Hospital Information System Market Size, Share, Trends & Forecast 2026–2034

Global Hospital Information System Market Size, Share, Growth, Trends Analysis, By Component (Software, Hardware, IT Infrastructure & Networking Services, Professional Services), By Deployment Model (On-Premise, Cloud-Based, Hybrid), By Application (EHR, Hospital Management, Revenue Cycle Management, Patient Portal, Clinical Decision Support, Pharmacy Management), By End User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Long-term Care Facilities, Pharmacies), By Region, and Forecast — 2026 to 2034.-

| Market Size in 2025 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 16,340 Million | USD 48,720 Million | 12.9% | 2025 |

Hospital Information System Industry Perspective:

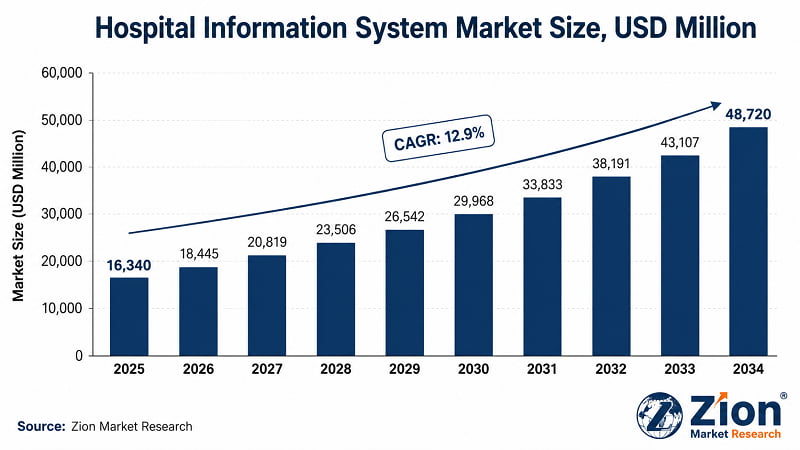

- At USD 16,340 Mn in 2025, the global hospital information system market reflects more than a decade of policy-driven digitalisation across healthcare delivery systems. The 12.9% CAGR projected through 2034 — reaching USD 48,720 Mn — signals a market that has moved beyond early adoption into full institutionalisation. The analytical question is no longer whether HIS will be adopted, but which deployment architectures, application layers, and regional vectors will generate disproportionate return.

- Three structural forces are shaping the trajectory. First, regulatory frameworks on four continents now mandate electronic health record implementation — converting what was optional IT investment into non-discretionary infrastructure spend. Second, the AI capability layer maturing within EHR and clinical decision support modules is compressing vendor competitive half-lives, rewarding early movers in AI-native architectures. Third, the outpatient and ambulatory care shift — accelerated by post-pandemic care delivery restructuring — is expanding the addressable market to settings that traditionally operated outside enterprise HIS scope.

- For procurement directors and capital allocators, the Zion Market Research's Hospital Information System Market report delivers sub-segment level sizing, country-level forecasts, and competitive positioning analysis across 5 segmentation dimensions and 35+ geographies — the analytical foundation for informed go-or-no-go decisions.

Hospital Information System Market: Overview

- Hospital information system encompasses the integrated set of software platforms, hardware infrastructure, networking services, and professional consulting solutions deployed across healthcare facilities to manage clinical workflows, administrative processes, financial operations, and patient care coordination. The market spans foundational infrastructure providers through to specialised application vendors serving specific care settings and clinical functions.

- The HIS value chain operates across three functional tiers. Foundational providers — including Microsoft (Azure Health Data Services), Amazon Web Services (AWS HealthLake), and Google Cloud (Healthcare API) — supply the infrastructure and data platform layer underpinning HIS deployments. Specialist integrators and core platform developers — Epic Systems, Oracle Health, and Allscripts — deliver the EHR, clinical, and revenue management applications that form the enterprise core. Application-layer specialists — including Veeva Systems (clinical trials), Netsmart Technologies (behavioural health), and Athenahealth (ambulatory care) — address vertical and specialty market segments with purpose-built solutions.

- For procurement and investment decision-makers, the distinction that matters is not whether hospital information system will grow — that question is settled — but which segments, geographies, and deployment models will capture disproportionate value within that growth. This report provides sub-segment level data, country-level forecasts, and competitive positioning analysis across 5 segmentation dimensions and 35+ geographies.

Key Insights

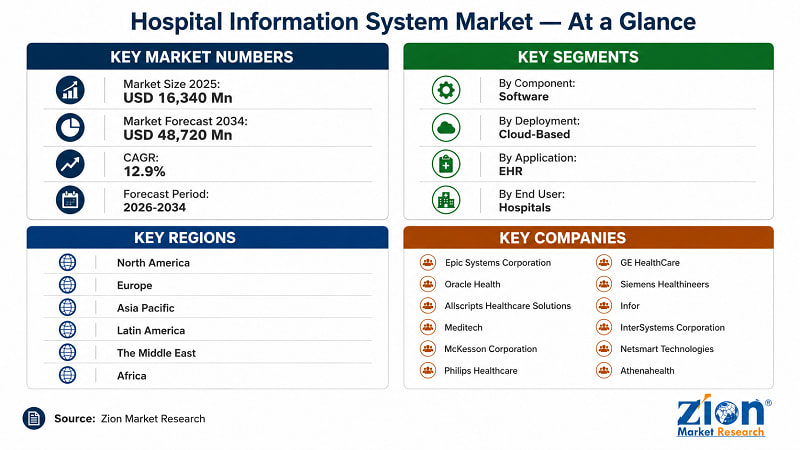

- The Global Hospital Information System market will grow from USD 16,340 Mn (2025) to USD 48,720 Mn (2034), registering a 12.9% CAGR over 2026–2034, per Zion Market Research.

- Software is the dominant component segment, holding approximately 58% of market revenue in 2025, driven by cloud-native EHR, clinical, and revenue cycle platforms generating recurring SaaS contract revenue.

- Cloud-Based deployment is the fastest-growing model, expanding at a CAGR exceeding the market average, as health systems prioritise scalability, remote access, and reduced capital expenditure over legacy on-premise architectures.

- Electronic Health Records (EHR) is the dominant application segment (~38% share), sustained by regulatory mandates on four continents requiring EHR implementation as a condition of reimbursement or licensure.

- Clinical Decision Support is the fastest-growing application segment, as AI model integration into prescribing, diagnostics, and care pathway management generates measurable care quality and operational efficiency outcomes.

- Hospitals represent the dominant end-user segment (~61% of 2025 revenue), given their enterprise-scale deployment requirements and budget authority for multi-year HIS contracts.

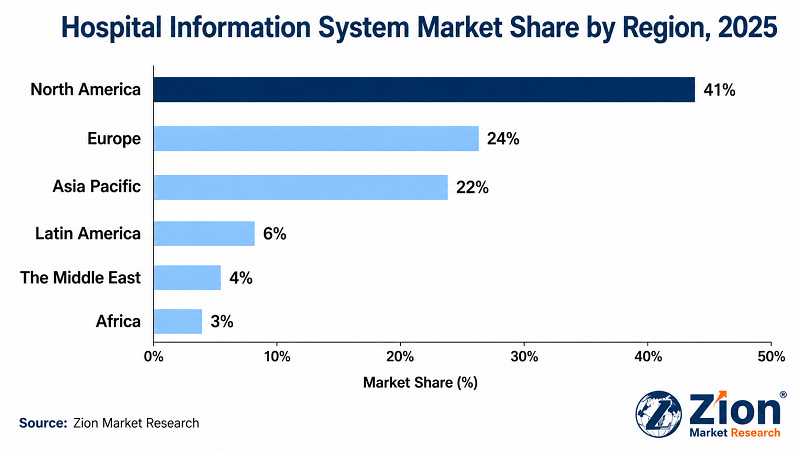

- North America leads regional market share (~41% in 2025), anchored by U.S. regulatory mandates, deep Epic and Oracle Health penetration, and federal interoperability investment through ONC.

- Asia Pacific is the fastest-growing region, propelled by India's Ayushman Bharat Digital Mission, China's national HIE expansion, and Australia's My Health Record integration mandates.

- The competitive landscape is consolidating around a small number of cloud-native full-suite platform vendors — Epic, Oracle Health — while a second tier of specialty and regional players differentiates on application depth and geographic coverage.

Why Choose the Zion Market Research's Hospital Information System Market Report?

Decision-makers comparing market intelligence reports on Hospital Information System will find the Zion Market Research's report differentiated on the following dimensions.

|

Dimension |

Zion Market Research Report |

Industry Average |

|

Report Pages |

300+ |

~120 pages |

|

Forecast Horizon |

9 years (2026–2034) |

7 years |

|

Segmentation Dimensions |

5 dimensions |

4–5 dimensions |

|

Historical Data |

6 years (2019–2024) |

4–5 years |

|

Country Coverage |

35+ countries |

15–18 countries |

|

Companies Profiled |

12-15 companies |

10 companies |

|

DROC Framework |

Full (Drivers, Restraints, Opportunities, Challenges) |

Drivers only |

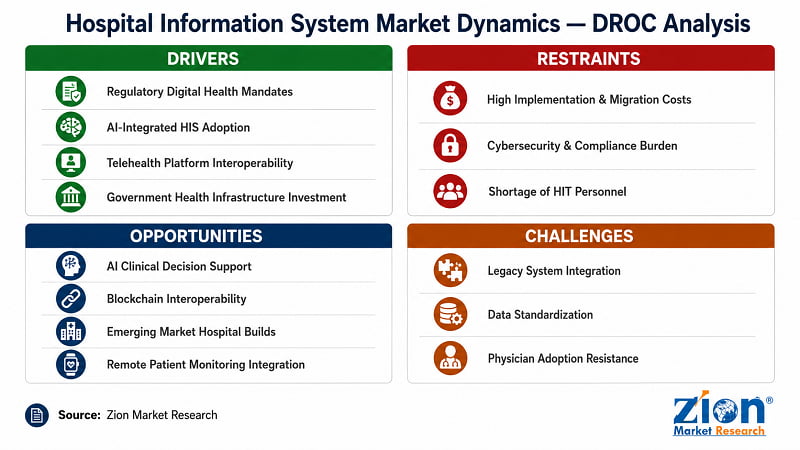

Hospital Information System Market: Dynamics (Drivers, Restraints, Opportunities, Challenges)

What Is Driving the Hospital Information System Market?

- Regulatory Mandates for Digital Health Records (Strongest Driver):

Health information technology legislation has created a structural demand floor that cannot be unwound. The U.S. HITECH Act allocated over USD 35 Bn in incentive payments to drive EHR adoption — a policy that succeeded in raising hospital EHR adoption from under 10% in 2008 to above 96% by 2021, per ONC data. The European Union's EU4Health programme and incoming European Health Data Space (EHDS) regulation extend this regulatory architecture across 27 member states, mandating cross-border health data interoperability by 2025.

India's Ayushman Bharat Digital Mission (ABDM), operationalised across all states from 2022, is creating the largest new addressable market in the sector. With 600 Mn digital health IDs issued and growing, ABDM is incentivising hospital HIS adoption at a scale no commercial marketing campaign could replicate. In the GCC, Saudi Arabia's Vision 2030 health IT pillar is directing multi-billion dollar investments into national HIS infrastructure, with Ministry of Health contracts serving as anchor demand for regional procurement.

The mechanism is direct: compliance is not optional. Health systems that fail to meet regulatory HIS requirements face exclusion from reimbursement schemes, loss of accreditation, and in some jurisdictions, operating licence risk. This converts HIS procurement from a capital budgeting decision into a compliance obligation — a qualitatively different demand driver with far greater downside resistance.

- AI Integration into Clinical Decision Support and Hospital Operations (Accelerating Driver):

The capability gap between AI-integrated and legacy HIS platforms is widening rapidly. Oracle Health deployed its AI-powered Clinical Documentation Improvement module across its EHR installed base from 2023, targeting physician documentation burden reduction — a pain point that contributes to clinician burnout and reduces time available for direct care. Early deployment data from pilot health system partners indicated documentation time reductions of 30–45 minutes per physician per day, per Oracle's public communications.

Beyond documentation, AI applications in sepsis prediction, deterioration alerting, and medication safety are generating measurable patient outcome improvements that health systems can present to payers and regulators. This outcome evidence creates a competitive differentiation cycle: health systems adopting AI-integrated HIS demonstrate quality metrics that support value-based contracting at premium rates, incentivising faster AI adoption cycles.

From a supply-side perspective, every major HIS vendor has committed AI capability roadmaps. The market implication is significant: vendors without credible AI integration face capability obsolescence within 3–5 years. For buyers, this creates procurement urgency — contract cycles that started as 7–10 year EHR agreements are now structured with 3-year AI capability review clauses.

- Telehealth Expansion Requiring Interoperable HIS Architectures (Sustained Driver):

Telehealth utilisation rates have not returned to pre-2020 levels. McKinsey estimated global telehealth volume stabilising at 38 times its pre-pandemic baseline, a demand level that requires HIS platforms capable of capturing, integrating, and acting on data generated across remote and in-person care settings simultaneously. The operational consequence is acute: a health system running telehealth visits on a platform that doesn't write back to its core EHR is accumulating clinical record fragmentation that degrades care coordination and increases liability exposure.

Cloud-based and hybrid HIS architectures are capturing this demand. The ability to extend EHR access to remote clinicians, integrate remote patient monitoring device data, and maintain single-patient record integrity across settings is architecturally impossible in pure on-premise configurations. Ochsner Health's digital medicine programme — which uses remote patient monitoring and HIS integration for chronic disease management — reported a 50% improvement in hypertension control rates in a publicly presented outcomes study, demonstrating the clinical case for integrated telehealth-HIS architectures.

- Government Investment in National Health IT Infrastructure (Regional Driver):

Beyond compliance mandates, direct government procurement and subsidy programmes are creating demand that would not exist at commercial pricing. Saudi Arabia's Ministry of Health has publicly committed to deploying an integrated national HIS infrastructure across all public hospitals by 2030 under Vision 2030. South Korea's government has funded national interoperability platform development. Australia's Digital Health Agency continues to invest in My Health Record infrastructure. These state-backed programmes create anchor contracts for international HIS vendors while building the installed base that drives services and upgrade revenue over decade-long cycles.

|

"The 21st Century Cures Act's information blocking provisions changed the game. For the first time, health systems face legal liability for not sharing data. The practical effect is that every HIS procurement decision now has to include a serious API and interoperability capability assessment — not just features and price." — Dr. Micky Tripathi, National Coordinator for Health IT, Office of the National Coordinator (ONC), U.S. Department of Health and Human Services (Source: HIMSS 2023 Annual Conference, March 2023) |

What Is Restraining the Hospital Information System Market?

- High Implementation Cost and Operational Disruption During Migration:

Enterprise HIS implementation is among the most resource-intensive technology projects undertaken by healthcare organisations. Full EHR replacement at a large multi-site health system — the level of investment required for systems like Epic or Oracle Health at academic medical centres — routinely involves total cost of ownership in the range of USD 100–500 Mn when hardware infrastructure, third-party integration, staff retraining, productivity loss during go-live, and post-implementation optimisation support are included.

This cost structure creates two distinct market problems. For large health systems, it creates switching cost lock-in that protects incumbents but suppresses competitive procurement activity — the primary benefit goes to Epic and Oracle Health. For smaller community hospitals and safety-net providers in both developed and emerging markets, the absolute cost of modern HIS implementation exceeds available capital, creating a two-tier market where resource-rich systems adopt rapidly while resource-constrained providers fall further behind.

The regional dimension is most acute in Latin America, Africa, and South and Southeast Asia, where public health system budget constraints are severe. Even government-funded HIS programmes in these regions face implementation stalls when domestic professional services capacity is insufficient.

- Cybersecurity Vulnerabilities and Multi-Jurisdictional Compliance Burden:

Healthcare is the most persistently targeted sector for ransomware and data breach attacks globally. IBM Security's 2023 Cost of a Data Breach Report found healthcare to have the highest average breach cost of any industry — USD 10.9 Mn per incident — for the 13th consecutive year. The connectivity that makes modern HIS valuable — integration with medical devices, remote monitoring, telehealth, and third-party analytics — also multiplies the attack surface.

Regulatory compliance adds a parallel cost layer. U.S. health systems must maintain HIPAA compliance with audit trail, access control, and breach notification obligations. European health systems operating under GDPR face data residency and processing restrictions that complicate cloud HIS adoption. Organisations operating in multiple jurisdictions — multinational hospital groups, global pharma companies with clinical systems — must maintain compliance across conflicting regulatory frameworks. This is not a one-time cost: it is a recurring annual budget commitment that grows as both the regulatory environment and the threat landscape evolve.

- Shortage of Trained Healthcare IT Personnel in Emerging Markets:

HIS deployment quality is inseparable from implementation and ongoing management capability. A well-designed system deployed poorly generates clinical resistance, workaround adoption, and data quality degradation that erodes the original value proposition. Across sub-Saharan Africa, South Asia, and parts of Southeast Asia, the pipeline of trained healthcare IT professionals — certified EHR implementation specialists, clinical informatics analysts, health data governance officers — is structurally insufficient relative to planned HIS deployment scale.

Government-funded programmes in these regions are beginning to address this through international partnership arrangements and domestic training investment, but workforce development lags infrastructure procurement by 3–5 years in most programmes. This constraint is unlikely to resolve fully within the forecast period, though it will moderate.

|

"The technology is no longer the hard part. What keeps me up at night is change management — getting clinicians to trust the system, use it correctly, and not build workarounds that corrupt the data. A failed EHR implementation is worse than no EHR at all." — Dr. Warner Thomas, President and Chief Executive Officer, Ochsner Health (Source: Becker's Hospital Review Annual Meeting remarks, 2023) |

What Opportunities Exist in the Hospital Information System Market?

- AI-Powered Clinical Decision Support Integration:

The convergence of large language models, real-world data assets, and EHR platform APIs is creating a generation of CDS tools with materially superior clinical utility to previous rule-based systems. Vendors positioning CDS as a native EHR module — rather than an adjunct product — are building a defensible competitive differentiation that justifies premium contract pricing. The opportunity is substantial: Zion Market Research estimates CDS to be the fastest-growing HIS application sub-segment through 2034, with healthcare system willingness-to-pay increasing as outcome evidence accumulates.

- Blockchain-Enabled Health Data Interoperability:

The persistent failure of traditional HL7 and proprietary interfaces to achieve true longitudinal patient record interoperability has created sustained demand for alternative architectures. Blockchain-based health data networks — piloted by organisations including MedRec and the Gem Health Network — offer cryptographically secure, patient-controlled data sharing across institutional boundaries without requiring central data repository trust. While commercial deployment remains early-stage, the regulatory tailwind from EHDS and ONC FHIR requirements is accelerating interoperability investment that positions blockchain-capable HIS vendors favourably for the next procurement cycle.

- Emerging Market Greenfield Hospital Builds in Africa and Southeast Asia:

Unlike North American and European markets where HIS adoption is primarily driven by replacement and upgrade cycles, sub-Saharan Africa and Southeast Asia contain substantial greenfield demand — new hospital construction programmes that require HIS from commissioning rather than legacy system replacement. These deployments are cloud-native by default, structurally advantaging vendors with modern SaaS architectures over legacy on-premise incumbents. The Zion Market Research's Africa and Asia Pacific regional forecasts identify this greenfield opportunity as the primary driver of above-average growth in these geographies through 2034.

- Remote Patient Monitoring Integration with Hospital HIS:

The clinical and commercial case for RPM integration is well-established — patients managed through RPM-integrated chronic disease programmes show measurably better outcomes at lower total cost. The HIS integration opportunity is the data layer: RPM devices generate continuous streams of vital signs, glucose readings, cardiac rhythms, and activity data that are clinically actionable only when contextualised within the patient's full longitudinal record in the HIS. Vendors building RPM-to-EHR integration as a core product capability — rather than a custom professional services engagement — are positioned to capture this demand as RPM adoption accelerates globally.

What Challenges Does the Hospital Information System Market Face?

- Legacy System Integration Complexity:

The HIS market carries a substantial legacy technology debt. Hospitals and health systems globally still operate on systems built in the 1990s and early 2000s — HL7 v2 interfaces, on-premise relational databases, non-API-accessible clinical applications. Modern cloud-native HIS deployment in these environments requires complex integration middleware, custom interface development, and data migration projects that can extend implementation timelines by 12–24 months and materially inflate costs. The challenge is not technical unsolvability — it is that the integration work is high-cost, high-risk, and health-system-specific, making it difficult to productise and scale.

- Data Standardization Across Heterogeneous Health Systems:

The promise of health data portability — the ability for a patient's record to follow them across health systems, payers, and geographies — depends on common data standards that remain inconsistently implemented. HL7 FHIR has achieved broad regulatory endorsement but uneven vendor implementation. SNOMED CT, LOINC, and ICD-11 are incompletely mapped across legacy systems. The practical consequence is that data migrated between HIS platforms frequently requires manual clinical review and remediation, adding costs that undermine the business case for system modernisation. This challenge is structural and will persist across the forecast period despite ongoing standards body work.

- Physician Adoption Resistance and Clinical Change Management:

The most technically capable HIS implementation fails if clinical end users don't use it correctly. Physician resistance to EHR adoption — driven by documentation burden, workflow disruption, and perceived reduction in patient interaction time — is a persistent industry challenge. Studies in the Journal of the American Medical Informatics Association have consistently found that EHR documentation adds 1–2 hours to a physician's daily workload. Vendors addressing this through AI-assisted documentation, ambient listening, and mobile-optimised interfaces are directly targeting the adoption friction — but the change management investment required at deployment remains a significant barrier, particularly in health systems with limited HIT programme management capacity.

Hospital Information System Market: Report Scope

|

Attribute |

Details |

|

Report Name |

Global Hospital Information System Market Size, Share, Growth, Trends Analysis, By Component, By Deployment Model, By Application, By End User, By Region, and Forecast — 2026 to 2034 |

|

Market Size in 2025 |

USD 16,340 Mn |

|

Market Forecast in 2034 |

USD 48,720 Mn |

|

Growth Rate (CAGR) |

12.9% |

|

Historical Data Period |

2019–2024 |

|

Base Year |

2025 |

|

Forecast Period |

2026–2034 |

|

Number of Pages |

300+ |

|

Tables & Figures |

120 Tables, 85 Figures |

|

Report Code |

ZMR-10557 |

|

Report Format |

|

|

Delivery Format |

Instant Download | Email Delivery |

|

Published Date |

May 2026 |

|

Research Methodology |

Primary Research (Expert Interviews, Surveys) + Secondary Research (Company Reports, Regulatory Filings, Trade Publications) |

|

Key Companies Covered |

Epic Systems Corporation, Oracle Health, Allscripts Healthcare Solutions, Meditech, McKesson Corporation, Philips Healthcare, GE HealthCare, Siemens Healthineers, Infor, InterSystems Corporation, Netsmart Technologies, Athenahealth |

|

Segments Covered |

By Component, By Deployment Model, By Application, By End User |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, The Middle East, Africa |

|

Customization Scope |

Available — contact sales@zionmarketresearch.com for custom scope, geographies, and segments |

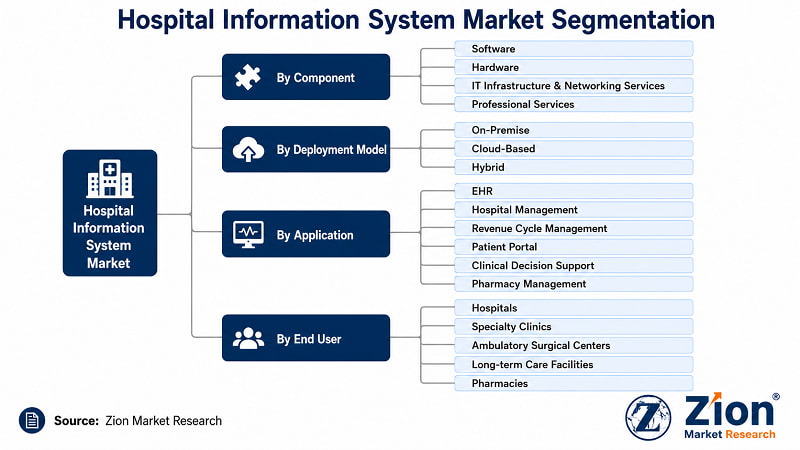

Hospital Information System Market: Segmentation

The Global Hospital Information System market is segmented by component, deployment model, application, and end user.

- By Component

Software holds approximately 58% of total HIS market revenue in 2025, driven by the recurring SaaS contract model that generates predictable annual recurring revenue for vendors and aligns payment timing with system utilisation for buyers. Cloud-native EHR and clinical management platforms — led by Epic Systems and Oracle Health — dominate this sub-segment. Hardware's share has contracted as compute shifts to cloud infrastructure. IT Infrastructure & Networking Services commands a stable share as network security and edge computing requirements at point-of-care settings maintain persistent demand. Professional Services is the fastest-growing component sub-segment — not because vendors are growing services margin, but because implementation complexity is rising as health systems simultaneously modernise core EHR, integrate AI modules, and address cybersecurity requirements in multi-year transformation programmes.

- By Deployment Model

Cloud-Based deployment captured over 52% of new HIS deployments in 2025, making it the first year in which cloud-based contracts outnumbered on-premise deployments. The driver is not merely cost — it is operational resilience, with cloud architectures offering disaster recovery and business continuity capabilities that on-premise systems cannot match without matching capital investment. Hybrid deployment is the second-fastest-growing model, as large health systems with substantial legacy on-premise infrastructure phase migration rather than executing big-bang replacements. On-Premise retains a meaningful share among very large academic medical centres and government health systems with data sovereignty requirements that preclude public cloud hosting.

- By Application

Electronic Health Records (EHR) commands approximately 38% of application revenue — the largest single application segment. Regulatory mandates are the primary sustaining factor; meaningful EHR share erosion would require policy reversal that is not anticipated in any major market. Hospital Management software is the second-largest segment, covering bed management, scheduling, supply chain, and facilities management workflow. Revenue Cycle Management is growing as health systems prioritise claim denial reduction and revenue integrity — payer complexity and denial rates have increased in the U.S. post-pandemic, creating acute demand for RCM analytics. Clinical Decision Support is the fastest-growing application, expanding at a CAGR that outpaces the market average as AI model deployment within EHR workflows accelerates.

- By End User

Hospitals represent 61% of market revenue in 2025 — the dominant end-user segment by a significant margin. Enterprise-scale HIS deployments at 100+ bed inpatient facilities represent the highest-value contracts in the market. Specialty Clinics are the second-largest segment, with cardiology, oncology, and orthopaedic groups deploying specialised EHR modules. Ambulatory Surgical Centers (ASCs) are the fastest-growing end-user segment as the outpatient surgical shift accelerates — Surgery Partners and Surgical Care Affiliates have both publicly indicated ongoing HIS modernisation investments. Long-term Care Facilities and Pharmacies represent smaller but stable end-user segments with distinct workflow and compliance requirements driving specialised HIS solution demand.

Hospital Information System Market: Regional Analysis

North America leads the global hospital information system market with approximately 41% revenue share in 2025. Asia Pacific is the fastest-growing region, driven by the structural scale of government-backed digitisation programmes across India, China, and Southeast Asia. The structural divergence between mature replacement markets (North America, Europe) and high-growth greenfield or first-adoption markets (Asia Pacific, The Middle East, Africa) defines the regional investment thesis for the forecast period.

- North America Hospital Information System Market

North America holds the largest HIS market share globally, driven overwhelmingly by the United States. The HITECH Act created the world's most comprehensively EHR-adopted inpatient hospital market — above 96% adoption for core EHR in hospitals with more than 100 beds, per ONC. The current growth driver is no longer EHR first-adoption but upgrade cycles, interoperability investment, and AI capability layer deployment. Canada is in active provincial HIE integration phases, with Ontario Health and BC Health Information Exchange programmes creating demand for interoperability infrastructure. Mexico's public health system is in earlier-stage HIS investment, with IMSS (Instituto Mexicano del Seguro Social) leading deployment activity.

- Europe Hospital Information System Market

Europe holds approximately 24% of global HIS market revenue, with Germany and the U.K. as the dominant national markets. Germany's Hospital Future Act (Krankenhauszukunftsgesetz), which allocated EUR 4.3 Bn for hospital digitalisation from 2021, created substantial near-term procurement activity concentrated in EHR, digital patient management, and telemedicine integration. The U.K.'s NHS Digital transformation programme continues to drive HIS investment across foundation trusts. The incoming European Health Data Space (EHDS) regulation is creating market opportunity for interoperability platform vendors as EU health systems prepare for cross-border data portability obligations.

- Asia Pacific Hospital Information System Market

Asia Pacific is the fastest-growing HIS region globally. India's Ayushman Bharat Digital Mission has issued over 600 Mn digital health IDs and is actively incentivising hospital HIS adoption across 28 states — the largest single digital health programme by population reach in history. China's national Health Information Exchange programme is connecting provincial health networks with standardised data sharing protocols, creating demand for interoperability-capable HIS platforms among both domestic and multinational vendors. South Korea's advanced health IT infrastructure is evolving from EHR adoption to AI and precision medicine data integration. Australia's My Health Record platform continues to drive integration investment.

- Latin America Hospital Information System Market

Latin America holds approximately 6% of global HIS market revenue, with Brazil driving regional activity as the largest healthcare economy in the region. Brazil's Rede Nacional de Dados em Saúde (RNDS) — the national health data network — is creating standardised interoperability requirements that favour vendors with FHIR-compliant architectures. Argentina and Colombia have active public health IT investment programmes at the ministry level. The region faces the twin constraints of public health budget limitations and HIT workforce shortage, which moderate deployment velocity relative to policy ambition.

- The Middle East Hospital Information System Market

The Middle East is one of the highest-growth regional markets for hospital information systems, anchored by Saudi Arabia's Vision 2030 health IT infrastructure investment. The Saudi Ministry of Health is executing a national HIS modernisation programme that represents one of the largest single-country HIS procurement programmes globally. The UAE's Smart Health initiative and Qatar's National Health IT Strategy are creating parallel demand vectors across the GCC. Epic Systems and Cerner (Oracle Health) have both established regional presence to serve GCC anchor contracts. Israel's health system, notable for decades-long Clalit Health Services HIS deployment, serves as a regional reference case for large-population HIS integration.

- Africa Hospital Information System Market

Africa represents the smallest HIS market share by revenue — approximately 3% in 2025 — but contains some of the fastest-growing deployment activity in absolute terms as government and NGO-funded health IT programmes expand. South Africa's public health system is the most advanced HIS market on the continent, with the National Health Insurance (NHI) programme creating demand for integrated patient record infrastructure. Egypt's Universal Health Insurance programme is driving HIS adoption across newly enrolled population cohorts. Nigeria and Kenya have active health IT investment programmes at the state and national level, though implementation bandwidth remains constrained by workforce limitations.

Full Country Coverage

|

Region |

Countries Covered |

|

North America |

The U.S., Canada, Mexico |

|

Europe |

Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe |

|

Asia Pacific |

China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific |

|

Latin America |

Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America |

|

The Middle East |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

Africa |

South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa |

**Country-level market sizing, historical data, and forecasts available for all geographies listed. Custom regional add-ons available — contact sales@zionmarketresearch.com

Hospital Information System Market: Competitive Landscape

- The global hospital information system market is concentrated at the top — Epic Systems and Oracle Health collectively command an estimated 40–50% of U.S. market revenue — but fragmented beyond the leading tier, with dozens of regional and specialty vendors competing for mid-market, ambulatory, and emerging market segments. The primary competitive differentiator is no longer functional completeness (all major platforms cover core EHR, clinical, and administrative workflows) but integration depth, AI capability roadmap, and implementation track record.

- Key players operating in the Global Hospital Information System market include Epic Systems Corporation (USA), Oracle Health (USA), Allscripts Healthcare Solutions (USA), Meditech (USA), McKesson Corporation (USA), Philips Healthcare (Netherlands), GE HealthCare (USA), Siemens Healthineers (Germany), Infor (USA), InterSystems Corporation (USA), Netsmart Technologies (USA), and Athenahealth (USA).

|

Company |

HQ Country |

Primary Focus |

Key Strategy |

Notable Recent Action |

|

Epic Systems |

USA |

Full-suite EHR & HIS |

Platform lock-in via deep integration & API ecosystem |

Expanded Middle East deployments; launched AI CDS module (2024) |

|

Oracle Health |

USA |

Cloud EHR & clinical AI |

AI-native EHR via Oracle Cloud Infrastructure |

AI Clinical Documentation Assistant deployment (2023–2024) |

|

Allscripts |

USA |

Ambulatory & population health |

Open platform interoperability |

Rebranded as Veradigm; refocused on data analytics (2023) |

|

Meditech |

USA |

Community & critical access hospitals |

Web-based EHR for mid-market |

Expanded cloud-hosted Expanse EHR internationally |

|

McKesson |

USA |

Health IT distribution & RCM |

Revenue cycle & supply chain integration |

Continued pharmacy management platform expansion |

|

Philips Healthcare |

Netherlands |

Radiology & ICU information systems |

Diagnostic informatics & patient monitoring integration |

AI-powered radiology workflow integration launched (2024) |

|

GE HealthCare |

USA |

Imaging & clinical operations IT |

Imaging AI & care area management |

Edison AI platform integrated with partner EHRs |

|

Siemens Healthineers |

Germany |

Imaging informatics & diagnostics |

Digital ecosystem for imaging-to-EHR integration |

Teamplay Digital Health Platform expanded in Europe (2024) |

|

Infor |

USA |

Healthcare operations & supply chain |

Cloud ERP for health system operations |

CloudSuite Healthcare platform update (2023) |

|

InterSystems |

USA |

HealthShare interoperability platform |

HIE and data integration infrastructure |

HealthShare Personal Community platform update |

|

Netsmart Technologies |

USA |

Behavioural health & human services |

EHR for mental health, substance use, I/DD settings |

myAvatar EHR platform enhancements |

|

Athenahealth |

USA |

Ambulatory EHR & RCM |

Cloud-native ambulatory EHR & network intelligence |

athenaOne network intelligence features expanded |

- Three strategic themes define the competitive set. First, AI capability is now a table-stakes differentiator — every major vendor has launched or announced AI-integrated modules. Second, the market is bifurcating between full-suite enterprise vendors (Epic, Oracle Health) and best-of-breed specialists in high-growth segments (Netsmart for behavioural health, Athenahealth for ambulatory). Third, international expansion — particularly into the Middle East and Asia Pacific — is a primary growth vector for U.S. and European vendors facing a maturing domestic replacement market.

Recent Developments in the Hospital Information System Market

Strategic activity in the hospital information system market accelerated through 2023–2024, with AI capability launches, international market entries, and regulatory-driven platform upgrades dominating the development calendar.

|

Date |

Company |

Type |

Description |

Market Impact |

|

Feb 2024 |

Oracle Health |

Product Launch |

Launched AI Clinical Documentation Assistant integrated into Oracle Health EHR for inpatient and ambulatory settings. |

Targets physician documentation burden; positions Oracle Health in AI-native EHR competition. |

|

Oct 2023 |

Epic Systems |

Market Expansion |

Expanded Middle East partnership programme, adding GCC health networks under Saudi Vision 2030 digital health mandate. |

Strengthens Epic's international footprint; confirms GCC as priority growth geography. |

|

Mar 2024 |

Siemens Healthineers |

Partnership |

Announced expanded Teamplay Digital Health Platform integration with third-party European HIS vendors. |

Accelerates imaging-to-EHR workflow automation across European markets. |

|

Jan 2024 |

Philips Healthcare |

Product Launch |

Launched AI-powered radiology workflow integration module connecting PACS and EHR systems. |

Deepens imaging informatics integration; strengthens Philips in radiology-adjacent HIS. |

|

Sep 2023 |

Athenahealth |

Platform Update |

Expanded athenaOne network intelligence features for ambulatory care revenue cycle optimisation. |

Reinforces Athenahealth position in ambulatory EHR and cloud-native RCM segment. |

|

Nov 2023 |

GE HealthCare |

Partnership |

Extended Edison AI platform partnerships with EHR vendors for care area management data integration. |

Broadens GE HealthCare AI capabilities beyond imaging into operational HIS. |

About Zion Market Research

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is updated constantly in order to fulfil our clients' requirements for prompt and direct online access. Keeping in mind the client's needs, we have included expert insights on global industries, products, and market trends in this database.

Author:

Mr. Nilesh Patil

Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067

Table Of Content

Methodology

FrequentlyAsked Questions

The ZION MARKET RESEARCH Hospital Information System Market Report is a 300+ page PDF delivering global market sizing (historical 2019–2024 and forecast 2026–2034), segmentation analysis across 5 dimensions (component, deployment model, application, end user, region), country-level forecasts for 35+ geographies, competitive landscape analysis with profiles of 12 companies, DROC analysis (drivers, restraints, opportunities, challenges), and 120 tables with 85 figures.

The Global Hospital Information System market was valued at USD 16,340 Mn in 2025. Zion Market Research projects the market to reach USD 48,720 Mn by 2034, advancing at a CAGR of 12.9% during 2026–2034. North America leads by regional share; Asia Pacific leads by growth rate.

The ZION MARKET RESEARCH report segments the Hospital Information System market across 5 dimensions: By Component (Software, Hardware, IT Infrastructure & Networking Services, Professional Services); By Deployment Model (On-Premise, Cloud-Based, Hybrid); By Application (EHR, Hospital Management, RCM, Patient Portal, Clinical Decision Support, Pharmacy Management); By End User (Hospitals, Specialty Clinics, ASCs, Long-term Care Facilities, Pharmacies); and By Region (6 ZION MARKET RESEARCH standard regions).

The report covers 35+ countries across all 6 ZION MARKET RESEARCH regions. North America: The U.S., Canada, Mexico. Europe: Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe. Asia Pacific: China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific. Latin America: Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America. The Middle East: GCC countries (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East. Africa: South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa. The Middle East and Africa are always covered as separate regions — never combined.

ZION MARKET RESEARCH offers custom scope options including: additional market segments beyond the 5 standard dimensions; extended geographic coverage or country-specific deep-dives; extended forecast periods; company-specific competitive analysis; and custom data tables for specific use cases. Contact sales@zionmarketresearch.com or +1 (302) 444-0166 to discuss customization requirements.

Three access options are available: (1) Request a free sample to preview data tables, segmentation framework, and regional coverage before purchasing; (2) Purchase the full 300+ page PDF report for immediate download; (3) Submit a research inquiry for custom scope or analyst consultation. Contact: Email: sales@zionmarketresearch.com | Phone: +1 (302) 444-0166 | Toll Free: +1 (855) 465-4651

List of Contents

Hospital Information System Industry Perspective:Hospital Information System OverviewKey InsightsWhy Choose the Zion Market ResearchsMarket Report?Hospital Information System Dynamics (Drivers, Restraints, Opportunities, Challenges)Hospital Information System Report ScopeHospital Information System SegmentationHospital Information System Regional AnalysisFull Country CoverageHospital Information System Competitive LandscapeRecent Developments in theMarketAbout Zion Market ResearchHappyClients