Farmed Bluefin Tuna Market Size, Share, Trends, Growth and Forecast 2034

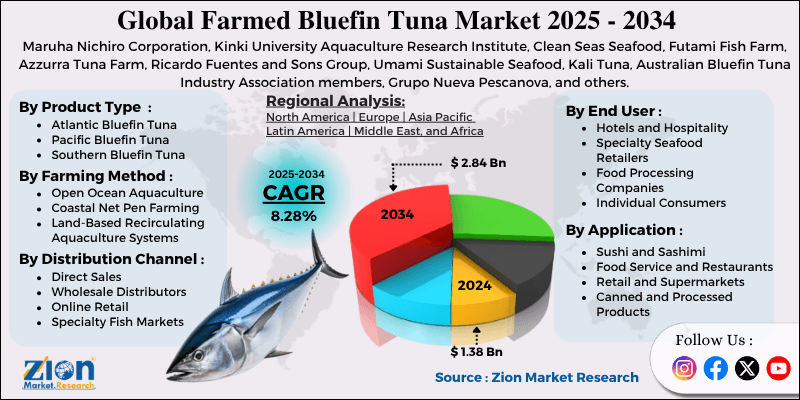

Farmed Bluefin Tuna Market By Product Type (Atlantic Bluefin Tuna, Pacific Bluefin Tuna, Southern Bluefin Tuna), By Farming Method (Open Ocean Aquaculture, Coastal Net Pen Farming, Land-Based Recirculating Aquaculture Systems), By Application (Sushi and Sashimi, Food Service and Restaurants, Retail and Supermarkets, Canned and Processed Products), By End-User (Hotels and Hospitality, Specialty Seafood Retailers, Food Processing Companies, Individual Consumers), By Distribution Channel (Direct Sales, Wholesale Distributors, Online Retail, Specialty Fish Markets), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 1.38 Billion | USD 2.84 Billion | 8.28% | 2024 |

Farmed Bluefin Tuna Industry Perspective:

What will be the size of the farmed bluefin tuna market during the forecast period?

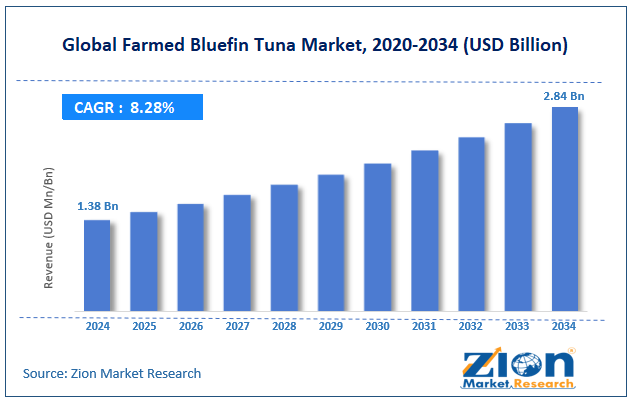

The global farmed bluefin tuna market size was worth approximately USD 1.38 billion in 2024 and is projected to grow to around USD 2.84 billion by 2034, with a compound annual growth rate (CAGR) of roughly 8.28% between 2025 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global farmed bluefin tuna market is estimated to grow annually at a CAGR of around 8.28% over the forecast period (2025–2034).

- In terms of revenue, the global farmed bluefin tuna market size was valued at approximately USD 1.38 billion in 2024 and is projected to reach USD 2.84 billion by 2034.

- The farmed bluefin tuna market is projected to grow significantly due to rising global demand for premium sushi and sashimi, ongoing restrictions on wild bluefin tuna catch quotas, growing consumer preference for sustainably sourced seafood, increasing investments in advanced aquaculture technologies, and expanding international trade of high-value seafood products to luxury food markets in North America, Europe, and Asia.

- Based on product type, the Pacific bluefin tuna segment is expected to lead the farmed bluefin tuna market. In contrast, the Atlantic bluefin tuna segment is anticipated to grow at a notable pace.

- Based on farming method, the coastal net pen farming segment is expected to lead the farmed bluefin tuna market. In contrast, the land-based recirculating aquaculture systems segment is anticipated to grow at the fastest rate.

- Based on application, the sushi and sashimi segment is expected to lead the farmed bluefin tuna market, while the food service and restaurants segment is anticipated to grow significantly.

- Based on end-user, the hotels and hospitality segment is the largest current end-user group, while the specialty seafood retailers segment is anticipated to grow most rapidly.

- Based on distribution channel, the wholesale distributors segment is expected to lead the farmed bluefin tuna market, while the online retail segment is anticipated to grow steadily.

- Based on region, the Asia Pacific is projected to dominate the global farmed bluefin tuna market during the estimated period, followed by Europe.

Farmed Bluefin Tuna Market: Overview

Farmed bluefin tuna is bluefin tuna that is raised in controlled farming systems instead of being caught from the wild ocean. It is one of the most valuable and expensive fish in the world, especially in Japan, where it is highly preferred for sushi and sashimi. The fish is known for its rich taste, fatty texture, and deep red color, making it a favorite among chefs and seafood lovers. Earlier, most bluefin tuna were caught in the wild, leading to overfishing and a sharp decline in wild fish populations. To protect these stocks, governments introduced strict fishing limits. However, this created a supply shortage because demand for bluefin tuna remained very high in global markets. To address this problem, fish farming emerged as an important alternative. In farming, young tuna is either caught and grown in large sea cages or bred and raised entirely in controlled systems. Japan was the first country to farm bluefin tuna through its full life cycle successfully. Today, countries like Australia, Spain, Croatia, Mexico, and Turkey are also involved in bluefin tuna farming.

The growing global appetite for sushi and Japanese cuisine, combined with tightening restrictions on wild bluefin tuna fishing, increasing consumer awareness of sustainability, and continued advances in aquaculture technology, is expected to drive strong and consistent growth in the farmed bluefin tuna market throughout the forecast period.

Farmed Bluefin Tuna Market: Technology Roadmap 2025–2034

What is the projected development roadmap of the farmed bluefin tuna market over the forecast period?

The farmed bluefin tuna market is evolving due to advances in breeding technologies, improved feed, the expansion of land-based farming, stricter sustainability standards, and greater acceptance among premium consumers and chefs. The market is expected to grow at a CAGR of around 8.28% over the forecast period, driven by strong demand across premium dining, sushi restaurants, luxury retail, and international seafood trade segments.

The following roadmap outlines key development phases expected through 2034.

2025–2027: Breeding Technology and Feed Efficiency Phase

- Fish farms are expected to improve their ability to breed bluefin tuna in controlled environments, reducing reliance on wild juvenile capture and stabilizing production.

- High-protein feed formulations are likely to evolve, helping tuna grow faster while maintaining desired taste and fat quality.

- Farmers are projected to increasingly adopt underwater cameras, water sensors, and automated feeding systems to monitor fish health and reduce losses.

2028–2031: Sustainable Scaling and Market Expansion Phase

- Land-based farming systems are expected to expand at larger scales, enabling tuna production in inland regions and lowering environmental impact.

- Sustainability certifications and traceability systems are likely to become standard, encouraging more transparent supply chains.

- Demand is projected to grow in regions such as the Middle East, Southeast Asia, and Latin America as sushi consumption increases.

2032–2034: Precision Aquaculture and Global Trade Phase

- Artificial intelligence is expected to be widely used to monitor fish health and growth in real time, improving overall efficiency.

- Genetic research is likely to support the selective breeding of tuna with faster growth and stronger disease resistance.

- Farmed bluefin tuna is projected to be traded globally through digital platforms with clear pricing, quality grading, and sustainability information.

Farmed Bluefin Tuna Market: Dynamics

Growth Drivers

What is driving demand for farmed bluefin tuna as global sushi culture and premium seafood consumption continue to expand?

The farmed bluefin tuna market is growing steadily as sushi and Japanese cuisine continue to gain popularity across a wide range of countries and consumer groups worldwide. What was once considered a niche dining option limited to Japan and a few global cities has now become a common food choice across North America, Europe, the Middle East, Southeast Asia, and even parts of Africa. A large number of new sushi restaurants are opening in both metropolitan and smaller cities, while supermarkets are also expanding their offerings of ready-to-eat sushi and fresh seafood products. Bluefin tuna is widely regarded as the highest quality fish used in sushi and sashimi due to its deep red color, rich flavor, and high fat content, especially in the premium fatty cut known as toro. As more consumers develop a taste for sushi, the demand for bluefin tuna continues to rise steadily. However, strict fishing limits on wild bluefin tuna have reduced supply, prompting restaurants and seafood buyers to rely on farmed bluefin tuna for consistent availability.

Restrictions on wild bluefin tuna fishing and rising sustainability awareness are creating lasting demand for farmed alternatives.

The farmed bluefin tuna industry is expanding rapidly as global efforts to protect wild tuna populations continue to encourage a shift toward more sustainable, controlled seafood sources. Strict fishing regulations introduced by international bodies have improved conservation while also creating opportunities for aquaculture to meet global demand in a stable and scalable way. This has positioned farmed bluefin tuna as a reliable alternative that supports long-term supply without depending on seasonal fishing cycles or natural stock variations. Seafood businesses, especially premium sushi restaurants and luxury hotels, are increasingly adopting farmed bluefin tuna because it offers consistent quality, predictable availability, and the ability to plan menus without supply uncertainty.

In addition, growing awareness around sustainability is positively influencing purchasing decisions, with consumers and businesses actively preferring seafood that is responsibly sourced and traceable. Farmed bluefin tuna meets these expectations by offering clear production visibility and improving environmental standards through advanced aquaculture practices. As a result, it is gaining strong acceptance among high-end buyers and retail chains, further supporting market growth. This combination of regulatory support, reliable supply, and rising demand for sustainability is significantly driving the expansion of the farmed bluefin tuna market worldwide.

Restraints

How do high production costs and long growth cycles create challenges for operators in the farmed bluefin tuna market?

The farmed bluefin tuna market faces growth limitations due to the high cost and complexity of production compared to other farmed fish. Bluefin tuna are large, active fish that require large amounts of feed, mainly smaller fish or fish-based feed, which increases overall production expenses. Unlike other species that can use plant-based feed, bluefin tuna farming still depends on costly marine-based nutrition. In addition, the time needed to grow bluefin tuna to market size is much longer, often taking several years, which increases operational costs and financial risk for producers. This long cycle also means that farms must invest more capital and wait longer to see returns. Any disruption, such as disease, poor water conditions, or extreme weather, can lead to major losses during this period. These challenges make production less flexible and harder to scale quickly. As a result, farmed bluefin tuna remains a premium product with a high selling price, limiting its reach to a smaller group of high-end consumers and restricting overall market expansion.

Opportunities

How is the growing global middle class and expanding luxury food culture creating new opportunities for the farmed bluefin tuna market?

The farmed bluefin tuna market is seeing strong growth opportunities amid rising demand for luxury food in emerging economies. Countries such as China, South Korea, the United Arab Emirates, Singapore, and Brazil are experiencing rising incomes, creating a larger group of consumers willing to spend on premium dining experiences. As a result, high-end sushi restaurants are expanding rapidly in major cities, increasing demand for top-quality ingredients such as bluefin tuna. This trend is opening new markets for farmed bluefin tuna producers beyond traditional regions such as Japan, the United States, and Western Europe. At the same time, improved cold storage, transport systems, and seafood logistics are making it easier to supply fresh, high-grade tuna to distant markets.

In addition, the growing interest in gourmet cooking at home is creating new sales channels for producers. Many consumers now want restaurant-quality sushi at home, and online seafood platforms are making this possible through direct delivery. This allows producers to sell directly to customers, improve profit margins, and expand their reach, creating strong long-term opportunities for the farmed bluefin tuna market.

Challenges

Environmental concerns, regulatory pressures, and the ethical debate over ranching juvenile wild fish are impacting the market.

The farmed bluefin tuna industry faces several challenges related to environmental impact and concerns about certain farming practices. A common method is tuna ranching, in which young wild fish are caught and then grown in sea cages until they reach market size. While this method helps meet demand, it still depends on wild fish and raises concerns about long-term sustainability. Experts worry that catching juvenile fish may affect future fish populations.

In addition, farming in ocean net pens can impact the surrounding marine environment through fish waste, leftover feed, and chemical use, which may affect water quality and nearby sea life. Local communities in some regions have also raised concerns about these environmental effects. To address these issues, producers need to invest in better waste management systems and improved farming methods, which can increase costs. Another major challenge is the differences in regulations across countries, as changes to fishing limits, permits, and environmental standards can create uncertainty for producers and complicate long-term planning in the farmed bluefin tuna market.

Farmed Bluefin Tuna Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Farmed Bluefin Tuna Market |

| Market Size in 2024 | USD 1.38 Billion |

| Market Forecast in 2034 | USD 2.84 Bllion |

| Growth Rate | CAGR of 8.28% |

| Number of Pages | 227 |

| Key Companies Covered | Maruha Nichiro Corporation, Kinki University Aquaculture Research Institute, Clean Seas Seafood, Futami Fish Farm, Azzurra Tuna Farm, Ricardo Fuentes and Sons Group, Umami Sustainable Seafood, Kali Tuna, Australian Bluefin Tuna Industry Association members, Grupo Nueva Pescanova, and others. |

| Segments Covered | By Product Type, By Farming Method,By Application, By End-User, By Distribution Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Farmed Bluefin Tuna Market: Segmentation

The global farmed bluefin tuna market is segmented by product type, farming method, application, end-user, distribution channel, and region.

What makes the Pacific bluefin tuna segment the expected leader in the farmed bluefin tuna market?

Based on product type, the global farmed bluefin tuna market is categorized into Atlantic bluefin tuna, Pacific bluefin tuna, and Southern bluefin tuna. The Pacific bluefin tuna segment holds approximately 54% of the global market share. It is expected to remain dominant, driven by Japan's well-established, technically advanced farming industry and strong domestic and export demand for this species in the premium sushi market. The Atlantic bluefin tuna segment holds around 28% share and is growing at a notable rate, supported by expanding farming operations in the Mediterranean region, particularly in Spain, Croatia, and Malta, as well as rising European and North American demand for locally farmed premium seafood.

How does coastal net pen farming maintain its leading position in the farmed bluefin tuna market?

Based on farming method, the farmed bluefin tuna market is divided into open-ocean aquaculture, coastal net-pen farming, and land-based recirculating aquaculture systems. The coastal net pen farming segment accounts for approximately 61% of the global market share, driven by its relatively lower infrastructure costs and ability to provide the large swimming volumes that bluefin tuna require to thrive and develop their characteristic muscle quality. The land-based recirculating aquaculture systems segment holds around a 15% share. It is growing at the fastest rate, supported by strong investor interest, environmental advantages, and the ability to produce bluefin tuna in locations far from the ocean.

Why does the sushi and sashimi application segment lead the farmed bluefin tuna market?

Based on application, the farmed bluefin tuna industry is segregated into sushi and sashimi, food service and restaurants, retail and supermarkets, and canned and processed products. The sushi and sashimi segment leads the market with approximately 49% of global market share, driven by the overwhelmingly high value placed on bluefin tuna in Japanese cuisine and the rapid global spread of sushi dining culture. Bluefin tuna is the centerpiece of premium sushi menus, commanding prices far above those of other seafood options and driving strong, consistent demand. The food service and restaurants segment holds around 27% share and is growing significantly as upscale dining establishments worldwide increasingly feature farmed bluefin tuna as a premium menu ingredient.

What makes the hotels and hospitality segment lead the farmed bluefin tuna end-user market?

Based on end-user, the farmed bluefin tuna market is categorized into hotels and hospitality, specialty seafood retailers, food processing companies, and individual consumers. The hotels and hospitality segment accounts for approximately 38% of the global market share and continues to lead the market, driven by five-star hotels, luxury resorts, and fine dining establishments that serve bluefin tuna as a signature ingredient and are willing to pay premium prices for consistently high-quality supply. The specialty seafood retailers segment holds around 24% of the market share. It is growing most rapidly, supported by rising consumer demand for high-quality at-home dining experiences and the expansion of premium food retail in major urban markets worldwide.

How does the wholesale distributors channel dominate the distribution landscape of the farmed bluefin tuna market?

Based on distribution channel, the farmed bluefin tuna market is classified into direct sales, wholesale distributors, online retail, and specialty fish markets. The wholesale distributors segment accounts for around 44% of the global market and is expected to remain dominant, as most farmed bluefin tuna is supplied through established seafood wholesale networks. The online retail segment holds around 18% share. It is growing steadily, particularly in North America and Japan, where consumers and small restaurants are increasingly comfortable ordering sashimi-grade premium seafood directly through digital platforms with overnight refrigerated delivery.

Farmed Bluefin Tuna Market: Regional Analysis

How does Asia Pacific's unique combination of culinary tradition, aquaculture expertise, and consumer demand drive its dominance in the farmed bluefin tuna market?

The farmed bluefin tuna market is led by Asia Pacific, which is expected to grow at a CAGR of around 6.8% during the forecast period and continues to dominate due to its strong seafood culture, advanced aquaculture expertise, and a large consumer base for premium sushi and sashimi. Japan plays the most important role in this regional leadership, as it represents both the highest demand and one of the most developed production systems in the world. Japanese consumers have a deep preference for high-quality bluefin tuna, and the famous seafood auctions in Tokyo act as a global benchmark for pricing and quality standards. The country has also invested heavily in research and innovation, with institutions like Kinki University and major companies such as Maruha Nichiro leading the development of full-cycle bluefin tuna farming. Japan remains the largest producer and consumer of farmed bluefin tuna, and domestic production has increased as strict limits on wild fishing push buyers toward farmed options.

In addition, countries such as South Korea, China, and Taiwan are emerging as strong consumer markets, supported by the rapid expansion of sushi restaurants, increasing urbanization, and rising disposable incomes across the region. The growing influence of Japanese cuisine across the Asia Pacific is further strengthening demand for premium seafood products, including bluefin tuna. Asia Pacific’s leadership is further reinforced by its strong regional trade networks, efficient seafood distribution systems, and continuous investments in aquaculture technology and infrastructure. Government policies in several countries are also supporting the expansion of sustainable fish farming practices. High consumer willingness to pay for premium seafood continues to drive consistent demand. These combined factors ensure that the Asia Pacific will remain the leading region in the global farmed bluefin tuna market throughout the forecast period.

What factors make Europe the second-largest market for farmed bluefin tuna?

The farmed bluefin tuna market sees Europe as the second-largest region, projected to grow at a CAGR of around 5.9% during the forecast period, supported by its strong role in both production and consumption. The Mediterranean Sea has long been an important area for bluefin tuna, and countries such as Spain, Croatia, Malta, and Turkey have built well-established farming and ranching operations in this region. These countries benefit from suitable water conditions, skilled farming practices, and access to major export routes, which support consistent, high-quality tuna production. Spain stands out as Europe's leading producer, with large-scale operations in regions such as Murcia and Andalusia that supply both international and domestic markets. Croatian producers have also gained recognition for delivering premium-quality tuna, especially to Japanese buyers.

At the same time, demand for sushi and Japanese cuisine has increased significantly across Europe over the past decade, especially in major cities such as London, Paris, Amsterdam, Madrid, and Berlin. High-end restaurants are increasingly using farmed bluefin tuna to meet customer expectations for quality and consistency. European consumers and businesses also place strong importance on sustainability and traceability, which supports the growth of responsible aquaculture practices. Well-developed logistics, cold chain systems, and regulatory standards further strengthen the market. This combination of strong production capacity, rising consumer demand, and a focus on sustainability ensures that Europe remains the second-largest region in the global farmed bluefin tuna market.

Recent Market Developments

- In January 2026, BlueNalu announced a USD 11 million investment to scale up production of cell-cultured bluefin tuna toro, aiming to meet rising global demand for sustainable premium seafood alternatives.

- In December 2025, Mediterranean producers, particularly in Malta, began redirecting farmed bluefin tuna exports toward China, reflecting shifting global demand patterns and expanding consumption in Asian markets.

Farmed Bluefin Tuna Market: Competitive Analysis

The leading players in the global farmed bluefin tuna market are;

- Maruha Nichiro Corporation

- Kinki University Aquaculture Research Institute

- Clean Seas Seafood

- Futami Fish Farm

- Azzurra Tuna Farm

- Ricardo Fuentes and Sons Group

- Umami Sustainable Seafood

- Kali Tuna

- Australian Bluefin Tuna Industry Association members

- Grupo Nueva Pescanova

The global farmed bluefin tuna market is segmented as follows:

By Product Type

- Atlantic Bluefin Tuna

- Pacific Bluefin Tuna

- Southern Bluefin Tuna

By Farming Method

- Open Ocean Aquaculture

- Coastal Net Pen Farming

- Land-Based Recirculating Aquaculture Systems

By Application

- Sushi and Sashimi

- Food Service and Restaurants

- Retail and Supermarkets

- Canned and Processed Products

By End-User

- Hotels and Hospitality

- Specialty Seafood Retailers

- Food Processing Companies

- Individual Consumers

By Distribution Channel

- Direct Sales

- Wholesale Distributors

- Online Retail

- Specialty Fish Markets

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

The farmed bluefin tuna is bluefin tuna that is raised in controlled farming systems instead of being caught from the wild ocean. It is one of the most valuable and expensive fish in the world, especially in Japan, where it is highly preferred for sushi and sashimi.

The global farmed bluefin tuna market is projected to grow due to rising global demand for premium sushi and sashimi, increasingly strict international quotas on wild bluefin tuna fishing, growing consumer preference for sustainably and responsibly sourced seafood, continued advances in closed-cycle breeding and feed technology, and expanding export opportunities in emerging luxury food markets across the Middle East, Southeast Asia, and Latin America.

According to a study, the global farmed bluefin tuna market size was worth around USD 1.38 billion in 2024 and is predicted to grow to around USD 2.84 billion by 2034.

The CAGR value of the farmed bluefin tuna market is expected to be around 8.28% during 2025–2034.

Asia Pacific is expected to lead the global farmed bluefin tuna market during the forecast period, driven primarily by Japan's dominant role as both the world's leading producer and largest consumer of farmed bluefin tuna.

The major players in the global farmed bluefin tuna market include Maruha Nichiro Corporation, Kinki University Aquaculture Research Institute, Clean Seas Seafood, Futami Fish Farm, Azzurra Tuna Farm, Ricardo Fuentes and Sons Group, Umami Sustainable Seafood, Kali Tuna, and Grupo Nueva Pescanova.

The report examines key aspects of the farmed bluefin tuna market, including a detailed analysis of current growth drivers and restraints, emerging opportunities, significant challenges facing producers and distributors, a competitive landscape analysis, regional market breakdowns, and a future outlook across all major product types, farming methods, applications, and geographies.

The farmed bluefin tuna market value chain includes juvenile fish production or capture, grow-out farming operations, fish harvesting and processing, quality grading and cold chain logistics, wholesale distribution, and final sale to restaurants, retailers, specialty fish markets, and individual consumers, with sustainability certification and traceability systems increasingly important at every stage of the chain.

The farmed bluefin tuna market is shifting toward fully closed-cycle farming methods that do not rely on wild juvenile fish, driven by rising sustainability demands from premium buyers, growing interest in land-based aquaculture systems that can produce high-quality fish anywhere in the world, and increasing consumer willingness to pay a premium for traceable, responsibly produced bluefin tuna.

The farmed bluefin tuna market is driven by growing sushi demand, stricter fishing limits, rising focus on sustainability, increasing incomes in emerging markets, and advances in aquaculture technology.

HappyClients