Ferrosilicon Market Size, Trend, Growth, Industry Analysis Report 2034

Ferrosilicon Market By Type (Atomized Ferrosilicon and Milled Ferrosilicon), By Application (Deoxidizer, Inoculants and Others), By End-use (Carbon & Other Alloy Steel, Electric Steel, Stainless Steel, Cast Iron and Others) and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 11.8 Billion | USD 15.8 Billion | 3.0% | 2024 |

Ferrosilicon Industry Perspective:

What will be the size of the global ferrosilicon market during the forecast period?

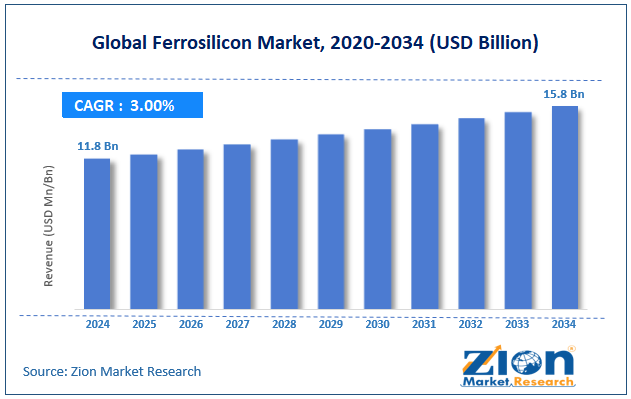

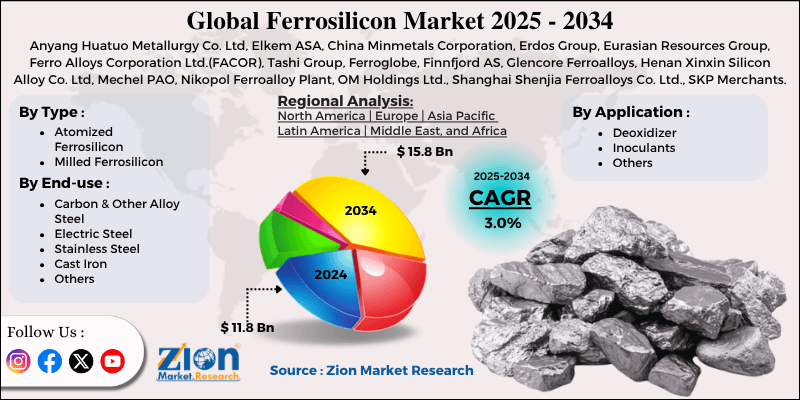

The global ferrosilicon market size was worth around USD 11.8 billion in 2024 and is predicted to grow to around USD 15.8 billion by 2034 with a compound annual growth rate (CAGR) of roughly 3.0% between 2025 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global Ferrosilicon market is estimated to grow annually at a CAGR of around 5.8% over the forecast period (2025-2034).

- In terms of revenue, the global Ferrosilicon market size was valued at around USD 195 billion in 2024 and is projected to reach USD 343 billion by 2034.

- Expansion of construction & infrastructure activities is expected to propel the Ferrosilicon market over the projected period.

- Based on the type, the atomized ferrosilicon segment captures the largest market share in 2024 of over 55%.

- Based on the application, the deoxidizer dominated the market with a revenue share of 68%.

- Based on the end-use, the carbon & other alloy steel hold the majority of market share of 44% in the ferrosilicon market.

- Based on region, the Asia Pacific captures the largest market share in 2024 of over 65%.

Ferrosilicon Market: Overview

Ferrosilicon is one of the important ferroalloys, whose major components are iron and silicon, with 15 to 90 percent silicon content, and is used as a key ingredient in various metallurgical processes. The substance is normally produced by reducing silica (SiO2) with coke in electric arc furnaces. Ferrosilicon is used across many industries and applications due to its unique properties. In steel manufacturing, for example, ferrosilicon is used as a reducing agent to remove oxygen impurities from molten steel and as an alloying ingredient that improves the physical and mechanical properties of metals. Another important field of use for this material is the casting industry, where ferrosilicon can be used to regulate microstructure and increase machinability of cast irons. Besides metallurgy, ferrosilicon is employed in the chemical industry to manufacture silicon compounds and electrical steels.

Impact of the USA-Israel War on Iran on the Ferrosilicon Market

In terms of its implications for the ferrosilicon industry, the current conflict between the United States and Israel against Iran has generated a negative domino effect. As a result of destruction at Iranian steel production facilities and import restrictions, steel production in the region will decline, as ferrosilicon is an important ingredient in steelmaking. In addition, higher energy prices, coupled with disruptions in energy delivery, particularly through the Strait of Hormuz, have greatly affected ferroalloy production due to their high energy requirements. Despite the short-term implications, the long-term effects are minimal because Iran makes only a small contribution to the international supply.

Ferrosilicon Market: Dynamics

Growth Drivers

Why does the rising demand from the steel industry drive the ferrosilicon market?

Demand from the steel industry is the most important determinant of the ferrosilicon market. This is because ferrosilicon is an integral component of steel production. Firstly, ferrosilicon is an excellent deoxidizer that removes oxygen from molten steel, improving its quality. An increase in the quantity of steel produced due to high demand for construction materials, infrastructure projects, cars, and equipment manufacturing increases the need for deoxidizers, such as ferrosilicon.

Secondly, ferrosilicon is an excellent alloy that enhances steel's properties. Properties of steel include strength, hardness, corrosion resistance, and magnetic properties. The increasing demand for high-performance steel, especially electrical steel, is driving demand for ferrosilicon, as it is used in transformers and electric engines required for generating electricity. Lastly, steel production is on a large scale; thus, small changes in steel output significantly increase demand for ferrosilicon. Very few alternatives have been found that can replace ferrosilicon.

Restraints

Volatility in raw material prices hinders the growth of the ferrosilicon industry

Fluctuations in the prices of raw materials adversely affect the development of the ferrosilicon industry, as it requires major raw materials such as silica (quartz), iron ore, and carbon-reducing agents. With the increase in raw material prices, due to factors such as limited mining activity, political conflicts, or transportation issues, the manufacturing process will be adversely affected, as production will become more expensive. Moreover, this problem will create difficulties in stabilizing prices, especially in a competitive environment. In addition, it becomes difficult for firms to make accurate predictions about their future operations, as costs may change at any time without notice.

Opportunities

How does the growth of the renewable energy & electronics sector offer a lucrative opportunity for the ferrosilicon market?

The development of the renewable energy and electronics industries constitutes another significant market opportunity for ferrosilicon, as evidenced by expansion trends and official government data. According to government information, India's renewable energy capacity amounted to 283.46 GW by March 2026, while renewables have played a substantial role not only in total energy output but also in covering over 51% of peak demand. Moreover, the target of achieving 500 GW of capacity by 2030, with 280 GW from solar energy alone, requires significant use of equipment such as transformers and motors, and, in turn, of electrical steel enriched with silicon, thereby increasing the demand for ferrosilicon.

On the international as well as domestic scene, renewables continue to show impressive growth, reaching 580 GW worldwide in 2024 and annual growth rates in excess of 7%, while in India, more than 22 GW have been added in the first half of 2025 (56% y-o-y growth). Finally, the development of the electronics industry, which relies heavily on silicon-based components such as semiconductors and consumer devices, drives demand for ferrosilicon, as it is used in the production of silicon and specialized steels.

Challenges

Why do the high energy consumption and production costs pose a significant challenge to the ferrosilicon market?

The high energy consumption and production costs are another critical issue for the ferrosilicon industry, as the production process is highly energy-intensive. Ferrosilicon production takes place at high temperatures (1,500–2,000°C) in electric arc furnaces and thus requires a continuous high electricity input. In this case, the energy bill becomes an important share of the total production cost and might even be the main one. Any increase in electricity prices due to higher fuel costs, electricity shortages, or other factors will impose additional costs on producers, and since ferrosilicon is a commodity good, companies cannot always pass these costs on to buyers and still maintain profits.

Besides the cost issue, higher energy costs are likely to increase pressure on producers regarding environmental legislation, as they lead to higher CO2 emissions. Thus, the company needs to spend additional money not only on environmental technologies but also on taxes, which increases costs. Lastly, volatile electricity costs negatively influence a business's decision-making process.

Ferrosilicon Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Ferrosilicon Market |

| Market Size in 2024 | USD 11.8 Billion |

| Market Forecast in 2034 | USD 15.8 Billion |

| Growth Rate | CAGR of 3.0% |

| Number of Pages | 226 |

| Key Companies Covered | Anyang Huatuo Metallurgy Co. Ltd, Elkem ASA, China Minmetals Corporation, Erdos Group, Eurasian Resources Group, Ferro Alloys Corporation Ltd.(FACOR), Tashi Group, Ferroglobe, Finnfjord AS, Glencore Ferroalloys, Henan Xinxin Silicon Alloy Co. Ltd, Mechel PAO, Nikopol Ferroalloy Plant, OM Holdings Ltd., Shanghai Shenjia Ferroalloys Co. Ltd., SKP Merchants, and others. |

| Segments Covered | By Type, By Application, By End-use, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Ferrosilicon Market: Segmentation

Type Insights

Why does the atomized ferrosilicon dominate the ferrosilicon market?

The atomized ferrosilicon segment captures the largest market share in 2024 of over 55%. The main reason for its growth is its increasing use in specialized and high-end applications. Atomized ferrosilicon, which comes in the form of a spherical powder, is extensively applied in dense media separation (DMS) processes in mineral processing, especially in cases like coal washing and diamond production, where high accuracy is essential. Rising global demand for minerals and enhanced ore recovery are boosting its use. Its use in other advanced applications, such as welding electrodes, metal powders, and heavy media separation in the recycled materials industry, is also driving demand.

Application Insights

How does the deoxidizer capture the largest market share in the ferrosilicon market?

The deoxidizer dominated the market with a revenue share of 68%. This increase is attributed to its importance in steel production. The major use of ferrosilicon is as a deoxidizing agent, reducing the oxygen content of molten steel. This minimizes the likelihood of flaws like porosity. The growing demand for deoxidizers reflects the increasing production of steel worldwide for various reasons.

End-use Insights

Does the carbon & other alloy steel segment dominate the ferrosilicon market?

The carbon & other alloy steel hold the majority of market share of 44% in the ferrosilicon market. Ferrosilicon is an important raw material in the production process of steel, where it is used as a deoxidizer and alloy agent. Ferrosilicon powder can release a large amount of heat when burned at high temperatures; hence, it is also used as a heat-producing agent in the production of capped steel.

Regional Insights

Why does the Asia Pacific lead the ferrosilicon market?

The Asia Pacific captures the largest market share in 2024 of over 65%. The market's growth is mainly driven by the rapid pace of industrialization, increased steel production, and massive infrastructure development in nations such as China, India, and Japan. The region is also the largest producer and consumer of steel, where massive investments in construction, transport, and urbanization projects have consistently increased demand for high-quality steel, thereby driving demand for ferrosilicon, which serves as the main deoxidizer and alloy in steelmaking. In addition, the growth of the automobile industry and heavy industries in the Asia Pacific region has contributed to the increased demand for steel.

Ferrosilicon Market: Competitive Analysis

The global ferrosilicon market is dominated by players like;

- Anyang Huatuo Metallurgy Co. Ltd

- Elkem ASA

- China Minmetals Corporation

- Erdos Group

- Eurasian Resources Group

- Ferro Alloys Corporation Ltd.(FACOR)

- Tashi Group

- Ferroglobe

- Finnfjord AS

- Glencore Ferroalloys

- Henan Xinxin Silicon Alloy Co. Ltd

- Mechel PAO

- Nikopol Ferroalloy Plant

- OM Holdings Ltd.

- Shanghai Shenjia Ferroalloys Co. Ltd.

- SKP Merchants

The global ferrosilicon market is segmented as follows:

By Type

- Atomized Ferrosilicon

- Milled Ferrosilicon

By Application

- Deoxidizer

- Inoculants

- Others

By End-use

- Carbon & Other Alloy Steel

- Electric Steel

- Stainless Steel

- Cast Iron

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Ferrosilicon is one of the important ferroalloys, whose major components are iron and silicon, with 15 to 90 percent silicon content, and is used as a key ingredient in various metallurgical processes.

Rising global steel production, rapid infrastructure and industrial development, increasing demand for high-performance and electrical steels, and expanding applications in automotive, renewable energy, and manufacturing sectors drives the industry growth.

The major challenge is the high energy consumption and electricity costs, volatile raw material prices, stringent environmental regulations, and supply chain disruptions impacting production stability and profitability.

Based on the application, the deoxidizer segment is expected to dominate the ferrosilicon market growth during the projected period.

Adoption of energy-efficient and low-emission smelting technologies, increasing use of ferrosilicon in electric arc furnace (EAF) steelmaking, rising demand for high-purity and specialty grades, and growing integration of automation and sustainable production practices are key innovations shaping the market.

According to the report, the global ferrosilicon market size was worth around USD 11.8 billion in 2024 and is predicted to grow to around USD 15.8 billion by 2034.

The global ferrosilicon market is expected to grow at a CAGR of 3.0% during the forecast period.

The global ferrosilicon industry growth is expected to be led by the Asia Pacific over the forecast period.

The global ferrosilicon market is dominated by players like Anyang Huatuo Metallurgy Co., Ltd, Elkem ASA, China Minmetals Corporation, Erdos Group, Eurasian Resources Group, Ferro Alloys Corporation Ltd. (FACOR), Tashi Group, Ferroglobe, Finnfjord AS, Glencore Ferroalloys, Henan Xinxin Silicon Alloy Co.,Ltd, Mechel PAO, Nikopol Ferroalloy Plant, OM Holdings Ltd., Shanghai Shenjia Ferroalloys Co. Ltd. and SKP Merchants among others.

The market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients