Chemical Substance Packaging Market Size, Share, Forecast 2034

Chemical Substance Packaging Market By Material Type (Plastics, Metal, Paper & Paperboard, Glass, and Others), By Packaging Type (Bottles and Jars, Intermediate Bulk Containers, Drums, and Others), By End-User Industry (Agrochemicals, Pharmaceuticals, Manufacturing, and Others), By Chemical Formulation (Gaseous Chemicals, Powdered Chemicals, Liquid Chemicals, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 18.24 Billion | USD 26.30 Billion | 4.15% | 2024 |

Chemical Substance Packaging Industry Perspective:

What will be the size of the global ,market during the forecast period?

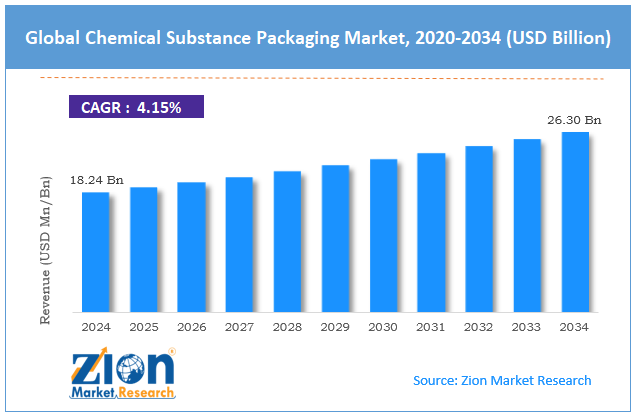

The global chemical substance packaging market size was worth around USD 18.24 billion in 2024 and is predicted to grow to around USD 26.30 billion by 2034 with a compound annual growth rate (CAGR) of roughly 4.15% between 2025 and 2034.

Key Insights:

- As per the analysis shared by our research analyst, the global chemical substance packaging market is estimated to grow annually at a CAGR of around 4.15% over the forecast period (2025-2034)

- In terms of revenue, the global chemical substance packaging market size was valued at around USD 18.24 billion in 2024 and is projected to reach USD 26.30 billion by 2034.

- The chemical substance packaging market is projected to grow at a significant rate due to the rising chemical production rate across the globe.

- Based on the material type, the plastics segment is growing at a high rate and will continue to dominate the global market, as per industry projections

- Based on the packaging type, the drums segment is anticipated to command the largest market share

- Based on the end-user industry, the manufacturing segment is anticipated to lead the market growth trends

- Based on the chemical formulation, the liquid chemicals segment is anticipated to influence revenue in the market

- Based on region, North America is projected to dominate the global market during the forecast period

Chemical Substance Packaging Market: Overview

Chemical substance packaging refers to the different types of solutions used for storing, transporting, and distributing chemical substances. The packaging of chemical materials plays a crucial role and hence differs significantly from regular packaging. According to industry research, packaging for chemical substances is designed to manage the highly hazardous properties of industrial chemicals. The most common type of chemical substance packaging includes drums, intermediate bulk containers (IBCs), jerrycans, bottles & jars, cans, and pails. In recent times, demand for flexible chemical packaging solutions has increased across the globe.

During the forecast period, the chemical substance packaging industry is projected to experience increased revenue, driven by the growing production of novel chemicals, heightened environmental protection efforts, and regulatory pressures. Additionally, innovative and robust packaging designs may open new avenues for extended growth in the coming years. A major drawback of the chemical substance packaging market is the high cost of specialized designs and the risk of supply chain disruptions.

Chemical Substance Packaging Market: Dynmics

Growth Drivers

How will the increase in chemical production influence revenue in the chemical substance packaging market?

The global chemical substance packaging market is projected to benefit from the rising chemical production rate across the globe. Asia-Pacific is one of the world’s largest contributors to the global chemical industry, accounting for more than 61% of total chemical production. Some of the leading factors driving demand for novel chemicals are urbanization, industrialization, and increased use in end-user industries. In February 2026, Arlanxeo, a global provider of performance elastomers, announced the launch of its new Therban hydrogenated nitrile butadiene rubber (HNBR) plant in Changzhou, China. The move has strengthened the company’s hold as a supplier of high-performance elastomers across Asia-Pacific.

According to official estimates, the Asia-Pacific hosts more than 1650 petrochemical facilities with several newly announced projects to start in the coming year. Similar trends are witnessed in other parts of the world. Packaging of chemical substances is essential not only for their long-term storage but also to ensure environmental safety, particularly when handling hazardous materials.

Government and regulatory pressure surrounding the chemical industry influences market revenue

The global chemical sector is heavily regulated and requires strict compliance with regulations governing the storage and transport of hazardous chemicals. These regulatory pressures directly impact demand for innovative chemical packaging items such as drums and IBCs. For instance, in February 2026, reports emerged suggesting that Estee Lauder Companies was fined USD 750,000 for violations of environmental laws in Canada.

Similarly, in a recent event, the Indian government launched new safety protocols for handling chemicals such as toluene, benzene, and xylene. Such strict procedures will subsequently impact demand in the global chemical substance packaging market.

Restraints

Why will the high cost of specialized packaging limit the growth of the chemical substance packaging market?

The global industry for chemical substance packaging is projected to be restricted by the high cost of specialized solutions. According to industry research, the cost of certified and pressure-related cylinders is exceptionally high since they are built using specialized materials and precision manufacturing procedures. Furthermore, the evolving certification landscape has created additional compliance-related growth barriers for the market players.

Opportunities

Ongoing advancements in packaging solutions offer renewed growth opportunities

The global chemical substance packaging market is anticipated to generate growth opportunities due to the rising advancements in packaging solutions. These innovations are driven by evolving regulatory compliance requirements, increased demand for eco-friendly packaging, and changing needs of end-users. In January 2026, INEOS Olefins & Polymers Europe announced the launch of a new Recycl-IN hybrid polymer. It contains 70% recycled material and intends to offer contact-sensitive cosmetics packaging solutions.

In February 2026, the UK government announced the launch of new plans to manage per- and polyfluoroalkyl substances (PFAS). Government officials also addressed potential food and water contamination and human dietary exposure to the chemicals. PFAS are used in food packaging along with other applications. In January 2026, Sun Chemical announced the launch of a new ultra-low monomer (ULM) solvent-free adhesive. The novel SunLam QA-8000 + HA450 adhesive is expected to assist packaging converters in moving away from solvent-based systems without compromising performance standards.

Challenges

Why will raw material volatility and supply chain disruptions challenge the chemical substance packaging market expansion?

The global chemical substance packaging industry is expected to be challenged by volatility in raw materials, particularly resins and plastics. The ongoing social-political conflict and evolving world order may impact market revenue in the long run. Furthermore, the risk of supply chain disruptions is expected to remain a prominent growth inhibitor in the coming years.

Chemical Substance Packaging Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Chemical Substance Packaging Market |

| Market Size in 2024 | USD 18.24 Billion |

| Market Forecast in 2034 | USD 26.30 Bllion |

| Growth Rate | CAGR of 4.15% |

| Number of Pages | 222 |

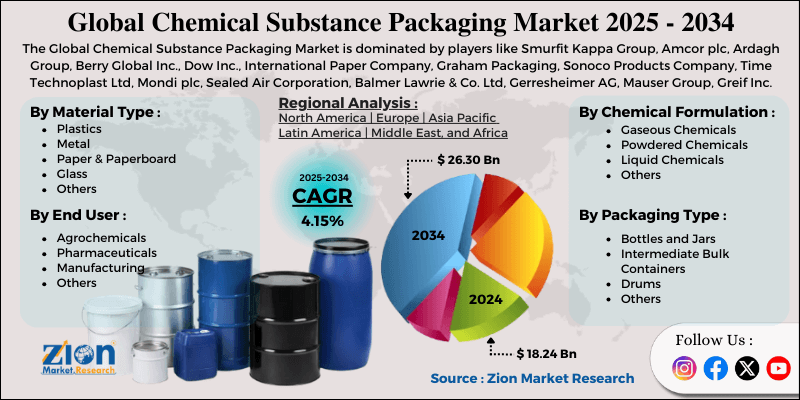

| Key Companies Covered | Smurfit Kappa Group, Amcor plc, Ardagh Group, Berry Global Inc., Dow Inc., International Paper Company, Graham Packaging, Sonoco Products Company, Time Technoplast Ltd, Mondi plc, Sealed Air Corporation, Balmer Lawrie & Co. Ltd, Gerresheimer AG, Mauser Group, Greif Inc., and others. |

| Segments Covered | By Material Type, By Packaging Type, By End-User Industry, By Chemical Formulation, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Chemical Substance Packaging Market: Segmentation

The global chemical substance packaging market is segmented based on material type, packaging type, end-user industry, chemical formulation, and region.

Why will plastic continue to dominate the chemical substance packaging market during the forecast period?

Based on material type, the global market segments are plastics, metal, paper & paperboard, glass, and others. In 2024, around 49.01% of global revenue was listed in the plastics segment, and it is projected to deliver a CAGR of 4.5% over the coming years. Plastic-based chemical packaging items offer superior performance and flexibility in handling different types of chemicals. These factors help the segment dominate its counterparts.

Which factors will help drums lead the segmental revenue in the coming years?

Based on packaging type, the global chemical substance packaging industry is divided into bottles and jars, intermediate bulk containers, drums, and others. As per industry research, drums accounted for 41% of the total revenue. The segment is projected to achieve a CAGR of 3.57% over the forecast period, driven by the standardized use of drums for handling large volumes of chemicals.

What is the market projection for the manufacturing segment over the projection period?

Based on end-user industry, the global market divisions are agrochemicals, pharmaceuticals, manufacturing, and others. Around 45.06% of the market share was led by the manufacturing segment in 2024 and will grow at a CAGR of 3.75% during the projection period. Chemical manufacturing has witnessed unprecedented growth in the past few years, driven by increased applications across end-user industries such as semiconductor fabrication, food & beverages, and other sectors.

What is the expected CAGR for liquid chemicals in the chemical substance packaging industry during the forecast period?

Based on chemical formulation, the global market divisions are gaseous chemicals, powdered chemicals, liquid chemicals, and others. In 2024, around 45.07% of total revenue was listed in the liquid chemicals segment. It is projected to deliver a 4.1% CAGR over the projection period, driven by the increasing use of liquid storage and transportation for most chemicals, particularly acids and surfactants.

Chemical Substance Packaging Market: Regional Analysis

Which factors are driving revenue in the North American chemical substance packaging market?

The global chemical substance packaging market is projected to be led by North America during the projection period. In 2024, the region accounted for 32.09% of global revenue and is expected to grow at a CAGR of 4.02% during the projection period. Countries such as the US and Canada have a well-established and growing chemical industry, resulting in high demand for effective packaging solutions. Additionally, strict government regulations, ongoing product innovation, and the presence of numerous players further contribute to the market's sustained growth.

What is the projected CAGR for Asia-Pacific during the forecast duration?

Asia-Pacific is anticipated to emerge as the fastest-growing market with a CAGR of 5.91% in the coming years. Countries such as China and India will lead regional revenue due to the presence of a robust chemical manufacturing industry. Additionally, growing manufacturers of new-age chemical packaging solutions, including novel raw materials and production techniques, will further aid regional expansion. The accelerated growth reported across end-user verticals such as pharmaceuticals, infrastructure development projects, and the construction industry will further aid improved revenue across the Asia-Pacific.

Chemical Substance Packaging Market: Competitive Analysis

The global chemical substance packaging market is led by players like:

- Smurfit Kappa Group

- Amcor plc

- Ardagh Group

- Berry Global Inc.

- Dow Inc.

- International Paper Company

- Graham Packaging

- Sonoco Products Company

- Time Technoplast Ltd

- Mondi plc

- Sealed Air Corporation

- Balmer Lawrie & Co. Ltd

- Gerresheimer AG

- Mauser Group

- Greif Inc.

What are the prominent trends in the chemical substance packaging industry?

Eco-friendly materials

The chemical packaging industry is experiencing increased demand for eco-friendly materials, such as biodegradable packaging and recycled plastics. These materials will help meet regulatory guidelines and pressures.

Smart packaging solutions

The rising use of advanced connectivity-enhancing technologies such as Quick Response (QR) codes and blockchain integration will further help the industry thrive during the projection period. These technologies are expected to help improve supply chain results in the chemical industry.

The global chemical substance packaging market is segmented as follows:

By Material Type

- Plastics

- Metal

- Paper & Paperboard

- Glass

- Others

By Packaging Type

- Bottles and Jars

- Intermediate Bulk Containers

- Drums

- Others

By End-User Industry

- Agrochemicals

- Pharmaceuticals

- Manufacturing

- Others

By Chemical Formulation

- Gaseous Chemicals

- Powdered Chemicals

- Liquid Chemicals

- Others

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

List of Contents

Chemical Substance PackagingIndustry Perspective:Key Insights:OverviewDynmicsReport ScopeSegmentationRegional AnalysisCompetitive AnalysisWhat are the prominent trends in the chemical substance packaging industry?The global chemical substance packaging market is segmented as follows:HappyClients