Mental Health Digital Therapeutics Market Size, Share, Trends & Forecast 2026–2034

Global Mental Health Digital Therapeutics Market by Product Type (Software-Based DTx, Device-Based DTx), by Therapeutic Area (Depression & Anxiety, Substance Use Disorders, PTSD & Trauma, ADHD, Schizophrenia & Psychosis, Others), by Delivery Platform (Mobile Applications, Web-Based Platforms, Wearable Devices, VR/AR Solutions), by End User (Patients/Consumers, Healthcare Providers, Payers & Employers), and by Region — Global Industry Perspective, Comprehensive Analysis, and Forecast 2026–2034.-

| Market Size in 2025 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 5,640 Million | USD 42,870 Million | 25.3% | 2025 |

Mental Health Digital Therapeutics Market: Industry Perspective

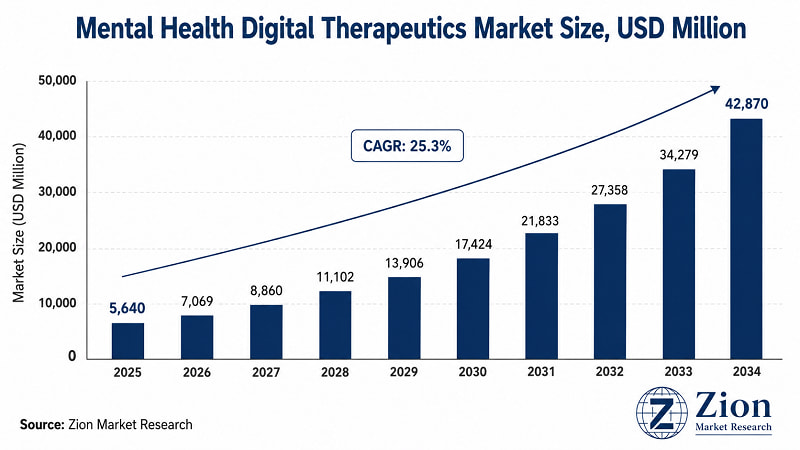

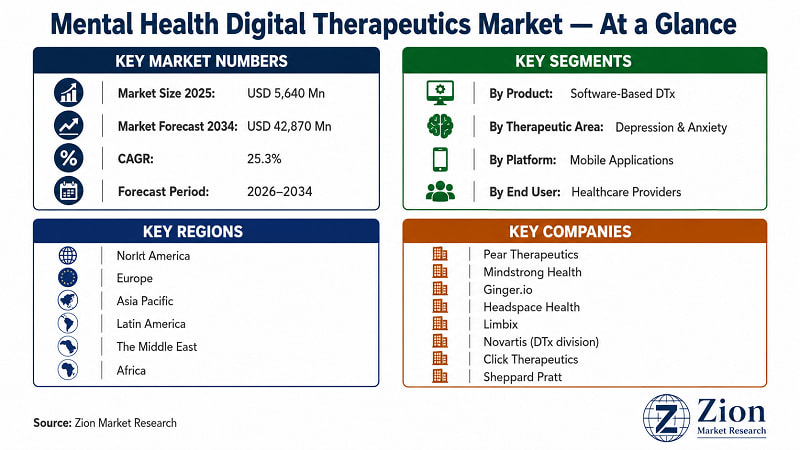

- The Global Mental Health Digital Therapeutics market stands at USD 5,640 Million in 2025 — a figure that represents only the earliest phase of what Zion Market Research projects will be a USD 42,870 Million industry by 2034.

- The 25.3% CAGR reflects three converging structural forces: the near-universal acknowledgement of a global mental health crisis, the digital infrastructure buildout accelerated by pandemic-era telehealth adoption, and a regulatory environment that has shifted from passive observation to active facilitation of DTx market access.

- The U.S. FDA has authorised multiple prescription DTx products. Germany's DiGA reimbursement scheme has created statutory coverage for approved digital therapeutics. Japan's PMDA has issued DTx-specific guidance.

- For procurement and investment decision-makers, the strategic question has moved from 'will DTx be reimbursed?' to 'which DTx categories will achieve the broadest payer coverage fastest?' — and the answer determines capital allocation for the next five years.

Mental Health Digital Therapeutics Market: Overview

- Mental Health Digital Therapeutics encompasses clinically validated software-driven interventions designed to prevent, manage, or treat diagnosable mental health conditions — delivered via mobile applications, web-based platforms, wearable devices, and immersive VR/AR environments. The scope includes prescription digital therapeutics (PDTs) requiring FDA or equivalent regulatory clearance, as well as clinically supported over-the-counter digital tools used by healthcare providers, payers, employers, and individual patients.

- The market value chain operates across three functional tiers. Foundational providers — including cloud infrastructure platforms (Amazon Web Services, Microsoft Azure), AI and NLP engine providers (Google DeepMind, IBM Watson Health), and clinical data network operators — form the technology substrate. Specialist developers such as Pear Therapeutics, Click Therapeutics, and Big Health operate at the integration tier, building regulatory-cleared DTx products on this infrastructure. Application-layer specialists — including Headspace Health, Woebot Health, and Spring Health — serve distinct vertical segments: employer wellness, consumer direct-to-patient, and healthcare-provider-integrated pathways respectively.

- For procurement and investment decision-makers, the distinction that matters is not whether Mental Health Digital Therapeutics will grow — that question is settled by clinical evidence, regulatory momentum, and payer economics — but which segments, geographies, and deployment models will capture disproportionate value within that growth. This report provides sub-segment level data, country-level forecasts, and competitive positioning analysis across 4 segmentation dimensions and 35+ geographies.

Key Insights

- The Global Mental Health Digital Therapeutics market registers a 25.3% CAGR over 2026–2034, growing from USD 5,640 Million (2025) to USD 42,870 Million (2034). Source: Zion Market Research.

- Software-Based DTx holds the dominant product segment share (~68%) in 2025, driven by scalable SaaS economics, lower regulatory barriers versus device-based DTx, and superior distribution through app stores and employer platforms.

- Mobile Applications lead the delivery platform segment with an estimated 57% share in 2025 — and are projected to remain dominant through 2034 due to smartphone penetration and consumer preference for asynchronous therapy access.

- Depression & Anxiety is the largest therapeutic area, accounting for an estimated 38% of total market value in 2025, supported by highest diagnosed prevalence rates and most mature clinical evidence base for DTx interventions.

- Healthcare Providers represent the fastest-growing end-user segment, as hospital systems and integrated delivery networks embed DTx into formal care pathways following FDA authorisations.

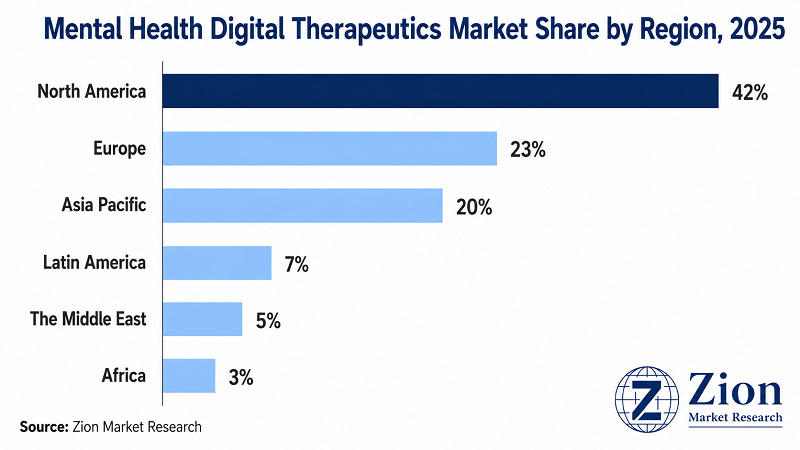

- North America holds an estimated 42% global market share in 2025, underpinned by the FDA's prescriber-pathway DTx framework, employer-channel infrastructure, and highest per-capita mental health spend.

- Asia Pacific registers the fastest regional CAGR, driven by China's digital health infrastructure investment, India's psychiatrist shortage creating structural demand for scalable DTx, and Japan's PMDA DTx guidance framework.

- The competitive landscape is bifurcating: pure-play clinical DTx companies (Pear, Click Therapeutics) face consolidation pressure from pharma incumbents (Novartis, Otsuka) entering via co-development partnerships.

- By 2030, employer-sponsored mental health DTx programmes are forecast to constitute over 30% of total end-user revenue — driven by measurable claims-cost reduction data from early payer adopters.

Why Choose the Zion Market Research's Mental Health Digital Therapeutics Market Report?

Decision-makers comparing market intelligence reports on Mental Health Digital Therapeutics will find the Zion Market Research report differentiated on the following dimensions.

|

Dimension |

Zion Market Research Report |

Industry Average |

|

Report Pages |

300+ |

~120 pages |

|

Forecast Horizon |

9 years (2026–2034) |

7 years |

|

Segmentation Dimensions |

4 dimensions |

2–3 dimensions |

|

Historical Data |

6 years (2019–2024) |

4–5 years |

|

Country Coverage |

35+ countries |

15–18 countries |

|

Companies Profiled |

15 companies |

10–12 companies |

|

DROC Framework |

Full (Drivers, Restraints, Opportunities, Challenges) |

Drivers only |

**For custom scope — additional segments, specific geographies, or extended forecast periods — contact sales@zionmarketresearch.com

Mental Health Digital Therapeutics Market: Dynamics (Drivers, Restraints, Opportunities, Challenges)

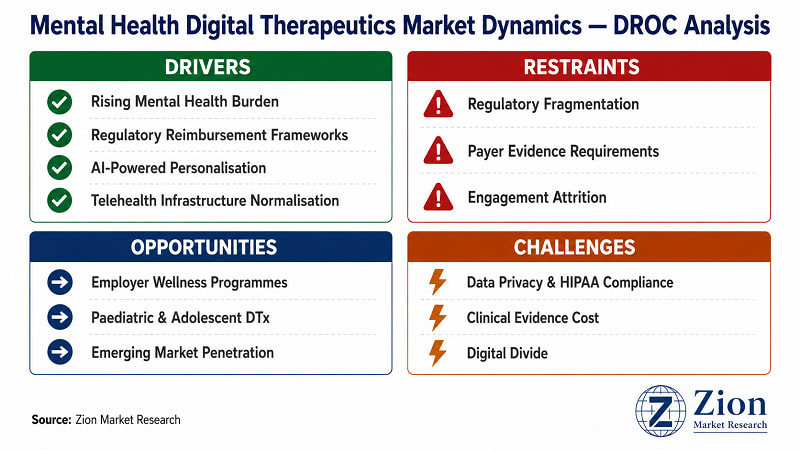

What Is Driving the Mental Health Digital Therapeutics Market?

- Rising Global Mental Health Burden and the Clinician-Scarcity Bottleneck:

The demand side of this market is structurally non-negotiable. The WHO estimates that 970 million people globally live with a mental health condition, yet fewer than half of those in high-income countries — and less than 10% in low-income countries — receive any treatment. The core supply-side headwind is clinician scarcity: the U.S. has a shortage of over 8,000 mental health practitioners as of 2024; India has fewer than 9,000 psychiatrists for 1.4 billion people. Digital therapeutics bypass this bottleneck by delivering structured, evidence-based protocols at marginal-cost-zero scale. Headspace Health reported serving over 100 institutional clients including major U.S. health systems by 2023, demonstrating that payer-driven institutional demand for scalable DTx already exists at commercial scale. The regulatory implication: DTx developers that can demonstrate clinical equivalence to in-person CBT protocols are positioned to capture payer budgets currently allocated to clinician-delivered care.

- Expanding Regulatory Reimbursement Pathways:

The establishment of reimbursement frameworks in the U.S., Germany, Japan, and Australia has transformed the commercial model for mental health DTx from direct-to-consumer subscription to institutionally purchased clinical tools. The FDA's De Novo pathway, which authorised Pear Therapeutics' reSET (substance use disorder) in 2017 and Freespira's PTSD application in 2019, established proof-of-concept for prescription DTx in mental health. Germany's DiGA framework reimbursed 53 digital health applications through statutory health insurers by end-2023, with mental health applications constituting the largest category. Click Therapeutics entered a co-development partnership with Otsuka Pharmaceutical in 2021 specifically to leverage the FDA prescription DTx pathway for major depressive disorder — citing reimbursement access as the primary commercial rationale. This regulatory tailwind structurally expands the TAM from individual consumer spend to institutional payer budgets, a category orders of magnitude larger.

- Artificial Intelligence and Adaptive Personalisation:

Third-generation mental health DTx platforms use machine learning to adapt therapeutic content based on real-time patient response data — moving beyond static protocol delivery to dynamic, personalised intervention pathways. This personalisation advantage is measurable: clinical studies on FDA-cleared DTx products demonstrate superior adherence rates and symptom-reduction outcomes compared to generic wellness apps. Natural language processing (NLP) integration enables continuous passive symptom monitoring through conversational AI interfaces — Woebot Health's NLP-driven chatbot had logged over 100 million conversational exchanges with users by 2023, generating a clinical dataset unavailable to any traditional mental health provider. The AI layer also enables population-level risk stratification for employer and payer clients — identifying high-risk employees for proactive outreach before acute episodes escalate to in-patient care. This preventive-use case is the strongest financial argument for employer adoption and represents a distinct revenue stream from the clinical treatment TAM.

- Telehealth Infrastructure Normalisation Post-Pandemic:

The COVID-19 pandemic permanently shifted patient expectations and provider capabilities around digital mental health delivery. Telehealth mental health visits in the U.S. increased from approximately 1% of all mental health encounters in 2019 to over 36% by 2021, according to data from the RAND Corporation. Critically, a significant proportion of that utilisation has been retained post-pandemic — patient comfort with asynchronous digital therapy tools has been established across age cohorts previously considered non-adopters. This normalisation effect lowers the patient-acquisition cost for DTx platforms and accelerates the adoption curve in markets like Asia Pacific and Latin America where in-person therapy infrastructure is less developed.

|

"The evidence base for digital therapeutics in mental health has crossed the threshold that payers require. We are no longer debating whether DTx works — we are negotiating coverage terms and outcomes-based contracts." — Dr. Adam Chekroud, Co-Founder & President, Spring Health (Source: HIMSS Global Health Conference & Exhibition, March 2023) |

What Is Restraining the Mental Health Digital Therapeutics Market?

- Regulatory Fragmentation Across Jurisdictions:

Mental health DTx developers pursuing multi-market entry face structurally incompatible regulatory requirements. The FDA's De Novo pathway requires a distinct evidence package from Germany's DiGA three-stage assessment (fast-track, positive care effects confirmation, long-term benefits demonstration). Japan's PMDA DTx guidance, introduced in 2020, carries distinct clinical data format requirements. Australia's TGA has yet to establish a DTx-specific reimbursement pathway equivalent to DiGA. This fragmentation imposes sequential rather than parallel market-entry strategies, extending time-to-revenue and increasing the capital requirement for international commercialisation. Smaller DTx developers without dedicated regulatory affairs infrastructure face a practical ceiling on geographic expansion — a structural advantage for pharma-backed entrants with established multi-market regulatory teams. North America and Europe feel this tension most acutely, as DTx developers must choose between U.S.-first and EU-first commercialisation pathways with limited capital for both simultaneously.

- Evidence Requirements and the Randomised Controlled Trial Barrier:

The clinical evidence bar for payer reimbursement has risen substantially since early DTx authorisations. Observational studies and retrospective analyses — acceptable for initial market entry — are increasingly insufficient for formulary inclusion or preferred-vendor status with major U.S. health plans or European statutory insurers. Randomised controlled trials (RCTs) cost USD 2–10 Million per indication and require 18–36 months to design, execute, and analyse. For DTx companies operating on venture timelines, this creates a funding gap between product development and clinical validation. The challenge is most acute in the substance use disorder and psychosis segments, where placebo-controlled trial design presents ethical complications that extend trial timelines further. Regulatory agencies in multiple jurisdictions are working on adaptive trial guidance for DTx, but no harmonised standard exists as of 2025.

- Engagement Attrition and the Therapeutic Paradox:

Mental health conditions create a fundamental paradox for DTx adoption. Depression — the largest therapeutic area — is characterised by anhedonia, low motivation, and executive function impairment: the precise cognitive states that reduce sustained engagement with any digital platform. Industry data suggests 30–60% of mental health app users disengage within 30 days of download. This attrition undermines the clinical outcomes data that reimbursement negotiations require, creating a circular challenge — poor engagement produces poor outcomes data, which limits payer coverage, which limits clinician prescription, which limits patient access. DTx developers are responding with passive-monitoring architectures and notification-driven re-engagement systems, but the engagement problem remains the most cited barrier in payer negotiations and represents a genuine clinical quality risk, not simply a commercial challenge.

|

"The reimbursement conversation with insurers always comes back to the same question: show me the RCT. The companies that can answer that question with published data are in a completely different negotiation than those that can't." — Jenna Carl, Chief Medical Officer, Big Health (Source: American Psychiatric Association Annual Meeting, May 2023) |

What Opportunities Exist in the Mental Health Digital Therapeutics Market?

- Employer-Sponsored Mental Health DTx Programmes:

The employer wellness channel represents the fastest-growing institutional demand pathway for mental health DTx. U.S. employers lose an estimated USD 1,900 per employee annually to depression-related productivity loss, according to data from the American Institute of Stress. DTx platforms that can demonstrate measurable reduction in claims costs and absenteeism within a 12-month plan cycle command premium per-employee-per-month (PEPM) pricing that exceeds consumer app revenue by a factor of 10–20x. Spring Health, Ginger.io, and Lyra Health have each established employer-channel business models that now serve hundreds of employers and millions of covered lives. The untapped opportunity lies in mid-market employers (500–5,000 employees) who currently lack access to enterprise mental health platforms due to minimum participation requirements.

- Paediatric and Adolescent Mental Health DTx:

Adolescent mental health represents one of the most acute unmet needs in the DTx market. WHO data shows that 50% of all mental health conditions emerge before age 14, yet paediatric-specific clinical-grade DTx products remain scarce. The FDA cleared Swing Therapeutics' Rejoyn for MDD in adults in 2023 — paediatric labelling extensions represent an approved pathway with clear commercial logic. Limbix, a specialist adolescent mental health DTx developer, has focused exclusively on this segment. However, the opportunity remains largely uncaptured: most established DTx platforms lack age-specific evidence packages and paediatric UX designs. Developers who invest in paediatric clinical validation now face a 3–5 year first-mover window before the segment attracts large-scale pharmaceutical investment.

- Emerging Market DTx Penetration via Public Health System Partnerships:

India, Brazil, Indonesia, Nigeria, and South Africa collectively represent a combined population of over 2.5 billion people, with mental health treatment gaps exceeding 90% in most of these markets. Traditional in-person mental health infrastructure cannot be built at sufficient scale within any realistic policy horizon. Digital therapeutics — particularly low-bandwidth mobile-first platforms — offer a structurally viable pathway to population-scale mental health access. Partnerships with national health ministries, international development organisations (WHO, World Bank), and telecom operators represent the go-to-market model for emerging market penetration. Revenue realisation operates on a public-health procurement model rather than per-patient subscription — lower per-unit economics but vastly larger addressable volumes.

- Integration with Pharmacotherapy and Companion Diagnostic DTx:

The most compelling pipeline opportunity in mental health DTx lies in the integration of digital therapeutic protocols with psychiatric pharmacotherapy. DTx platforms that monitor patient response to antidepressants, antipsychotics, or addiction medications — and adaptively adjust behavioural therapy content based on pharmacological response data — create a companion diagnostic and therapeutic value that pharmaceutical companies cannot easily replicate internally. Otsuka's partnership with Click Therapeutics and Novartis' DTx investment programme are both premised on this companion-therapy model. The regulatory pathway for combination products (drug + DTx) is established through FDA's Combination Products Office, making the commercial and regulatory logic tractable. This category could command premium pricing that exceeds standalone DTx by 3–5x if clinical outcomes data supports the combination-therapy value claim.

What Challenges Does the Mental Health Digital Therapeutics Market Face?

- Data Privacy, HIPAA Compliance, and Cybersecurity Risk:

Mental health data is among the most sensitive personal health information categories, carrying reputational, legal, and actuarial risk for any entity that processes it. Mental health DTx platforms collect continuous behavioural, mood, and linguistic data — a profile that, if breached, creates patient harm risk beyond standard medical data breaches. U.S. HIPAA enforcement has been extended to digital health platforms; EU GDPR Article 9 imposes specific conditions on processing health data for research or commercial purposes. DTx developers operating in multiple jurisdictions face the compound challenge of jurisdiction-specific data residency requirements — some markets (China, Russia, Germany in certain contexts) require in-country data storage — increasing infrastructure cost and operational complexity for global platforms.

- Digital Divide and Equity of Access:

The populations with the highest mental health burden — lower-income communities, rural populations, elderly individuals — are precisely those with the lowest rates of smartphone ownership, digital literacy, and broadband access. A DTx market that serves exclusively the digitally connected and economically comfortable population misses the clinical need most acutely. Healthcare equity regulations in multiple jurisdictions are beginning to require equity impact assessments for digital health technologies receiving public reimbursement. DTx developers who do not proactively design for low-digital-literacy populations and low-bandwidth environments risk regulatory scrutiny and reputational challenge — and forfeit access to the public-sector procurement contracts that the emerging market opportunity requires.

- Competitive Pressure from Adjacent Consumer Wellness Platforms:

The mental health DTx market faces boundary-blurring competitive pressure from consumer wellness apps — Headspace, Calm, BetterHelp — that do not carry FDA clearance but market similar benefits at lower price points. While the clinical-grade DTx segment is differentiated by regulatory authorisation and reimbursement access, the consumer perception gap between a clinically validated DTx and a well-marketed wellness app remains narrow for many patients and some employers. DTx companies must invest in patient and employer education as a sales cost — explaining the clinical-grade distinction — while simultaneously defending their premium pricing against wellness platform alternatives that compete on brand recognition and consumer acquisition budgets.

Mental Health Digital Therapeutics Market: Report Scope

|

Attribute |

Detail |

|

Report Name |

Global Mental Health Digital Therapeutics Market Report 2026–2034 |

|

Market Size in 2025 |

USD 5,640 Million |

|

Market Forecast in 2034 |

USD 42,870 Million |

|

Growth Rate (CAGR) |

25.3% (2026–2034) |

|

Historical Data Period |

2019–2024 |

|

Base Year |

2025 |

|

Forecast Period |

2026–2034 |

|

Number of Pages |

300+ |

|

Tables & Figures |

Approx. 110+ tables, 80+ figures (complex market — 5 segmentation dimensions) |

|

Report Code |

ZMR-10559 |

|

Report Format |

|

|

Delivery Format |

Digital Download |

|

Published Date |

May 2026 |

|

Research Methodology |

Primary Research (interviews with DTx executives, hospital CIOs, payers, regulatory specialists) + Secondary Research (FDA/EMA/BfArM filings, peer-reviewed publications, company annual reports, earnings call transcripts) |

|

Key Companies Covered |

Pear Therapeutics, Mindstrong Health, Ginger.io, Headspace Health, Limbix, Click Therapeutics, Novartis AG, Otsuka Digital Health, Big Health, Freespira, Alto Neuroscience, Spring Health, Cerebral Inc., Noom, Woebot Health |

|

Segments Covered |

By Product Type; By Therapeutic Area; By Delivery Platform; By End User |

|

Regions Covered |

North America; Europe; Asia Pacific; Latin America; The Middle East; Africa (all 6 separate) |

|

Customization Scope |

Available — contact sales@zionmarketresearch.com for custom segment, country, or extended forecast requirements |

Mental Health Digital Therapeutics Market: Segmentation

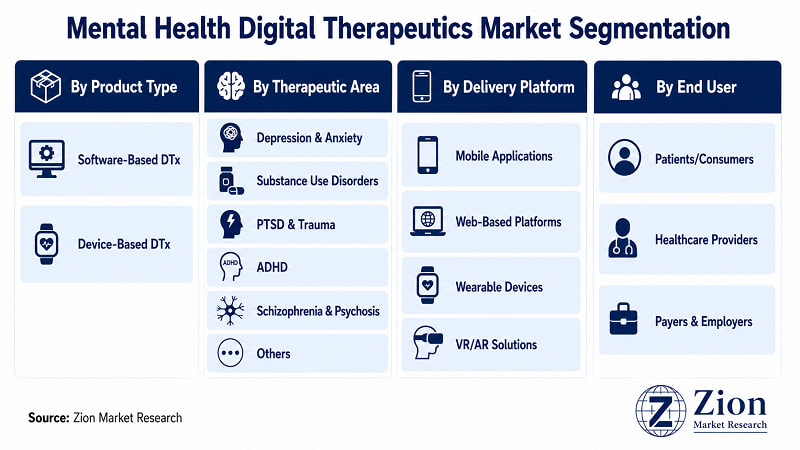

The Global Mental Health Digital Therapeutics market is segmented by Product Type, Therapeutic Area, Delivery Platform, and End User.

- By Product Type

The product type dimension divides the market into Software-Based DTx and Device-Based DTx. Software-Based DTx commands an estimated 68% share in 2025, driven by SaaS economics, app-store distribution, and regulatory pathway availability through the FDA's De Novo and 510(k) mechanisms. The category's dominant market position reflects lower capital intensity and faster iteration cycles compared to hardware. Device-Based DTx — wearables, neurostimulation devices, and biofeedback hardware — carries higher margins per unit and superior reimbursement in some payer categories, but faces manufacturing complexity and longer regulatory review timelines. Device-based solutions are growing faster in the PTSD and substance use disorder segments, where biometric monitoring adds clinical value unavailable to software-only platforms. Freespira's FDA-cleared device for PTSD and panic disorder exemplifies the device-DTx premium-reimbursement model.

- By Therapeutic Area

Depression & Anxiety represents the largest therapeutic area with ~38% market share, reflecting the highest diagnosed prevalence globally and the most mature clinical evidence base for DTx interventions. Cognitive behavioural therapy (CBT)-based software platforms have the strongest evidence base in this segment, with multiple RCTs validating digital CBT for both conditions. Substance Use Disorders is the fastest-growing therapeutic area, driven by the opioid crisis policy priority in North America and Australia and the regulatory momentum created by Pear Therapeutics' reSET authorisation. PTSD & Trauma, ADHD, and Schizophrenia & Psychosis represent emerging segments where clinical validation work is earlier-stage but regulatory pathway precedents are being established — particularly for PTSD, where the VA's interest in scalable DTx for veteran populations creates a significant public procurement opportunity.

- By Delivery Platform

Mobile Applications lead with an estimated 57% share — the natural distribution channel for consumer-facing and employer-facilitated DTx given smartphone penetration rates. Web-Based Platforms serve the enterprise and healthcare provider channel, where IT integration requirements and data security governance favour browser-based delivery over app-store-dependent mobile distribution. Wearable Devices represent a fast-growing segment as continuous biometric monitoring adds real-world clinical data capture to DTx programmes. Biometric data integration enables passive symptom monitoring — a capability that addresses the engagement-attrition challenge by reducing the active user burden. VR/AR Solutions remain the smallest platform segment but demonstrate the highest clinical efficacy in exposure therapy applications for PTSD and phobia treatment. Oxford VR and Limbix have both published clinical trial data on VR-delivered therapy outcomes, establishing the evidence base for this emerging delivery modality.

- By End User

Healthcare Providers are the fastest-growing end-user segment, as hospital systems, integrated delivery networks, and outpatient psychiatric practices formally integrate DTx into prescriber workflows. FDA-authorised PDT products require a healthcare provider prescriber — this institutional channel is distinct from direct-to-consumer access and carries superior average selling price. Patients/Consumers represent the largest current end-user segment by volume, served through app-store and employer-platform distribution. Payers & Employers are the structurally most important emerging end-user category — employers bear the productivity and insurance cost of employee mental health, creating a strong ROI case for DTx investment independent of clinical prescription pathways. Spring Health, Ginger.io, and Lyra Health have each built >USD 1 Billion valuation businesses exclusively on the employer channel, validating the commercial scale of this end-user segment.

Mental Health Digital Therapeutics Market: Regional Analysis

North America commands the largest share of the Global Mental Health Digital Therapeutics market in 2025, supported by the most mature regulatory framework for prescription DTx, the highest per-capita mental health expenditure, and a well-developed employer wellness infrastructure. Asia Pacific registers the fastest regional CAGR, driven by the intersection of high mental health burden, massive underserved populations, and accelerating digital health policy investment.

- North America Mental Health Digital Therapeutics Market

North America holds an estimated 42% of global market share in 2025. The U.S. leads by a wide margin — the FDA's prescriber-pathway DTx framework has created a commercially viable regulatory infrastructure unmatched globally. The National Institute of Mental Health (NIMH) estimates that nearly one in five U.S. adults lives with a mental health condition, creating a consumer demand base that sustains both employer-channel and direct-to-consumer DTx business models. Canada's provincial health systems are at varying stages of DTx integration; Ontario Health's digital health strategy includes exploratory frameworks for reimbursed digital mental health tools. Mexico's market is at an early stage, with DTx adoption concentrated among private health system patients. Key challenge for the region: Medicaid reimbursement for DTx remains inconsistent across U.S. states, limiting access for lower-income populations.

- Europe Mental Health Digital Therapeutics Market

Europe's DTx market is defined by Germany's DiGA framework — the world's most advanced statutory reimbursement mechanism for digital health applications. Germany's BfArM had reimbursed over 53 digital health apps by end-2023, with mental health applications forming the largest category. This creates a benchmark market where clinical evidence standards and commercial outcomes data are most mature. The U.K.'s NHS has deployed Big Health's Sleepio and Daylight at scale, demonstrating public health system DTx integration at population level. France and the Nordic countries (Sweden, Denmark) are developing national digital health strategies that include DTx reimbursement pathways. The EU MDR classification and GDPR data privacy requirements create unified compliance challenges for DTx developers seeking pan-European deployment.

- Asia Pacific Mental Health Digital Therapeutics Market

Asia Pacific registers the fastest regional growth, driven by structurally distinct market dynamics across its major economies. China's National Health Commission '14th Five-Year' mental health action plan (2021–2025) allocates specific investment to digital mental health infrastructure — creating policy-level demand for DTx-equivalent platforms. India's treatment gap (fewer than 9,000 psychiatrists for 1.4 billion people) makes DTx the only structurally scalable mental health delivery pathway. Japan's PMDA issued DTx-specific guidance in 2020 and has since approved software-based interventions for hypertension and nicotine dependence — a regulatory pathway directly applicable to mental health DTx. South Korea's digital health regulatory environment has advanced significantly since 2021, with the Korea Health Industry Development Institute (KHIDI) supporting DTx clinical evidence programmes. Australia's Therapeutic Goods Administration (TGA) is developing formal digital health product regulation, with mental health platforms operating under existing SaMD (Software as Medical Device) classifications pending dedicated DTx guidance.

- Latin America Mental Health Digital Therapeutics Market

Latin America represents a market at early commercial stage but with substantial structural demand. Brazil leads regional adoption, driven by ANVISA's progressive digital health regulatory updates and the country's large private health insurance sector (approximately 50 million beneficiaries) that provides a viable institutional payer channel for DTx. Brazil's SUS (Unified Health System) mental health programme — the second largest public mental health programme globally by coverage — represents a long-term public procurement opportunity for scalable DTx platforms. Colombia and Argentina have developing digital health regulatory frameworks but lag Brazil by 3–5 years in DTx-specific provisions. Key regional challenge: currency volatility and USD-denominated DTx pricing create affordability barriers for private-pay consumer adoption in Argentina and Venezuela. DTx developers targeting Latin America are primarily pursuing employer-channel and private payer routes, with public health system integration as a medium-term objective.

- The Middle East Mental Health Digital Therapeutics Market

The Middle East DTx market is characterised by strong government-driven healthcare digitisation initiatives, particularly in the GCC. Saudi Arabia's Vision 2030 health transformation programme has elevated digital health as a national priority, with the Saudi Health Council actively supporting digital therapeutics evaluation frameworks. The UAE's Dubai Health Authority has implemented digital health innovation policies that provide a favourable regulatory environment for DTx pilot programmes. Israel represents the region's most advanced DTx ecosystem — Israel's digital health sector benefits from a combination of strong health data infrastructure (through Clalit Health Services' integrated EHR system), a globally competitive health tech startup ecosystem, and significant government investment in digital health R&D. The mental health stigma challenge remains a notable restraint across much of the Middle East, suppressing patient self-identification and limiting consumer-channel DTx adoption despite favourable infrastructure.

- Africa Mental Health Digital Therapeutics Market

Africa represents the most nascent but structurally significant long-term opportunity in the Global Mental Health Digital Therapeutics market. The continent carries an estimated 20% of the global mental health burden with less than 2% of global mental health resources, according to WHO data. South Africa leads the regional market, with a developed private health insurance sector and a progressive digital health regulatory framework under the South African Health Products Regulatory Authority (SAHPRA). Egypt's National Mental Health Programme has incorporated digital health tools in pilot initiatives, supported by WHO Eastern Mediterranean Region technical assistance. Nigeria's mental health burden is enormous — an estimated 40–50 million Nigerians live with mental health conditions — but the formal healthcare infrastructure to support prescription DTx remains limited. The viable near-term model for Africa is mobile-first, low-bandwidth DTx deployed through public health partnerships, NGO networks, and telecom operator distribution — not the prescription-pathway model dominant in North America.

Full Country Coverage

|

Region |

Countries Covered |

|

North America |

The U.S., Canada, Mexico |

|

Europe |

Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe |

|

Asia Pacific |

China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific |

|

Latin America |

Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America |

|

The Middle East |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

Africa |

South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa |

**Country-level market sizing, historical data, and forecasts available for all geographies listed. Custom regional add-ons available — contact sales@zionmarketresearch.com

Mental Health Digital Therapeutics Market: Competitive Landscape

- The Global Mental Health Digital Therapeutics market is moderately fragmented, with a clear bifurcation between clinical-grade prescription DTx developers pursuing FDA and European regulatory authorisation, and consumer-facing employer-channel platforms scaling through B2B wellness partnerships. The competitive differentiation axis is shifting from technology features toward clinical evidence depth and payer reimbursement coverage — capabilities that favour well-capitalised incumbents and pharma-backed entrants over early-stage startups.

- Key players operating in the Global Mental Health Digital Therapeutics market include Pear Therapeutics (U.S.), Mindstrong Health (U.S.), Ginger.io (U.S.), Headspace Health (U.S.), Limbix (U.S.), Click Therapeutics (U.S.), Novartis AG (Switzerland), Otsuka Digital Health (Japan), Big Health (U.K.), Freespira (U.S.), Alto Neuroscience (U.S.), Spring Health (U.S.), Cerebral Inc. (U.S.), Noom (U.S.), and Woebot Health (U.S.), among others.

|

Company |

HQ Country |

Primary Focus |

Key Strategy |

Notable Recent Action |

|

Pear Therapeutics |

U.S. |

Prescription DTx (SUD) |

FDA-authorised PDT pipeline |

Secured PDT codes for reSET & reSET-O; Chapter 11 filing 2023; assets acquired |

|

Click Therapeutics |

U.S. |

Prescription DTx (MDD, Schizophrenia) |

Pharma co-development partnerships |

Otsuka partnership for MDD DTx; AstraZeneca partnership for Alzheimer's cognition |

|

Big Health |

U.K./U.S. |

CBT-based DTx (insomnia, anxiety) |

Employer & payer channel + NHS partnership |

NHS-scaled Sleepio deployment; Daylight for anxiety launched in U.S. employer market |

|

Headspace Health |

U.S. |

Employer wellness DTx |

B2B enterprise SaaS + clinical DTx merger |

Merger with Ginger.io 2022 to combine wellness & clinical DTx platforms |

|

Spring Health |

U.S. |

Employer mental health benefits |

Precision mental health routing algorithm |

USD 100M Series D (2023); 200+ employer clients including General Mills |

|

Freespira |

U.S. |

Device-based DTx (PTSD, panic disorder) |

VA and hospital system deployment |

Expanded VA contract coverage; FDA clearance for panic disorder indication |

|

Otsuka Digital Health |

Japan |

PDT companion to psychiatric drugs |

Integration with Abilify MyCite digital medicine system |

Click Therapeutics MDD co-development agreement 2021 |

|

Novartis AG |

Switzerland |

DTx investment & co-development |

Strategic investment in DTx pipeline companies |

Multiple DTx partnership agreements in neuropsychiatry therapeutic area |

|

Woebot Health |

U.S. |

NLP-driven conversational DTx |

Consumer + healthcare provider integration |

100M+ chatbot interactions by 2023; partnership with UCSF for clinical validation |

|

Limbix |

U.S. |

Adolescent mental health DTx |

Paediatric-focused DTx pipeline |

Published clinical trial data for adolescent depression DTx; FDA submission in progress |

- M&A activity is accelerating across the competitive landscape. Pharmaceutical incumbents are acquiring or co-developing DTx assets to build companion therapy value propositions that enhance their existing psychiatric drug pipelines. The Chapter 11 filing and asset acquisition of Pear Therapeutics in 2023 signals that standalone prescription DTx without a pharmaceutical partner faces a difficult capital market environment at current evidence-generation costs.

Recent Developments in the Mental Health Digital Therapeutics Market

Strategic activity in the Mental Health Digital Therapeutics market is accelerating across all categories — M&A, product launches, regulatory approvals, and investment rounds. The pace of capital deployment signals sustained institutional confidence in the market's commercial fundamentals despite high-profile setbacks in the pure-play prescription DTx segment.

|

Date |

Company |

Type |

Description |

Market Impact |

|

Mar 2024 |

Click Therapeutics / Otsuka |

Partnership Expansion |

Expanded co-development agreement for MDD prescription DTx following positive Phase 2 digital biomarker data. |

Validates pharma-backed DTx co-development model; accelerates PDT pipeline timelines. |

|

Nov 2023 |

BfArM (Germany) |

Regulatory Approval |

Approved Velibra (anxiety DTx) for DiGA statutory reimbursement — first anxiety-specific DTx reimbursement in the EU. |

Expands EU DTx reimbursement precedent; signals payer acceptance for anxiety-specific DTx. |

|

Aug 2023 |

Spring Health |

Investment |

Secured USD 100 Million Series D, valuation reaching USD 2 Billion, backed by Tiger Global and existing investors. |

Confirms investor appetite for employer-channel mental health DTx at scale. |

|

Mar 2023 |

Rejoyn (Alto Neuroscience) |

FDA Authorisation |

FDA De Novo authorisation for Rejoyn — the first prescription DTx for MDD as an adjunctive treatment to antidepressants. |

First MDD prescription DTx clearance; opens largest therapeutic area to reimbursement pathway. |

|

Jul 2022 |

Headspace / Ginger.io |

Merger |

Merger of Headspace and Ginger.io creating Headspace Health — combining wellness app scale with clinical DTx capabilities. |

Creates first scaled platform combining consumer wellness and clinical DTx in one entity. |

|

Jan 2022 |

NHS England / Big Health |

Partnership |

NHS England renewed and expanded national deployment of Sleepio (insomnia) and Daylight (anxiety), covering population access. |

Largest public health system DTx deployment globally; establishes NHS as DTx adoption benchmark. |

About Zion Market Research

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is updated constantly in order to fulfil our clients' requirements for prompt and direct online access. Keeping in mind the client's needs, we have included expert insights on global industries, products, and market trends in this database.

Author:

Mr. Nilesh Patil

Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067

Table Of Content

Methodology

FrequentlyAsked Questions

The ZMR Global Mental Health Digital Therapeutics Market Report 2026–2034 is a 300+ page comprehensive study covering market sizing and forecast (2019–2034), four segmentation dimensions (Product Type, Therapeutic Area, Delivery Platform, End User), full DROC analysis (Drivers, Restraints, Opportunities, Challenges), regional analysis across 6 ZMR regions with 35+ country-level forecasts, competitive landscape analysis with strategy table, 15 company profiles, and research methodology documentation. Tables and figures: approximately 110+ tables and 80+ figures.

According to Zion Market Research, the Global Mental Health Digital Therapeutics market was valued at USD 5,640 Million in 2025 and is projected to reach USD 42,870 Million by 2034. The market grows at a 25.3% CAGR over the forecast period 2026–2034, supported by rising mental health burden, expanding regulatory reimbursement frameworks, and AI-powered personalisation of therapy delivery platforms.

This report segments the Global Mental Health Digital Therapeutics market across four dimensions: (1) By Product Type — Software-Based DTx and Device-Based DTx; (2) By Therapeutic Area — Depression & Anxiety, Substance Use Disorders, PTSD & Trauma, ADHD, Schizophrenia & Psychosis, and Others; (3) By Delivery Platform — Mobile Applications, Web-Based Platforms, Wearable Devices, and VR/AR Solutions; (4) By End User — Patients/Consumers, Healthcare Providers, and Payers & Employers.

The report provides country-level market sizing and forecasts across 6 ZMR regions — The Middle East and Africa are covered as entirely separate regional analyses, never combined. North America: The U.S., Canada, Mexico. Europe: Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe. Asia Pacific: China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific. Latin America: Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America. The Middle East: GCC, Israel, Turkey, Iran, Rest of Middle East. Africa: South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa.

Zion Market Research offers customization across multiple dimensions: additional geographic markets not in the standard scope; company-specific competitive benchmarking; extended forecast periods beyond 2034; additional segmentation dimensions (e.g., by reimbursement type, by therapeutic protocol, by regulatory jurisdiction); custom primary research interviews with sector-specific stakeholders; and proprietary executive briefings. Contact sales@zionmarketresearch.com or call +1 (302) 444-0166 to discuss requirements.

List of Contents

Mental Health Digital Therapeutics Industry PerspectiveMental Health Digital Therapeutics OverviewKey InsightsWhy Choose the Zion Market ResearchsMarket Report?Mental Health Digital Therapeutics Dynamics (Drivers, Restraints, Opportunities, Challenges)Mental Health Digital Therapeutics Report ScopeMental Health Digital Therapeutics SegmentationMental Health Digital Therapeutics Regional AnalysisFull Country CoverageMental Health Digital Therapeutics Competitive LandscapeRecent Developments in theMarketHappyClients