Advanced Materials for Electronics Market Size, Share, Trends, Growth and Forecast 2034

Advanced Materials for Electronics Market By Type (Graphene Material, Silicon Carbide Material, Ceramic Material, Smart Glass Material, and Others), By Application (Photovoltaic Cells, Displays, Touch Screens, Sensors, Semiconductors, Wearable Electronics Devices, Biomedical Devices, and Others). and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 35.01 Billion | USD 71.5 Billion | 7.4% | 2024 |

Advanced Materials for Electronics Industry Perspective:

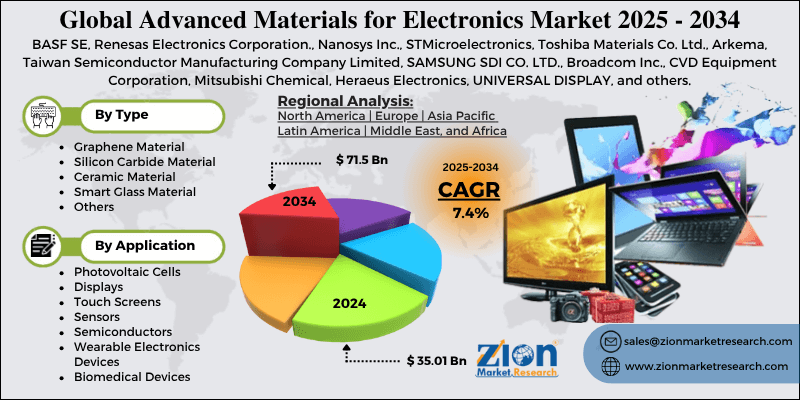

The global advanced materials for electronics market size was worth around USD 35.01 billion in 2024 and is predicted to grow to around USD 71.5 billion by 2034, with a compound annual growth rate (CAGR) of roughly 7.4% between 2025 and 2034.

Advanced Materials for Electronics Market: Overview

The term "advanced materials for electronics" refers to specially designed materials with better qualities, such as mechanical strength, chemical resistance, thermal stability, or electrical conductivity, that are utilized to create and improve electronic systems and gadgets. These materials are made at the molecular or atomic level to enable or enhance functionality, efficiency, performance, and miniaturization in electronic applications.

Key Insights

- As per the analysis shared by our research analyst, the global advanced materials for electronics market is estimated to grow annually at a CAGR of around 7.4% over the forecast period (2025-2034).

- In terms of revenue, the global advanced materials for electronics market size was valued at around USD 35.01 billion in 2024 and is projected to reach USD 71.5 billion by 2034.

- The increasing penetration of EVs across the globe is expected to drive the advanced materials for electronics market over the forecast period.

- Based on the type, the silicon carbide segment is expected to hold the largest market share over the forecast period.

- Based on the application, the semiconductors segment is expected to dominate the market expansion over the projected period.

- Based on region, Europe is expected to dominate the market during the forecast period.

Advanced Materials for Electronics Market: Growth Drivers

Expansion of Electric Vehicles (EVs) and renewable energy drives market growth

Advanced materials for the electronics sector are primarily driven by the growth of renewable energy sources and the increasing adoption of electric vehicles (EVs). The need for materials providing better performance, efficiency, and sustainability in next-generation technology drives this expansion.

Materials that can improve power efficiency, temperature control, and downsizing are sorely needed as transportation becomes more electric. Two basic components, wide-bandgap semiconductors with enhanced energy efficiency and low heat-generating capability for high-voltage power electronics in electric vehicles, are silicon carbide (SiC) and gallium nitride (GaN).

Moreover, the integration of renewable energy sources depends on advanced materials for effective energy conversion and storage. Examining perovskite and graphene will help to increase solar panel efficiency and affordability.

Moreover, better materials are necessary for the development of batteries and other storage devices that can endure the intermittent nature of renewable energy. Thus, the aforementioned stats influence the industry expansion.

Advanced Materials for Electronics Market: Restraints

High production and R&D costs hinder market growth

The advanced materials for electronics market is anticipated to grow considerably, despite potential obstacles from high production and research and development (R&D) costs. Graphene, nanomaterials, and high-performance alloys are examples of advanced materials that sometimes need complex and specialized manufacturing techniques.

High-strength carbon fiber, for instance, may be produced for over $10 per pound, which keeps it from being widely employed in sectors where cost is an issue.

Furthermore, developing new advanced materials necessitates a significant investment in staff, specialized tools, and research. Patent disputes and issues with intellectual property protection are the main causes of the 8% annual increase in R&D spending in materials science. Therefore, high production and R&D costs hinder the sector’s expansion.

Advanced Materials for Electronics Market: Opportunities

Growing expansion of advanced material business by the key player offers a lucrative opportunity for market growth

The rising expansion of the advanced material business by the key players is expected to offer a lucrative opportunity for the advanced materials for electronics market expansion over the analysis period.

For instance, in October 2024, Honeywell sought to have its Advanced Materials division split off as a separate, publicly traded company in the United States by the end of 2025 or the start of 2026.

Honeywell expects to provide its owners with a tax-free spin-off. Considering its status as a leading worldwide supplier of specialty chemicals and materials with a sustainability focus, this pure-play company will be well-positioned to benefit from an enhanced strategic focus and the financial flexibility to pursue innovation and growth possibilities through investment cycles.

Through the expected spin-off, Honeywell will also be able to advance its strategic targets of simplifying its portfolio, developing its Accelerator operating system, and accelerating organic growth.

Advanced Materials for Electronics Market: Challenges

Lack of skilled workforce poses a major challenge to market expansion

Due to technological breakthroughs in semiconductors, electric vehicles (EVs), and renewable energy systems, the advanced materials for electronics industry is expanding significantly. However, a significant obstacle impeding this advancement is the scarcity of a trained labor force.

The skills taught in academics and those required in the electronics sector are quite different. Professionals in specialized disciplines like semiconductor design, advanced packaging, and chip fabrication are in short supply as a result of many college programs failing to keep up with the rapid improvements in technology.

Advanced Materials for Electronics Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Advanced Materials for Electronics Market |

| Market Size in 2024 | USD 35.01 Billion |

| Market Forecast in 2034 | USD 71.5 Billion |

| Growth Rate | CAGR of 7.4% |

| Number of Pages | 211 |

| Key Companies Covered | BASF SE, Renesas Electronics Corporation., Nanosys Inc., STMicroelectronics, Toshiba Materials Co. Ltd., Arkema, Taiwan Semiconductor Manufacturing Company Limited, SAMSUNG SDI CO. LTD., Broadcom Inc., CVD Equipment Corporation, Mitsubishi Chemical, Heraeus Electronics, UNIVERSAL DISPLAY, and others. |

| Segments Covered | By Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Advanced Materials for Electronics Market: Segmentation

The global advanced materials for electronics industry are segmented based on type, application, and region.

Based on the type, the global market is bifurcated into graphene material, silicon carbide material, ceramic material, smart glass material, and others. The silicon carbide material segment is expected to hold the largest market share over the forecast period. SiC's exceptional qualities, which make it perfect for high-power and high-frequency applications, such as its high thermal conductivity, high electric field breakdown strength, and temperature resistance, are what propel its dominance.

SiC's vital function in power electronics, especially in electric cars and renewable energy systems, where its effectiveness and performance are highly prized, is driving the market's expansion. Its market position is further strengthened by developments in SiC technology and its growing application in cutting-edge fields.

Based on the application, the global advanced materials for electronics industry are bifurcated into photovoltaic cells, displays, touch screens, sensors, semiconductors, wearable electronics devices, biomedical devices, and others. The semiconductors segment is expected to dominate the market over the projected period.

Excellent thermal performance and efficiency of materials like silicon carbide (SiC) and gallium nitride (GaN) drive power electronics to employ them more and more. High-frequency gadgets, renewable energy systems, and electric vehicles (EVs) depend on these components.

Moreover, the explosion of wearables, smartphones, tablets, and Internet of Things devices highlights the necessity of innovative semiconductor materials with improved performance and energy economy. Laws such as the U.S. CHIPS Act and other initiatives in Asia and Europe are also significantly funding semiconductor R&D and manufacturing, hence driving demand for innovative materials.

Advanced Materials For Electronics Market: Regional Analysis

Europe dominates the market over the projected period

Europe is expected to dominate the global advanced materials for electronics market. The regional expansion of the market is owing to the growing automotive electrification.

The automobile industry's demand for specialized semiconductor materials is increasing rapidly due to the shift to electric vehicles (EVs) and the integration of advanced driver assistance systems (ADAS).

Furthermore, the demand for cutting-edge materials that improve performance and energy efficiency is being driven by the widespread use of smartphones, tablets, wearable technology, and smart home appliances.

Additionally, the European Chips Act aims to raise more than €43 billion to enhance the semiconductor industry by promoting domestic manufacturing and reducing reliance on foreign suppliers.

On the other hand, the Asia Pacific is expected to grow at the highest CAGR during the projected period. China, Taiwan, South Korea, and Japan are among the key semiconductor manufacturing hubs in Asia Pacific.

The demand for sophisticated materials used in chip manufacture and packaging is driven by the region's dominance in semiconductor fabrication.

Additionally, regional governments are putting laws and incentive schemes into place to encourage domestic electronics research and production. India's $10 billion incentive package, for instance, intends to improve its semiconductor industry.

Advanced Materials for Electronics Market: Competitive Analysis

The global advanced materials for electronics market is dominated by players like:

- BASF SE

- Renesas Electronics Corporation.

- Nanosys Inc.

- STMicroelectronics

- Toshiba Materials Co. Ltd.

- Arkema

- Taiwan Semiconductor Manufacturing Company Limited

- SAMSUNG SDI CO. LTD.

- Broadcom Inc.

- CVD Equipment Corporation

- Mitsubishi Chemical

- Heraeus Electronics

- UNIVERSAL DISPLAY

The global advanced materials for electronics market are segmented as follows:

By Type

- Graphene Material

- Silicon Carbide Material

- Ceramic Material

- Smart Glass Material

- Others

By Application

- Photovoltaic Cells

- Displays

- Touch Screens

- Sensors

- Semiconductors

- Wearable Electronics Devices

- Biomedical Devices

- Others

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

The term "advanced materials for electronics" refers to specially designed materials with better qualities, such as mechanical strength, chemical resistance, thermal stability, or electrical conductivity, that are utilized to create and improve electronic systems and gadgets.

The advanced materials for electronics market is majorly influenced by several variables such as renewable energy expansion, growing adoption of EVs across the globe, and the emergence of advanced technology such as AI, IoT, and 5G.

According to the report, the global advanced materials for electronics market size was worth around USD 35.01 billion in 2024 and is predicted to grow to around USD 71.5 billion by 2034.

The global advanced materials for electronics market is expected to grow at a CAGR of 7.4% during the forecast period.

The global advanced materials for electronics market growth is expected to be driven by Europe. It is currently the world’s highest revenue-generating market due to the rising adoption of EVs and the proliferation of smartphones.

The global advanced materials for electronics market is dominated by players like BASF SE, Renesas Electronics Corporation., Nanosys Inc., STMicroelectronics, Toshiba Materials Co., Ltd., Arkema, Taiwan Semiconductor Manufacturing Company Limited, SAMSUNG SDI CO., LTD., Broadcom Inc., CVD Equipment Corporation, Mitsubishi Chemical, Heraeus Electronics, and UNIVERSAL DISPLAY, among others.

The market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients