Atherectomy Devices Market Size, Share, Trends, Growth and Forecast 2034

Atherectomy Devices Market By Product (Directional Atherectomy Devices, Rotational Atherectomy Devices, Orbital Atherectomy Devices, Laser Atherectomy Devices), By Application (Peripheral Artery Disease [PAD] Treatment Devices, Coronary Artery Disease [CAD] Intervention Devices, Carotid Artery Disease Intervention Devices, Renal Artery Disease Intervention Devices, Aortic Atherosclerosis Intervention Devices), By End-User (Hospitals, Specialty Clinics, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 1,040.37 Million | USD 1,939.96 Million | 8.10% | 2024 |

Atherectomy Devices Industry Perspective:

What will be the size of the global atherectomy devices market during the forecast period?

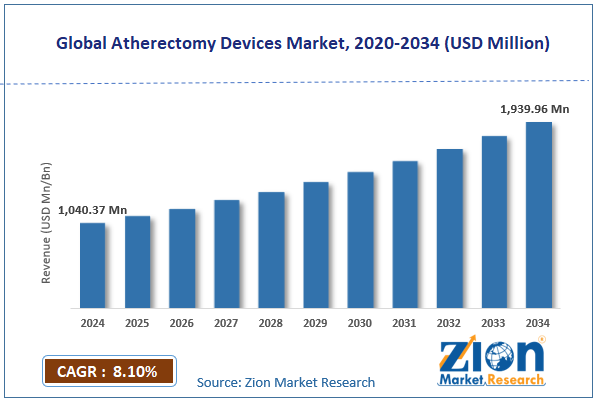

The global atherectomy devices market size was approximately USD 1040.37 million in 2024 and is projected to reach USD 1939.96 million by 2034, with a compound annual growth rate (CAGR) of approximately 8.10% between 2025 and 2034.

Key Insights:

- As per the analysis shared by our research analyst, the global atherectomy devices market is estimated to grow annually at a CAGR of around 8.10% over the forecast period (2025-2034)

- In terms of revenue, the global atherectomy devices market size was valued at around USD 1040.37 million in 2024 and is projected to reach USD 1939.96 million by 2034.

- The atherectomy devices market is projected to grow significantly, driven by the growing geriatric population worldwide, technological advancements in atherectomy systems, and rising healthcare expenditure in emerging economies.

- Based on product, the directional atherectomy devices segment is expected to lead the market, while the rotational atherectomy devices segment is expected to grow considerably.

- Based on application, the Peripheral Artery Disease (PAD) treatment devices segment is the dominating segment. In contrast, the Coronary Artery Disease (CAD) intervention devices segment is projected to witness sizeable revenue over the forecast period.

- Based on end-user, the hospitals segment is expected to lead the market, followed by the specialty clinics segment.

- By region, North America is projected to dominate the global market during the forecast period, followed by Europe.

Atherectomy Devices Market: Overview

Atherectomy devices are non-invasive, catheter-based tools used to remove atherosclerotic plaque from blocked or narrowed arteries, commonly in patients with coronary or peripheral artery disease. These devices, like orbital, laser, rotational, or directional atherectomy systems, physically sand, cut, or vaporize plaque to restore blood flow and enhance vessel patency. The global atherectomy devices market is likely to expand rapidly, driven by rising cardiovascular disease cases, advances in device design, and the growing preference for minimally invasive procedures. The worldwide cases of coronary and peripheral artery disease are growing because of an aging population and lifestyle risk factors. This rise increases demand for effective interventional treatments. Atherectomy devices offer a viable option to manage complex arterial blockages.

Moreover, continual advancement in device efficiency, safety, and navigability improves procedural outcomes. Newer atherectomy systems lower thermal injury and embolization risk. These improvements fuel clinical preference and industry adoption. Furthermore, minimally invasive interventions generally offer shorter stays, faster recovery, and reduced pain. Atherectomy is preferred over open surgery for several patients. Patient and provider preferences drive the market.

Nevertheless, the global market faces limitations, including the risk of procedure-related complications and limited reimbursement in some markets. Potential complications like perforation, dissection, or distal embolization exist. These risks make some clinicians cautious about the broader use. Safety concerns may also slow adoption and device preference. In regions lacking supportive reimbursement policies, patient out-of-pocket expenses remain high. This financial barrier discourages non-urgent or elective procedures. Limited coverage limits market penetration. Still, the global atherectomy devices industry benefits from several favorable factors, such as product innovation for complex lesion management, integration with imaging and digital technologies, and strategic collaborations and alliances.

Development of devices optimized for chronic or calcified total occlusions offers differentiation. Improving safety features and simplified use may appeal to clinician preference, creating a competitive advantage. Combining atherectomy systems with robotics, AI guidance, and real-time imaging improves precision. Improved procedural visualization can reduce complication rates. Technology integration offers a premium product segment. Alliances among device manufacturers, research institutions, and healthcare providers can boost adoption. Collaborative training programs raise clinician competency. Associations also support industry entry in regulated regions.

Atherectomy Devices Market: Dynamics

Growth Drivers

How does the atherectomy devices market benefit from integration with adjunct therapies such as drug-coated balloons?

Atherectomy is increasingly used in combination with adjunct therapies such as specialty stents and drug-coated balloons. Pre-treatment plaque modification can reduce restenosis more than standalone therapy and enhance drug uptake. Hybrid clinical protocols are growing for complex and recurrent lesions to enhance long-term outcomes. Interventional specialists are adopting integrative strategies as evidence accumulates in favor of combination approaches. This expands the clinical role of atherectomy beyond basic plaque removal. Such integration further stimulates demand for he said devices, impacting the atherectomy devices market.

How do technological improvements and product innovation drive the atherectomy devices market growth?

Device manufacturers are launching advanced atherectomy platforms with enhanced safety, precision, and versatility. Newer systems comprise improved imaging integration and navigation tools to support complex interventions. Enhancements in orbital, rotational, and laser technologies facilitate the treatment of a broader range of lesion types. Sensor-guided technologies and robotics are beginning to improve operator control and procedural outcomes. Ergonomic designs and miniaturization also increase clinical applicability. These advancements are appealing to more clinicians, encouraging them to adopt atherectomy solutions.

Restraints

High device and procedure costs unfavorably impact the market progress

Atherectomy systems and disposables are more expensive than simpler treatments like balloon angioplasty. Significant capital expenditure for advanced platforms restricts investment by smaller hospitals. Patients without strong insurance coverage may face major out-of-pocket costs. Higher procedural expenses hamper broader adoption in price-sensitive regions. Budget limitations in the developing market further limit uptake. Cost concerns remain a key barrier to wider adoption worldwide.

Opportunities

How do hybrid treatment approaches create promising avenues for the growth of the atherectomy devices industry?

Combining atherectomy with drug-coated balloons, biologic therapies, or stents can enhance long-term outcomes, such as vessel patency. Clinical protocols integrating multiple technologies are gaining prominence. This increases the role of atherectomy beyond standalone plaque removal. Favorable outcomes may impact guideline recommendations. Payers could be more willing to support bundled procedures with proven benefits. Hybrid approaches create fresh clinical demand, thus positively impacting the growth of the atherectomy devices industry.

Challenges

Incomplete clinical evidence in certain populations limits the market growth

While atherectomy is effective in the majority of conditions, evidence remains limited in certain subgroups, such as heavily calcified distal lesions or small vessels. The lack of consistent long-term outcome data makes it challenging for some clinicians to commit completely. Generating more high-class evidence takes time and resources. Some payers may need stronger evidence for wide coverage. This uncertainty can slow guidance acceptance. Evidence gaps remain a challenge to wider adoption.

Atherectomy Devices Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Atherectomy Devices Market |

| Market Size in 2024 | USD 1,040.37 Million |

| Market Forecast in 2034 | USD 1,939.96 Mllion |

| Growth Rate | CAGR of 8.10% |

| Number of Pages | 224 |

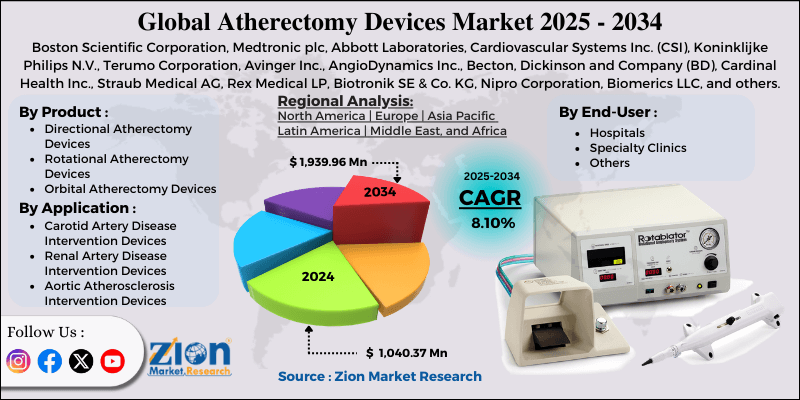

| Key Companies Covered | Boston Scientific Corporation, Medtronic plc, Abbott Laboratories, Cardiovascular Systems Inc. (CSI), Koninklijke Philips N.V., Terumo Corporation, Avinger Inc., AngioDynamics Inc., Becton, Dickinson and Company (BD), Cardinal Health Inc., Straub Medical AG, Rex Medical LP, Biotronik SE & Co. KG, Nipro Corporation, Biomerics LLC, and others. |

| Segments Covered | By Product, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Atherectomy Devices Market: Segmentation

The global atherectomy devices market is segmented by product, application, end-user, and region.

Why is the Directional Atherectomy Devices segment projected to dominate the atherectomy devices market?

Based on product, the global atherectomy devices industry is divided into directional atherectomy devices, rotational atherectomy devices, orbital atherectomy devices, and laser atherectomy devices. The directional atherectomy devices segment registers 42% of the total market. This share is backed by their wide clinical applicability, strong clinical adoption in coronary and peripheral interventions, and versatility in treating various lesion types.

Conversely, the rotational atherectomy devices segment ranks second with over 30% market share. This growth is driven by proven effectiveness and longstanding clinical use, mainly in modifying heavily calcified arterial lesions, where they are a foundation in several interventional cardiology procedures.

What factors help the Peripheral Artery Disease (PAD) Treatment Devices segment lead the atherectomy devices market?

Based on application, the global atherectomy devices market is segmented into Peripheral Artery Disease (PAD) treatment devices, Coronary Artery Disease (CAD) intervention devices, carotid artery disease intervention devices, renal artery disease intervention devices, and aortic atherosclerosis intervention devices. The peripheral artery disease (PAD) treatment devices segment captures a dominating 58% share of the market. This is due to high worldwide incidences of PAD, especially in diabetic and aging populations, and the surging preference for minimally invasive vascular interventions.

However, the coronary artery disease (CAD) intervention devices segment holds the second-largest share, at 35% of the market, as atherectomy is a crucial adjunctive therapy for calcified and complex coronary lesions, supported by expanding interventional procedures and clinical evidence of enhanced outcomes.

What are the key reasons for the leadership of the Hospitals segment in the atherectomy devices market?

Based on end-user, the global market is segmented into hospitals, specialty clinics, and others. The hospitals segment dominates with 65% of the total market, as they house multidisciplinary teams and advanced catheterization labs vital for complex coronary and peripheral procedures, and they receive the bulk of procedural volumes and reimbursement support.

Nonetheless, the specialty clinics segment ranks second with 30% market share. This is fueled by the inclination toward minimally invasive care, low operating costs, and outpatient settings, which make atherectomy procedures increasingly viable outside traditional hospital settings.

Atherectomy Devices Market: Regional Analysis

What gives North America a competitive edge in the global Atherectomy Devices Market?

North America is projected to maintain its dominant position in the global Atherectomy Devices market, with a 6-7% CAGR, owing to high disease prevalence, advanced healthcare infrastructure, and favorable reimbursement and clinical adoption. North America holds a high prevalence of peripheral artery and cardiovascular diseases because of aging populations, sedentary lifestyles, and diabetes. This creates a large patient pool, thereby augmenting demand for advanced interventions such as atherectomy devices. Well-equipped catheterization labs and hospitals, along with expert interventional specialists, support broader use of innovative devices. Regional healthcare systems enable complex procedures with high success rates, driving device adoption.

Furthermore, supportive insurance coverage lowers patient cost pressure, motivating more procedures. Strong clinician evidence and early adoption of novel solutions promote consistent use of atherectomy in treating complex vascular lesions.

Why does Europe rank second in the global Atherectomy Devices Market?

Europe maintains its position as the second-largest region, with a 6.8% CAGR in the global Atherectomy Devices industry, driven by strong healthcare infrastructure, high pressure of vascular diseases, and favorable reimbursement and clinical guidelines. Europe holds well-established vascular centers and hospitals equipped with advanced catheter labs. This infrastructure supports a wider range of minimally invasive procedures, comprising atherectomy. Ready access to specialized equipment allows high procedural volumes in major regions.

Moreover, the region witnesses a large number of cases of peripheral artery and cardiovascular diseases because of lifestyle risks and aging populations. This fuels demand for interventional therapies. Atherectomy devices are increasingly used to efficiently manage calcified and complex lesions. Additionally, several European nations have established reimbursement pathways and supportive policies for endovascular procedures. These financial architectures reduce cost barriers for providers and patients. Combined with guideline inclusion and clinician familiarity, this drives device utilization and adoption.

Atherectomy Devices Market: Competitive Analysis

The leading players in the global atherectomy devices market are:

- Boston Scientific Corporation

- Medtronic plc

- Abbott Laboratories

- Cardiovascular Systems Inc. (CSI)

- Koninklijke Philips N.V.

- Terumo Corporation

- Avinger Inc.

- AngioDynamics Inc.

- Becton

- Dickinson and Company (BD)

- Cardinal Health Inc.

- Straub Medical AG

- Rex Medical LP

- Biotronik SE & Co. KG

- Nipro Corporation

- Biomerics LLC

What are the key trends in the global Atherectomy Devices Market?

Growth of ambulatory and minimally invasive procedures:

There is a growing shift toward minimally invasive vascular interventions performed in ambulatory or outpatient settings. Atherectomy devices that support shorter procedure times and quick recoveries are in higher demand. This trend reduces hospital stays and overall treatment costs.

Emphasis on evidence‑based adoption and guideline support:

Clinicians are more dependent on strong clinical data demonstrating safety and efficacy for complex lesions. Growing inclusion of atherectomy in treatment guidelines fuels procedural uptake. Strong evidence strengthens physician confidence and augments adoption in specialties.

The global atherectomy devices market is segmented as follows:

By Product

- Directional Atherectomy Devices

- Rotational Atherectomy Devices

- Orbital Atherectomy Devices

- Laser Atherectomy Devices

By Application

- Peripheral Artery Disease (PAD) Treatment Devices

- Coronary Artery Disease (CAD) Intervention Devices

- Carotid Artery Disease Intervention Devices

- Renal Artery Disease Intervention Devices

- Aortic Atherosclerosis Intervention Devices

By End-User

- Hospitals

- Specialty Clinics

- Others

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

HappyClients