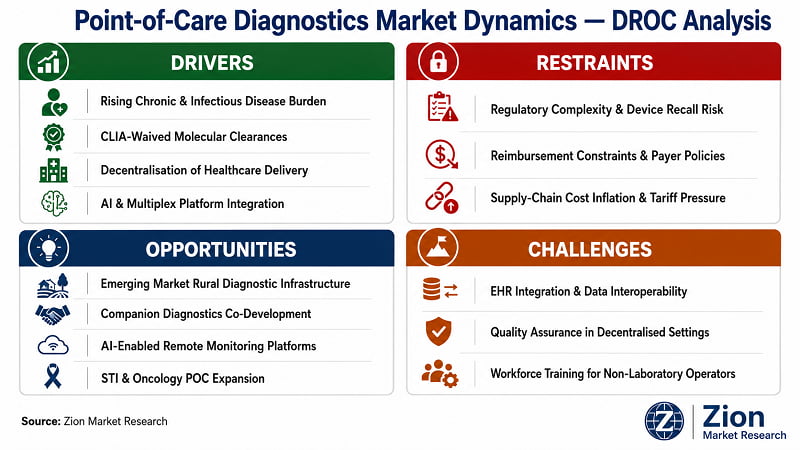

What Is Driving the Point-of-Care Diagnostics Market?

- Rising Global Chronic & Infectious Disease Burden — the primary demand catalyst:

537 million adults globally were living with diabetes in 2024, according to the International Diabetes Federation — a figure the IDF projects to reach 643 million by 2030. This sustained demand-side dynamic drives glucose testing as the single largest product sub-segment within POC diagnostics. Beyond metabolic disease, infectious disease pressures compound the demand signal: dengue outbreaks across Southeast Asia, resurgent tuberculosis in Sub-Saharan Africa, and persistent respiratory pathogen activity in temperate climates have pushed government procurement agencies toward stockpiling rapid diagnostic tests. WHO prequalified 12 new malaria rapid tests in 2025, reflecting active regulatory pipeline activity in the infectious disease POC segment. Abbott supplied 15 million malaria tests to India's National Health Mission in 2025, covering districts where laboratory microscopy was unavailable in 40% of primary health centres — demonstrating the commercial-scale viability of POC in low-resource settings. The combined chronic and infectious disease burden creates a demand structure that's secular, not cyclical, positioning POC diagnostics for above-trend volume growth through the full 2026–2034 forecast horizon.

- Regulatory Acceleration — CLIA Waived Molecular Testing Creates New Market Segment:

The FDA's 510(k) expedited pathway cleared 47 new POC devices in 2024, a 22% year-on-year increase, fundamentally expanding the addressable market for near-patient testing. The critical structural change is the CLIA-waived status granted to eight molecular respiratory panels between 2024 and 2025 — including Cepheid's Xpert Xpress Flu/RSV and Roche's cobas Liat Influenza A/B & RSV — permitting deployment in physician offices without high-complexity laboratory certification. This matters financially: CMS reimburses CLIA-waived molecular assays at USD 45–75 per panel, creating a direct economic incentive for practices to upgrade from antigen-based lateral flow tests to higher-sensitivity PCR-class platforms. Cepheid shipped 2.3 million Xpert Xpress units in Q3 2024 — a 35% year-on-year surge that demonstrates how regulatory tailwind converts directly into manufacturing volume demand. In Europe, the European Medicines Agency granted CE-IVD marks to 12 new POC cardiac biomarker assays during 2024–2025, enabling one-hour myocardial infarction rule-outs in emergency departments — expanding the cardiac marker segment's premium ASP tier.

- Decentralisation of Healthcare Infrastructure — Structural Shift to Near-Patient Settings:

Health system economics across both developed and emerging economies are driving care from inpatient and centralised settings to ambulatory, home, and community-based environments. The COVID-19 pandemic provided a proof-of-concept for massively deployed decentralised testing at scale — an acceleration that permanently altered institutional procurement models. The U.S. government, through NIH and BARDA, has allocated over USD 2 billion to support diagnostic innovation with an explicit emphasis on decentralised deployment contexts: outpatient clinics, nursing homes, tribal clinics, and homes. BARDA awarded funding to Beckman Coulter in October 2025 to validate biomarkers for MIS-C detection through a multi-centre clinical trial — a signal of sustained government investment in POC infrastructure. Siemens Healthineers responded to this demand by expanding U.S. operations in May 2025 with a USD 150 million investment to strengthen manufacturing capacity, supply-chain resilience, and customer support. Supply-side investment of this scale confirms that vendors with institutional procurement access see decentralisation as a sustained, multi-year volume driver rather than a temporary market condition.

- AI Integration & Multiplex Platform Capability — Accelerating Adoption Velocity:

Artificial intelligence is transitioning from an experimental feature to an embedded analytical layer within POC diagnostics systems. AI-enhanced image interpretation is improving lateral flow assay accuracy by reducing operator-dependent read variability; multiplex signal deconvolution allows a single cartridge to detect and differentiate multiple pathogens simultaneously. QuidelOrtho's VITROS platform, for example, added high-sensitivity Troponin capability in Q3 2025, demonstrating how AI-assisted assay expansion increases per-instrument revenue without requiring hardware replacement. Cloud connectivity — which enables remote quality control, EHR integration, and real-time fleet monitoring across geographically distributed devices — has shifted from a premium feature to a procurement prerequisite for hospital networks. Manufacturers without robust digital capabilities face procurement exclusion, according to institutional procurement committee analyses. This creates a structural competitive filter that advantages vertically integrated platforms over standalone device vendors, driving consolidation and ASP improvement simultaneously.

- Key Takeaway:

"Our intended acquisition of LEX Diagnostics will strengthen and accelerate our presence in point-of-care molecular diagnostics — one of the largest and fastest-growing segments in the diagnostics industry. In comparing the results of recent clinical trial data, investment requirements, and the significant market opportunity for both the Savanna and LEX Diagnostics platforms, we determined that LEX Diagnostics offers important performance advantages for customers and is better aligned with our strengths."

— Brian J. Blaser, President and Chief Executive Officer, QuidelOrtho Corporation

(Source: QuidelOrtho Corporation Press Release, June 2025)

What Is Restraining the Point-of-Care Diagnostics Market?

- Regulatory Complexity & Device Recall Risk — Eroding Procurement Confidence:

The FDA issued Class I recalls for 3.7 million TRUEresult and TRUEtrack glucose meters in May 2024 following software errors producing falsely elevated readings in hypoglycemic patients — a patient safety incident with direct commercial consequences. Abbott followed with a voluntary recall of 3.6 million FreeStyle Libre 2 readers in October 2024 due to battery overheating risks. Such high-profile recalls erode clinician confidence and force hospital procurement committees to demand third-party accuracy audits before approving new platform deployments, extending sales cycles and increasing compliance costs for manufacturers. In Europe, the IVDR deadline of May 2025 removed approximately 30% of legacy POC devices from the market — a simultaneous supply disruption that hit healthcare providers dependent on uncertified platforms hardest in France, Italy, and Eastern European markets, where notified-body audit capacity is more constrained.

- Reimbursement Constraints & Payer Policy Tightening — Restricting Outpatient Volume:

Private insurers, including Anthem, introduced prior authorisation rules limiting respiratory pathogen panels to high-risk patients, restricting volume in outpatient settings where the growth opportunity is most pronounced. This policy shift creates a bifurcated market dynamic: hospital-based testing — where reimbursement is broader — continues to grow, while outpatient and urgent care settings face volume constraints that suppress the per-episode economics that POC manufacturers use to justify platform investment. The restraint is most acute in the U.S. market, where reimbursement policy changes by major commercial payers can rapidly alter demand curves for specific test categories. European managed care structures in the UK's NHS and Germany's statutory health insurance system impose similar per-test cost controls that limit premium-ASP molecular POC assay adoption beyond high-acuity settings.

- Supply-Chain Cost Inflation & Tariff Disruption — Margin Compression Across the Value Chain:

Certain diagnostic reagents and laboratory supplies are now subject to U.S. import duties as high as 25% or more depending on classification and country of origin — raising the landed cost of critical inputs for manufacturers sourcing internationally. The U.S. Bureau of Economic Analysis reported a 2.6% year-on-year increase in the Personal Consumption Expenditures price index for medical care services in June 2025, confirming healthcare-specific inflation above headline rates. A 2024 report on healthcare supply chain challenges found that geopolitical instability contributed to a 2.9% annual rise in supply chain costs driven largely by rising logistics and component costs. These pressures compress distributor margins and raise per-test costs for laboratories and healthcare providers — reducing accessibility and dampening adoption in price-sensitive emerging markets where the volume growth opportunity is largest.

- Key Takeaway:

"Achieving uniform regulatory standards is a significant challenge. Low-resource settings often lack the infrastructure for consistent test quality assurance — this may lead to inconsistent test results and slow adoption rates in markets where the clinical need is highest."

— Regulatory analysis on POC diagnostics standardisation in low-resource settings

(Source: Renub Research, Point-of-Care Diagnostics Market Analysis, 2025)

What Opportunities Exist in the Point-of-Care Diagnostics Market?

- Emerging Market Rural Diagnostic Infrastructure — Large Underserved TAM:

China's NMPA clearance of Roche's cobas Liat system in 2024 unlocked access to 36,000 township health centres serving 600 million rural residents — a single regulatory event that created a commercially accessible TAM previously unreachable by laboratory-grade molecular diagnostics. India's National Health Mission, with a population of 1.4 billion and 40% of primary health centres lacking laboratory microscopy, represents a structurally similar opportunity at scale. The Asian Development Bank reported in June 2025 that over 20 countries in Asia face a 20% or greater risk of premature death from chronic diseases — a public health imperative that is converting into POC procurement mandates across national health ministries. ASEAN-based manufacturers, including SD Biosensor (South Korea), are positioning for this opportunity through ruggedised, battery-operated platforms designed for environments with limited cold-chain and power infrastructure.

- Companion Diagnostics Co-Development — Premium Revenue Stream:

The POC diagnostics sector is the fastest-emerging companion diagnostic deployment channel for pharmaceutical R&D pipelines. Molecular assay platforms with multiplex capability are shortening clinical trial site qualification timelines by eliminating the need for centralised laboratory infrastructure at trial sites. The FDA's framework for companion diagnostic co-approval creates a locked platform-assay revenue relationship: once a drug is approved with a specific POC companion diagnostic, the test becomes a mandated procurement item for prescribing institutions. With oncology and infectious disease as the two highest-priority therapeutic areas for pharma R&D investment, POC diagnostics manufacturers with CE-marked or FDA-cleared oncology biomarker assays are well-positioned to secure premium, high-margin, long-cycle commercial contracts.

- AI-Enabled Remote Patient Monitoring Integration — Platform Value Expansion:

The integration of wearable biosensors with POC diagnostic platforms is creating a new revenue tier: continuous monitoring devices that generate real-time data streams accessible by both patients and clinicians. Abbott's FreeStyle Libre CGM platform — despite its 2024 recall — demonstrated the commercial scale achievable through direct-to-consumer CGM: the product generated multi-billion dollar revenues by making glucose monitoring a daily consumer habit rather than a periodic clinical event. The same model is being applied to cardiac biomarkers, oxygen saturation, and inflammatory markers. Cloud connectivity from POC platforms into EHR systems enables remote quality control, outcome tracking, and population health analytics — capabilities that health systems are willing to pay premium prices for as value-based care contracts link reimbursement to outcome metrics.

- STI & Oncology Point-of-Care Expansion — Next-Growth Segment:

Roche gained FDA 510(k) clearance and CLIA waiver for its cobas Liat STI multiplex assay panels in January 2025 — expanding POC molecular testing into the sexually transmitted infection category, where point-of-care testing can enable same-visit diagnosis and treatment, reducing transmission, follow-up costs, and antimicrobial resistance risk. The global STI testing market represents a multi-billion dollar incremental TAM for POC molecular platforms. In oncology, loop-mediated isothermal amplification (LAMP) and multiplexed lateral flow immunoassay technologies are enabling high-sensitivity detection of cancer biomarkers without complex laboratory infrastructure — a technically validated approach now being commercialised by a cohort of specialist developers targeting low- and middle-income country markets.

What Challenges Does the Point-of-Care Diagnostics Market Face?

- EHR Integration & Data Interoperability — The Connectivity Gap:

Procurement committees at major hospital systems increasingly specify EHR integration and remote quality-control capability as mandatory requirements — not optional features. Manufacturers lacking robust digital capabilities face procurement exclusion regardless of assay performance. The interoperability challenge is compounded by fragmented EHR ecosystems: Epic, Cerner, and MEDITECH each require device-specific interface development, raising integration costs for POC manufacturers. In emerging markets, where digital health infrastructure is less mature, the absence of reliable internet connectivity renders cloud-connected device management features commercially irrelevant, requiring manufacturers to maintain parallel product lines — adding R&D cost and supply-chain complexity.

- Quality Assurance in Decentralised Settings — Operator Training & Error Rates:

Moving molecular-grade testing out of centralised laboratories introduces operator skill and quality control risks that do not exist in supervised laboratory environments. Lateral flow tests — despite their simplicity — show higher error rates when interpreted visually by non-laboratory personnel. Regulatory frameworks, including CLIA in the U.S. and equivalent standards in Europe, impose quality control requirements that add operational cost for non-laboratory settings. Inconsistent test results from poorly trained operators can undermine clinical trust in POC platforms, particularly in settings where incorrect diagnostic decisions have serious therapeutic consequences — sepsis diagnosis, cardiac biomarker interpretation, and drug-of-abuse screening among them.

- Workforce Training for Non-Laboratory Operators — Last-Mile Adoption Barrier:

Deploying POC diagnostics in primary care clinics, pharmacies, and home settings requires training non-laboratory personnel — nurses, pharmacists, community health workers — to perform tests previously conducted by trained laboratory technicians. This training requirement adds an adoption barrier that slows the conversion from sample-to-test intention to operational POC deployment, particularly in markets where health workforce capacity is constrained. Platform manufacturers are addressing this through user interface simplification, automated quality control systems, and connectivity-enabled remote troubleshooting — but the workforce challenge remains a material friction point in the last-mile adoption equation across both developed and emerging markets.

Point-of-Care Diagnostics Market: Report Scope

|

Attribute |

Detail |

|

Report Name |

Global Point-of-Care Diagnostics Market — Analysis & Forecast, 2026–2034 |

|

Market Size in 2025 |

USD 42,180 Mn |

|

Market Forecast in 2034 |

USD 98,640 Mn |

|

Growth Rate (CAGR) |

9.9% (2026–2034) |

|

Historical Data Period |

2019–2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026–2034 |

|

Number of Pages |

300+ |

|

Tables & Figures |

110 tables, 80 figures |

|

Report Code |

ZMR-0000 |

|

Report Format |

|

|

Delivery Format |

Immediate Digital Download (PDF) |

|

Published Date |

May 2026 |

|

Research Methodology |

Primary Research + Secondary Research + Data Triangulation |

|

Key Companies Covered |

Abbott Laboratories | F. Hoffmann-La Roche Ltd. | Siemens Healthineers AG | Danaher Corporation (Cepheid) | QuidelOrtho Corporation | BD | Thermo Fisher Scientific Inc. | bioMérieux SA | QIAGEN N.V. | Bio-Rad Laboratories Inc. | EKF Diagnostics Holdings plc | Trinity Biotech plc | Sysmex Corporation | Nova Biomedical | Werfen |

|

Segments Covered |

By Product | By Technology | By Mode of Purchase | By End User | By Region |

|

Regions Covered |

North America | Europe | Asia Pacific | Latin America | The Middle East | Africa |

|

Customization Scope |

10% free customization with purchase. Contact sales@zionmarketresearch.com for extended scope options. |

Point-of-Care Diagnostics Market: Segmentation

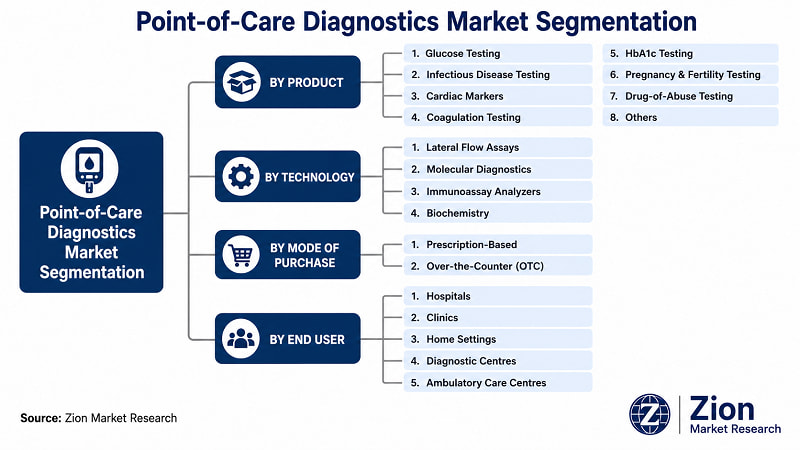

The Global Point-of-Care Diagnostics market is segmented by product, technology, mode of purchase, end user, and region.

- By Product

The product dimension encompasses eight categories: glucose testing, infectious disease testing, cardiac markers, coagulation testing, HbA1c testing, pregnancy & fertility testing, drug-of-abuse testing, and others. Infectious disease testing dominates, accounting for an estimated 30–35% of 2025 global revenue — a position reinforced by sustained post-pandemic procurement and the ongoing burden of dengue, malaria, tuberculosis, and influenza. The infectious disease sub-segment benefits from the highest assay innovation velocity, with WHO prequalifying 12 new malaria rapid tests in 2025 alone. Glucose testing holds the second-largest share, driven by 537 million adults globally living with diabetes and the consumer-grade adoption of self-monitoring platforms. Cardiac markers are the fastest-growing product sub-segment at the premium ASP tier, as CE-IVD marks for 12 new POC cardiac biomarker assays granted by EMA in 2024–2025 enable one-hour myocardial infarction rule-outs in emergency departments — converting a previous centralised lab workflow to a near-patient setting.

- By Technology

The technology dimension includes lateral flow assays, molecular diagnostics, immunoassay analyzers, and biochemistry. Lateral flow assays (LFAs) hold the dominant technology share — estimated at 40–45% of 2025 global volume — through their unmatched combination of simplicity, low cost, and deployability in resource-limited settings. They remain the backbone of infectious disease and pregnancy testing at scale. Molecular diagnostics is the fastest-growing technology segment, expanding at approximately 10–12% CAGR, driven by CLIA-waived PCR panel adoption in physician offices and urgent care clinics. Cepheid's GeneXpert MTB/RIF Ultra assay shortened tuberculosis time-to-treatment in South African clinics from 14 days to under 2 hours — a clinical outcome metric that drives institutional procurement decisions across public health settings. Abbott's ID NOW platform, delivering results in 13 minutes, set the commercial standard for molecular POC speed and is the dominant platform in U.S. decentralised molecular testing.

- By Mode of Purchase

The mode of purchase dimension comprises prescription-based and over-the-counter (OTC) products. Prescription-based testing dominates, reflecting the majority of POC diagnostic volume flowing through clinical settings — hospitals, clinics, and diagnostic centres — where physician authorisation governs procurement. Prescription-based platforms typically carry higher per-test revenue through insurance reimbursement and institutional supply contracts. The OTC segment is the fastest-growing mode, driven by rising consumer demand for self-testing in glucose monitoring, pregnancy, STI, and rapid COVID-19 detection. The CLIA-waived status for home-use molecular tests — including Aptitude Medical Systems' Metrix COVID/Flu multiplex test, which received FDA EUA in February 2025 for CLIA-waived and home settings — is progressively blurring the boundary between clinical and consumer diagnostic categories.

- By End User

The end-user dimension covers hospitals, clinics, home settings, diagnostic centres, and ambulatory care centres. Hospitals are the dominant end-user category, holding an estimated 40%+ revenue share in 2025, driven by their role as primary deployment sites for high-acuity tests including cardiac biomarkers, coagulation monitoring, blood gas analysis, and sepsis biomarkers. Abbott's i-STAT and Roche's cobas Liat are commonly deployed across ICU, ER, and maternity care departments in major health systems. Home settings are the fastest-growing end-user segment — a trend accelerated by the COVID-19 pandemic and sustained by aging population demographics, chronic disease self-management priorities, and rising healthcare consumerism. Diagnostic centres led the non-hospital category with approximately 35–36% of market revenue in 2024–2025 through specialised rapid diagnostic services across medical disciplines.

Point-of-Care Diagnostics Market: Regional Analysis

North America dominates the Global Point-of-Care Diagnostics market with approximately 42% revenue share in 2025. Asia Pacific is the fastest-growing region at an estimated 10.7% CAGR through 2034, driven by government-mandated rural health infrastructure programmes in China and India and rising healthcare consumerism across ASEAN markets. The structural reason for North America's dominance is a combination of factors that are difficult to replicate quickly: a mature reimbursement framework that covers molecular-class POC assays at premium price points, a concentrated manufacturing and R&D base that enables rapid innovation cycles, and a clinical culture that has historically adopted new diagnostic technologies faster than any other region.

- North America Point-of-Care Diagnostics Market

North America commands approximately 42% of 2025 global POC diagnostics revenue, with the U.S. representing the dominant driver through its advanced reimbursement infrastructure, high disease prevalence, and a deep concentration of POC platform manufacturers and distributors. The FDA's expedited 510(k) clearance pathway approved 47 new POC devices in 2024 — 22% more than the prior year — and the CLIA-waived status granted to eight molecular respiratory panels between 2024 and 2025 has structurally expanded the outpatient molecular POC market. CMS reimbursement of CLIA-waived molecular assays at USD 45–75 per panel creates the economic incentive for physician office and urgent care centre platform upgrades. Canada is expanding digital-connected POC platforms in emergency department settings; Mexico is increasing diagnostic network density through government public health programmes focused on diabetes and infectious disease management. One challenge across the region is the tariff-driven cost inflation for reagents and components sourced internationally, which is compressing manufacturer margins and raising per-test costs.

- Europe Point-of-Care Diagnostics Market

Europe's POC diagnostics market is navigating the disruptive transition to the EU In Vitro Diagnostic Regulation (IVDR), which removed approximately 30% of legacy POC devices from the European market by its May 2025 deadline — creating both a procurement challenge for healthcare providers dependent on non-certified platforms and a commercial opportunity for IVDR-compliant alternatives. Germany leads European adoption, having expanded reimbursement for patient-managed INR testing and positioned itself as the primary market entry point for U.S. and Asian POC manufacturers seeking European regulatory clearance. The UK's National Health Service deployed Roche cobas Liat units across 200 general practices specifically to curb inappropriate antibiotic prescribing — a use-case-driven procurement model that is influencing NHS Scotland and NHS Wales procurement strategies. France, Italy, and Spain represent the secondary tier of European adoption, with growing interest in cardiac biomarker and respiratory molecular POC platforms. The regulatory headwind from IVDR compliance costs remains a material challenge particularly for smaller European manufacturers.

- Asia Pacific Point-of-Care Diagnostics Market

Asia Pacific is the fastest-growing region for POC diagnostics globally, projected at approximately 10.7% CAGR through 2034. China's NMPA clearance of Roche's cobas Liat system in 2024 opened access to 36,000 township health centres serving 600 million rural residents — a market access event with transformative TAM implications for molecular POC platforms. India's National Health Mission distributed 15 million Abbott malaria rapid tests in 2025, demonstrating that government procurement mandates can drive POC volume at a scale that no commercial distribution network could replicate independently. Japan holds the second-largest revenue share within Asia Pacific in 2025, with a sophisticated clinical culture adopting CGM and AI-enabled diagnostic platforms. South Korea is a technology-forward adoption environment, particularly for molecular and immunoassay platforms. Australia is expanding coverage to CGM and AI-enabled diagnostics across its primary care network. ASEAN nations — Thailand, Indonesia, Vietnam, Malaysia, and the Philippines — represent the highest-potential volume growth markets, with rising healthcare awareness and government investments in diagnostic network expansion.

- Latin America Point-of-Care Diagnostics Market

Latin America's POC diagnostics market is led by Brazil, which accounts for the largest country-level revenue share in the region through its combination of a large population base, a substantial chronic disease burden, and an established public and private healthcare infrastructure that is actively expanding diagnostic access. Brazil's Unified Health System (SUS) procurement programmes have been a significant driver of rapid antigen test adoption for infectious diseases including dengue — endemic across multiple Brazilian states. Argentina, Colombia, Chile, and Peru follow as secondary markets with growing private-sector POC adoption driven by expanding diagnostic centre networks and rising middle-class demand for direct-to-consumer health monitoring. A regulatory challenge specific to the region is the fragmented national regulatory landscape: manufacturers must navigate country-by-country registration processes, adding time and cost to market-entry timelines relative to the harmonised EU and standardised FDA frameworks.

- The Middle East Point-of-Care Diagnostics Market

The Middle East is an emerging high-value POC diagnostics market, driven by GCC healthcare infrastructure investment programmes — particularly in Saudi Arabia under Vision 2030 and in the UAE where healthcare modernisation is a stated national priority. The GCC countries (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, and Oman) represent the primary revenue-generating sub-region, with hospital systems actively upgrading from manual and centralised laboratory workflows to connected POC platforms across emergency, ICU, and ambulatory settings. Israel is a technology-forward market for POC diagnostics and molecular testing, with a strong domestic diagnostics industry and active integration of AI-enhanced platforms. Turkey is an important market for affordable rapid antigen and lateral flow platforms across its extensive public hospital network. Iran remains an underserved market with a significant disease burden but limited access to premium POC technology due to trade restrictions. The Middle East's POC market growth is supported by rising diabetes prevalence across the GCC — the region has one of the world's highest diabetes rates — and government-mandated infectious disease surveillance programmes.

- Africa Point-of-Care Diagnostics Market

Africa represents one of the highest-unmet-need markets for POC diagnostics globally, with a disease burden dominated by infectious diseases — malaria, tuberculosis, HIV, and an increasing chronic disease overlay from diabetes and cardiovascular disease — that POC testing is uniquely well-positioned to address. South Africa is the largest and most sophisticated POC diagnostics market on the continent, with Cepheid's GeneXpert MTB/RIF Ultra assay having shortened tuberculosis time-to-treatment in South African clinics from 14 days to under 2 hours — a validated clinical outcome that has driven national TB programme procurement mandates. Egypt and Nigeria are the next largest markets, with both countries investing in public health diagnostic infrastructure supported by multilateral funding from organisations including the WHO, Gavi, and the Global Fund. WHO prequalified 12 new malaria rapid tests in 2025, enabling procurement agencies to source assays meeting stringent sensitivity thresholds for low-parasitemia detection — a direct enabler for African public health programme procurement at scale. The primary challenge for commercial POC vendors in Africa remains the infrastructure gap: power reliability, cold-chain requirements, and internet connectivity are variable across sub-national geographies, necessitating ruggedised, low-power platform designs.

Full Country Coverage

|

Region |

Countries Covered |

|

North America |

The U.S., Canada, Mexico |

|

Europe |

Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe |

|

Asia Pacific |

China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific |

|

Latin America |

Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America |

|

The Middle East |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

Africa |

South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa |

**Country-level market sizing, historical data, and forecasts available for all geographies listed. Custom regional add-ons available — contact sales@zionmarketresearch.com

Point-of-Care Diagnostics Market: Competitive Landscape

- The Global Point-of-Care Diagnostics market is semi-consolidated, with the top five players — Abbott Laboratories, F. Hoffmann-La Roche Ltd., Siemens Healthineers AG, Danaher Corporation (Cepheid), and QuidelOrtho Corporation — collectively holding an estimated 50–60% of global revenue. The dominant strategic pattern is platform breadth combined with digital connectivity: the vendors winning institutional procurement contracts are those that offer a full menu of assays across multiple disease categories on a single connected platform, reducing the number of separate vendor relationships that healthcare systems must manage. M&A is the primary vehicle for menu expansion, with QuidelOrtho's 2025 acquisition of LEX Diagnostics and Siemens Healthineers' USD 150 million U.S. manufacturing investment both signalling continued consolidation momentum.

- Key players operating in the Global Point-of-Care Diagnostics market include Abbott Laboratories (USA), F. Hoffmann-La Roche Ltd. (Switzerland), Siemens Healthineers AG (Germany), Danaher Corporation / Cepheid (USA), QuidelOrtho Corporation (USA), BD — Becton Dickinson (USA), Thermo Fisher Scientific Inc. (USA), bioMérieux SA (France), QIAGEN N.V. (Netherlands), Bio-Rad Laboratories Inc. (USA), EKF Diagnostics Holdings plc (UK), Trinity Biotech plc (Ireland), Sysmex Corporation (Japan), Nova Biomedical (USA), and Werfen (USA).

|

Company |

HQ |

Primary Focus |

Key Strategy |

Notable Recent Action |

|

Abbott Laboratories |

USA |

Glucose, Molecular, Infectious Disease |

Broad platform + digital integration |

ID NOW CLIA-waived molecular expansion; i-STAT TBI cartridge FDA clearance (Apr 2024) |

|

F. Hoffmann-La Roche Ltd. |

Switzerland |

Molecular POC, Cardiac, Coagulation |

PCR accuracy at point of care; navify connectivity |

cobas Liat STI assay FDA clearance (Jan 2025); NMPA China clearance (2024) |

|

Siemens Healthineers AG |

Germany |

Blood gas, Cardiac, Urinalysis |

Digital health integration; EHR connectivity |

USD 150 Mn U.S. manufacturing expansion (May 2025); India MedGenome partnership (Dec 2024) |

|

Danaher / Cepheid |

USA |

Molecular POC (GeneXpert) |

CLIA-waived molecular expansion; TB/respiratory focus |

2.3 Mn Xpert Xpress units shipped Q3 2024 (35% YoY growth) |

|

QuidelOrtho Corporation |

USA |

Immunoassay, Cardiac, Molecular |

Molecular POC strategy pivot; M&A |

LEX Diagnostics acquisition (2025); USD 140 Mn cost savings achieved |

|

BD (Becton Dickinson) |

USA |

Rapid antigen, Infectious Disease |

Pharmacy & outpatient channel expansion |

BD Veritor Plus global expansion (Jan 2025) |

|

Thermo Fisher Scientific |

USA |

Molecular, Biochemistry |

R&D and specialty assay development |

Ongoing molecular POC platform investment |

|

bioMérieux SA |

France |

Respiratory Molecular, Microbiology |

Near-patient molecular solutions |

Respiratory POC portfolio expansion; BIOFIRE platform |

|

QIAGEN N.V. |

Netherlands |

Portable molecular systems |

Diverse assay menu; field-deployable platforms |

QIAstat-Dx syndromic testing expansion |

|

Bio-Rad Laboratories |

USA |

Immunoassay, Quality Controls |

Quality assurance and immunoassay |

EQAS external quality assurance program for POC |

|

EKF Diagnostics Holdings |

UK |

Hematology, POC Biochemistry |

Niche clinical chemistry; HbA1c & lactate |

Biosen C-Line analyzer market expansion |

|

Trinity Biotech plc |

Ireland |

Infectious Disease Rapid Tests |

Emerging market rapid test supply |

HIV and infectious disease rapid test distribution |

|

Sysmex Corporation |

Japan |

Hematology, Urinalysis |

High-precision clinical niches |

POC hematology expansion in Asia Pacific |

|

Nova Biomedical |

USA |

Blood Gas, Electrolytes, Metabolites |

Critical care POC precision testing |

StatStrip glucose and lactate hospital expansion |

|

Werfen |

USA |

Coagulation, Immunohematology |

Critical care hemostasis testing |

GEM Premier 7000 acoustofluidics collaboration with AcouSort (Aug 2024) |

- Across the competitive set, four strategic themes are consistent: (1) molecular POC is the highest-priority growth investment category; (2) digital connectivity and EHR integration are now mandatory, not optional, platform requirements; (3) M&A is accelerating as vendors compete to acquire menu breadth and assay IP faster than organic R&D allows; and (4) emerging market localisation — ruggedised platforms, local regulatory clearances, and government procurement relationships — is the next frontier for volume-led market share gains.

Recent Developments in the Point-of-Care Diagnostics Market

Strategic activity in the Global Point-of-Care Diagnostics market has accelerated significantly through 2024–2025, with M&A, regulatory milestones, and product launches reshaping the competitive landscape across molecular, cardiac, and infectious disease testing categories.

|

Date |

Company |

Type |

Description |

Market Impact |

|

Jan 2025 |

Roche Diagnostics |

Product Launch / Regulatory |

cobas Liat STI multiplex assay panels received FDA 510(k) clearance and CLIA waiver for point-of-care STI diagnosis including Chlamydia and Gonorrhea |

Expands molecular POC menu into the STI category; enables same-visit diagnosis and treatment across urgent care and sexual health clinics |

|

Jan 2025 |

BD (Becton Dickinson) |

Product Expansion |

Global expansion of BD Veritor Plus platform for rapid COVID-19 and influenza combo testing across pharmacies and outpatient settings |

Strengthens BD's position in the pharmacy and outpatient rapid antigen channel; extends global installed base |

|

May 2025 |

Siemens Healthineers |

Investment |

USD 150 million U.S. operations expansion — new and upgraded manufacturing facilities across multiple states to boost capacity and customer support |

Signals vendor confidence in sustained North America demand; improves supply-chain resilience for hospital system procurement |

|

Jun 2025 |

QuidelOrtho Corporation |

M&A / Strategy |

Announced intended acquisition of LEX Diagnostics for its ultra-fast molecular diagnostics platform to strengthen POC molecular presence |

Accelerates QuidelOrtho's molecular POC positioning; LEX platform offers performance advantages over prior Savanna platform |

|

Oct 2025 |

BARDA / Beckman Coulter |

Research Funding / Investment |

BARDA awarded funding to Beckman Coulter to validate effectiveness of biomarker for MIS-C detection through a large multi-centre clinical trial |

Demonstrates continued U.S. government investment in POC diagnostic infrastructure; validates biomarker-driven POC expansion |

|

Feb 2025 |

Aptitude Medical Systems |

Regulatory |

Metrix COVID/Flu multiplex test received FDA Emergency Use Authorization — first molecular POC test cleared for CLIA-waived and home settings for flu A, flu B, and SARS-CoV-2 differentiation in 20 minutes |

Expands home-based molecular POC market; removes last major barrier between clinical-grade molecular accuracy and consumer self-testing |

About Zion Market Research

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is updated constantly in order to fulfil our clients' requirements for prompt and direct online access. Keeping in mind the client's needs, we have included expert insights on global industries, products, and market trends in this database.

Author:

Mr. Nilesh Patil

Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067

Table Of Content

Methodology

FrequentlyAsked Questions

The Zion Market Research's Global Point-of-Care Diagnostics Market report comprises 300+ pages covering: full market sizing and forecasting for 2019–2034 across five segmentation dimensions (product, technology, mode of purchase, end user, and region); 110 data tables and 80 figures; 15 company profiles with competitive strategy analysis; country-level forecasts for 35+ geographies across all six Zion Market Research regions; full DROC analysis (drivers, restraints, opportunities, challenges); research methodology documentation; and recent developments table covering 2024–2025 strategic events. The report is delivered in PDF format with immediate digital download.

According to Zion Market Research, the Global Point-of-Care Diagnostics market was valued at USD 42,180 Mn in 2025 and is projected to reach USD 98,640 Mn by 2034, expanding at a CAGR of 9.9% during the forecast period 2026–2034. Historical data covers 2019–2025. North America leads with approximately 42% revenue share; Asia Pacific is the fastest-growing region at approximately 10.7% CAGR. Infectious disease testing is the dominant product segment.

The report segments the market across five dimensions: (1) By Product — glucose testing, infectious disease testing, cardiac markers, coagulation testing, HbA1c testing, pregnancy & fertility testing, drug-of-abuse testing, and others; (2) By Technology — lateral flow assays, molecular diagnostics, immunoassay analyzers, and biochemistry; (3) By Mode of Purchase — prescription-based and over-the-counter; (4) By End User — hospitals, clinics, home settings, diagnostic centres, and ambulatory care centres; (5) By Region — six ZMR regions covering 35+ countries.

The report provides country-level analysis across 35+ geographies. North America: The U.S., Canada, Mexico. Europe: Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe. Asia Pacific: China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific. Latin America: Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America. The Middle East: GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East. Africa: South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa. The Middle East and Africa are always covered as separate regions — never combined.

Zion Market Research offers 10% free customization with every report purchase — allowing buyers to specify additional segments, specific country breakdowns, or adjusted forecast scenarios at no extra cost. Beyond 10%, paid customization is available including: extended forecast periods (post-2034); additional country-level deep-dives not included in the standard scope; competitor-specific analysis; and primary research add-ons including executive interviews with specific stakeholder types. Contact sales@zionmarketresearch.com or call +1 (302) 444-0166 to discuss your specific customisation requirements.

Three options are available: (1) Free Sample: Access sample chapters, key data tables, and the condensed TOC (2) Full Report: Purchase the complete 300+ page PDF (3) Custom Research Inquiry: Contact the ZMR team directly at sales@zionmarketresearch.com | +1 (302) 444-0166 | Toll Free: +1 (855) 465-4651 to discuss multi-user licensing, enterprise access, or custom scope requirements.

List of Contents

Point-of-Care Diagnostics Industry Perspective:Point-of-Care Diagnostics OverviewKey InsightsWhy Choose the Zion Market ResearchsPoint-of-Care Diagnostics Market Report?Point-of-Care Diagnostics Dynamics (Drivers, Restraints, Opportunities, Challenges)Point-of-Care Diagnostics Report ScopePoint-of-Care Diagnostics SegmentationPoint-of-Care Diagnostics Regional AnalysisFull Country CoveragePoint-of-Care Diagnostics Competitive LandscapeRecent Developments in theMarketHappyClients