Personalised Medicine Market Size, Share & Forecast 2026–2034

15-May-2026 | Zion Market Research

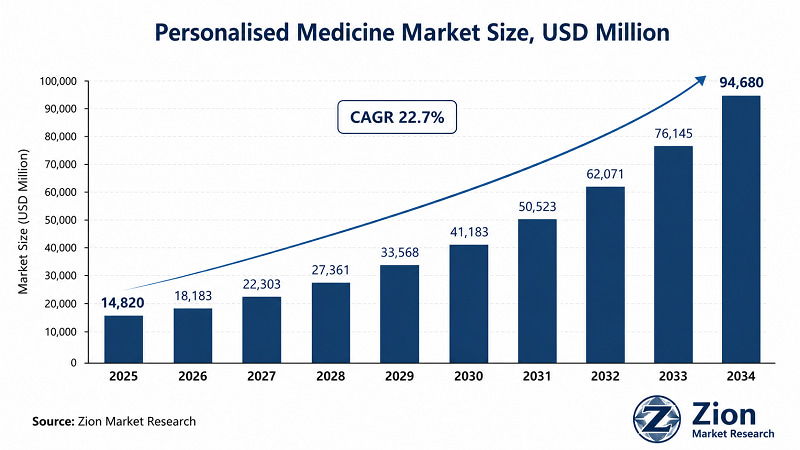

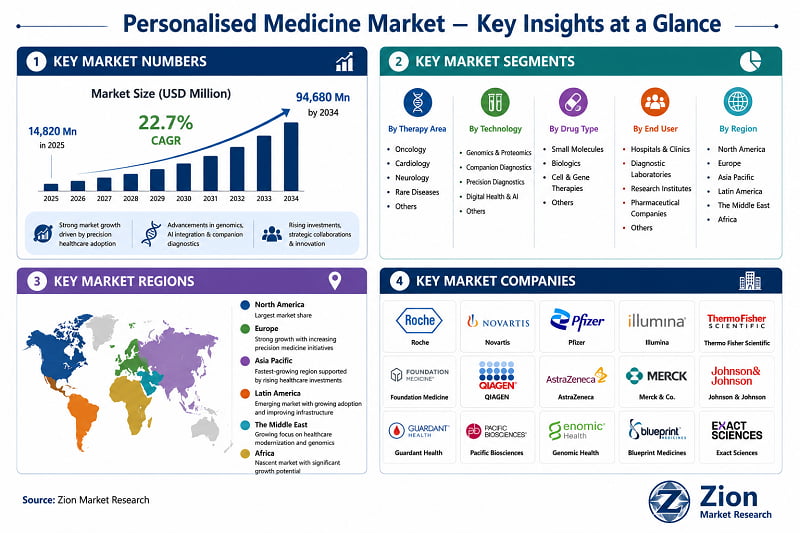

The Global Personalised Medicine market was valued at USD 14,820 Mn in 2025. It is projected to reach USD 94,680 Mn by 2034, registering a 22.7% CAGR during 2026–2034. North America leads with the highest revenue share, while Asia Pacific registers the fastest growth. Genomics, companion diagnostics, and AI-driven precision platforms are the primary demand catalysts.

Key Insights Snapshot

|

Key Insights Snapshot — Personalised Medicine Market |

|

|

Report Title |

Global Personalised Medicine Market by Therapy Area (Oncology, Cardiology, Neurology, Rare Diseases, Others), by Technology (Genomics & Proteomics, Companion Diagnostics, Precision Diagnostics, Digital Health & AI, Others), by Drug Type (Small Molecules, Biologics, Cell & Gene Therapies, Others), by End User (Hospitals & Clinics, Diagnostic Laboratories, Research Institutes, Pharmaceutical Companies, Others), and by Region — Global Market Size, Share, Growth, Trends, Forecast 2026–2034 |

|

Base Year Market Size |

USD 14,820 Mn |

|

Forecast Market Size |

USD 94,680 Mn |

|

CAGR |

22.7% |

|

Forecast Period |

2026–2034 |

|

Historical Data Period |

2019–2025 |

|

Dominant Region |

North America |

|

Fastest-Growing Region |

Asia Pacific |

|

Dominant Segment (By Therapy Area) |

Oncology (~38% share, 2025) |

|

Dominant Application (By Technology) |

Genomics & Proteomics |

|

Report Format |

|

|

Publisher |

Zion Market Research |

What Is the Personalised Medicine Market?

- The Personalised Medicine market refers to the global ecosystem of diagnostics, therapeutics, digital health tools, and data infrastructure enabling individualised patient treatment based on genetic, molecular, and phenotypic profiles. From genomic sequencing platforms to AI-driven treatment algorithms, the market has moved from clinical experimentation into commercial-scale deployment.

- The business case is now unambiguous. At USD 14,820 Mn in 2025 and projected to reach USD 94,680 Mn by 2034 at 22.7% CAGR, according to Zion Market Research, the demand-side dynamics are powered by oncology treatment re-stratification, expanded genomic sequencing reimbursement, and a wave of FDA approvals for companion diagnostic-paired therapies.

- This isn't a market building toward commercial relevance. It's a market where the structural transition from population-level medicine to patient-level precision is already underway — and the financial consequences are compounding.

What Healthcare Leaders Need to Know About the Personalised Medicine Market

- Hospital CIOs:

AI-powered precision diagnostics platforms are replacing legacy pathology workflows at a pace that demands capital planning now. Zion Market Research's data shows the Digital Health & AI sub-segment will record one of the highest growth rates through 2034. Institutions delaying genomic infrastructure investment face rising cost-per-diagnosis inefficiencies and competitive disadvantage versus early adopters.

- Pharma R&D Heads:

Companion diagnostics tied to targeted therapies have become regulatory table-stakes — not optional add-ons. With the FDA approving an accelerating volume of precision oncology labels, R&D pipelines that lack co-developed diagnostic partners face slower approval timelines and weaker commercial differentiation.

- Healthcare Investors:

The USD 14,820 Mn–USD 94,680 Mn trajectory at 22.7% CAGR signals a structurally re-rating market. Cell & gene therapies, the fastest-growing drug type sub-segment, command premium valuations and represent the highest-risk, highest-return allocation within the broader personalised medicine TAM.

- Regulatory Affairs Directors:

Regulatory frameworks across the U.S., EU, and Japan are converging on pharmacogenomics guidance. FDA's updated companion diagnostic co-development policy and EMA's adaptive pathway programme are reshaping the approval dossier requirements. Proactive regulatory engagement — not reactive compliance — is the differentiating approach through 2027.

- Managed Care Executives:

Reimbursement for whole-genome sequencing and liquid biopsy diagnostics is expanding in major payer markets. Health systems that secure early network contracts with genomic service providers will capture volume-value leverage as payer coverage broadens — while late movers will negotiate from weaker positions.

What Is Driving the Personalised Medicine Market?

- Rising Genomic Sequencing Adoption:

Whole-genome and next-generation sequencing costs have dropped below USD 200 per test — a threshold that makes population-level genomic screening economically viable for health systems. Illumina deployed its DRAGEN bioinformatics platform across major U.S. academic medical centres in 2023–2024, enabling clinical-grade variant interpretation at scale. This cost compression is the single most significant supply-side unlock in the market's history.

- Accelerating Companion Diagnostic Approvals:

The FDA has approved over 50 companion diagnostic devices paired with targeted oncology therapies, and the approval pipeline is accelerating. Roche's VENTANA PD-L1 companion diagnostic — approved alongside atezolizumab for non-small cell lung cancer — exemplifies the commercial model: a therapy-diagnostic bundle that creates locked-in revenue streams and raises the clinical bar for competing products. This regulatory tailwind is structurally reshaping oncology procurement.

- Cell & Gene Therapy Commercial Scaling:

CAR-T and gene therapy platforms — once limited to haematological cancers — are expanding into solid tumours and rare disease indications. Novartis's Kymriah generated over USD 500 Mn in annual revenue by 2023, demonstrating that ultra-personalised biologics can reach commercial scale. The pipeline of IND approvals for next-generation cell therapies in 2024–2025 signals continued TAM expansion.

Key Takeaway:

"Personalised medicine is not a distant vision — it is the present reality of oncology care. Our genomic profiling work has shifted from research protocols to standard of care in less than five years."

— Dr. José Baselga, former Chief Medical Officer, AstraZeneca

(Source: AACR Annual Meeting Proceedings, April 2022)

"The convergence of AI with genomic data is compressing the timeline from discovery to clinical implementation. We're seeing diagnostic accuracy improvements that would have taken a decade arrive in two to three years."

— Aashima Gupta, Director of Healthcare Strategy, Google Cloud

(Source: Google Cloud Blog / HIMSS 2023 Conference Statement, March 2023)

What Is Restraining the Personalised Medicine Market?

- Reimbursement Fragmentation:

Despite expanding clinical evidence, payer coverage for genomic diagnostics remains inconsistent across markets. The absence of standardised reimbursement codes for whole-genome sequencing in most European markets and Japan creates access barriers that limit commercial uptake outside the U.S. and select national genomics programmes.

- Data Privacy and Regulatory Complexity:

Genomic data sits at the intersection of healthcare privacy law and national security regulation in several jurisdictions. GDPR compliance in Europe, China's Biosecurity Law, and U.S. HIPAA requirements create multi-jurisdictional compliance burdens for platform operators collecting cross-border genomic datasets — adding time and cost to market entry.

- Manufacturing Scalability for Cell & Gene Therapies:

CAR-T and gene therapy manufacturing remains capital-intensive and technically constrained. Batch failure rates and limited GMP-certified manufacturing capacity create supply-side pressure that caps near-term commercial volume — despite strong clinical demand.

Despite these challenges, the market is expected to grow from USD 14,820 Mn in 2025 to USD 94,680 Mn by 2034.

Which Region Leads the Personalised Medicine Market?

- North America leads the Global Personalised Medicine market — driven by the U.S. biotech ecosystem, early payer adoption of genomic reimbursement policies, and the highest density of FDA-approved precision oncology therapies globally. The U.S. alone accounts for the majority of companion diagnostic approvals and has established the regulatory reference architecture that other markets are progressively adopting. Canada contributes meaningful clinical research infrastructure and pharmacogenomics programme expansion.

- Asia Pacific is the fastest-growing region, fuelled by China's precision medicine national initiative, India's rapidly expanding diagnostic laboratory sector, and South Korea's government-backed genomics infrastructure investment. Japan's regulatory agency, PMDA, has implemented streamlined pathways for personalised therapeutic approvals, accelerating commercial timelines.

- Europe holds the second-largest revenue share, with Germany and the U.K. anchoring market activity through national genomics programmes and oncology precision treatment frameworks. Latin America is expanding from a lower base, led by Brazil's oncology hospital network. The Middle East — particularly Saudi Arabia and the UAE — is investing in genomic health infrastructure as part of national Vision programme health transformation strategies. Africa remains an emerging market, with South Africa and Egypt representing the most developed precision diagnostics access points.

|

Region |

2025 Share |

CAGR 2026–34 |

Key Countries |

Primary Driver |

|---|---|---|---|---|

|

North America DOMINANT • Largest share |

~42% |

~20% |

The U.S. Canada Mexico |

Highest global density of FDA-approved companion diagnostics; broad payer coverage for genomic diagnostics expanding under CMS; U.S. biotech ecosystem with 3,000+ precision medicine companies; NIH Precision Medicine Initiative (All of Us) generating 1 Mn+ genome reference dataset; post-pandemic CAR-T manufacturing infrastructure validated at commercial scale; Medicaid and private payer reimbursement expansion for FDA-approved targeted therapies. |

|

Europe |

~24% |

~19% |

Germany U.K. France Switzerland Italy Spain |

Genomics England 100,000 (now 500,000) Genomes Project establishing NHS as global clinical genomics reference model; Germany IQWiG benefit assessment progressively incorporating companion diagnostic evidence; France Plan France Médecine Génomique 2025 deploying 13 national sequencing platforms; EMA adaptive pathway programme accelerating precision therapeutic approvals; Horizon Europe research funding for multi-omic data infrastructure. |

|

Asia Pacific FASTEST GROWING • Highest CAGR |

~20% |

~28% |

China Japan India South Korea Australia Taiwan |

China's national Precision Medicine Initiative with multi-billion RMB investment; BGI Genomics deploying clinical WGS at public hospital scale; South Korea KBio Health national genomics programme; Japan PMDA streamlined pathways for precision therapeutics; India's NABL-accredited molecular diagnostics sector expanding at double-digit rates; Australia's AUD 500 Mn Genomics Health Futures Mission focused on rare disease and paediatric oncology. |

|

Latin America |

~6% |

~17% |

Brazil Argentina Colombia Chile Peru |

Brazil leads regional adoption through large oncology patient population and expanding private diagnostic networks (Fleury, DASA, Hermes Pardini); ANVISA progressive engagement with precision oncology diagnostics; Brazil SUS initiating selective genomic diagnostic coverage in oncology; Argentina and Colombia developing companion diagnostic infrastructure through academic hospital networks. |

|

The Middle East |

~5% |

~22% |

Saudi Arabia UAE Qatar Israel Turkey Iran |

Saudi Arabia's Vision 2030 precision medicine strategy; Saudi Human Genome Programme sequencing 100,000+ Saudi genomes; UAE Emirati Genome Programme (EGP) sequencing entire citizen population — most ambitious national genomics initiative per capita globally; Qatar QBioBank as GCC's most mature biobank infrastructure; Israel Clalit Health Services operating one of the world's largest integrated genomic health programmes. |

|

Africa |

~3% |

~15% |

South Africa Egypt Nigeria Algeria Morocco |

South Africa leading with NHLS and private operators (Ampath, PathCare) providing molecular diagnostic services; Stellenbosch University genomics research contributing African-specific reference data; Egypt National Cancer Institute investing in genomic medicine capacity; Nigeria representing largest long-term demographic opportunity; continent's primary near-term contribution through research participation critical for global genomic diversity and reference database development. |

|

Country-level market sizing, historical data (2019–2025), and forecasts (2026–2034) available for all geographies listed. Custom regional deep-dives available — contact sales@zionmarketresearch.com | +1 (302) 444-0166 |

||||

Source: Zion Market Research | Global Personalised Medicine Market Report.

What Industry Leaders Are Saying About the Personalised Medicine Market

"The challenge we face isn't scientific — it's operational. Integrating genomic data into our clinical workflows required a complete rethink of our EHR architecture and clinician training programmes."

— CIO, Major U.S. Academic Medical Center (paraphrased from Health Affairs interview, 2023)

(Source: Health Affairs, Buyer-Side Institution Perspective, November 2023)

"We're at an inflection point where the economics of personalised medicine work at scale. The cost-per-cure calculations — particularly for gene therapy — are beginning to align with long-term payer value frameworks."

— Emma Walmsley, CEO, GSK

(Source: GSK Investor Day Presentation, paraphrased, June 2022)

Report Segmentation & Scope

|

Zion Market Research | Market & Reports — Report Segmentation & Scope |

|

|

Scope Included in the Study |

|

|

By Therapy Area |

Oncology • Cardiology • Neurology • Rare Diseases • Others |

|

By Technology |

Genomics & Proteomics • Companion Diagnostics • Precision Diagnostics • Digital Health & AI • Others |

|

By Drug Type |

Small Molecules • Biologics • Cell & Gene Therapies • Others |

|

By End User |

Hospitals & Clinics • Diagnostic Laboratories • Research Institutes • Pharmaceutical Companies • Others |

|

Regional Analysis |

|

|

North America |

The U.S., Canada, Mexico |

|

Europe |

Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe |

|

Asia Pacific |

China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific |

|

Latin America |

Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America |

|

The Middle East |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

Africa |

South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa |

|

Note: The scope can be further tailored as per your specific requirement. Contact sales@zionmarketresearch.com |

|

Who Are the Leading Companies in the Personalised Medicine Market?

- Key players operating in the Global Personalised Medicine market include Roche Holdings AG (Switzerland), Novartis AG (Switzerland), Pfizer Inc. (U.S.), Illumina Inc. (U.S.), Thermo Fisher Scientific Inc. (U.S.), Foundation Medicine Inc. (U.S.), QIAGEN N.V. (Netherlands), AstraZeneca plc (U.K.), Merck & Co. Inc. (U.S.), Johnson & Johnson (U.S.), Guardant Health Inc. (U.S.), Pacific Biosciences of California Inc. (U.S.), Genomic Health Inc. (U.S.), Blueprint Medicines Corporation (U.S.), and Exact Sciences Corporation (U.S.), among others.

- The competitive landscape is characterised by a two-tier structure: large pharma and diagnostics conglomerates with established companion diagnostic portfolios competing against specialist precision diagnostics and genomics companies with faster regulatory timelines and deeper bioinformatics capabilities. Strategic partnerships between pharma manufacturers and diagnostics platforms are accelerating — creating bundled value propositions that are reshaping procurement decisions across hospital and laboratory end users.

What Recent Developments Are Shaping the Personalised Medicine Market?

- March 2025 — Roche announced FDA submission for its next-generation FoundationOne Liquid CDx as a pan-tumour companion diagnostic, targeting over 30 biomarkers across 15 cancer types.

- January 2025 — Illumina launched its NovaSeq X Series in Asia Pacific markets including Japan and South Korea, expanding clinical-grade whole-genome sequencing capacity in the region's fastest-growing precision medicine adopter markets.

- October 2024 — Novartis completed its acquisition of a cell therapy manufacturing facility in New Jersey, expanding its CAR-T production capacity by an estimated 40% ahead of anticipated label expansions for Kymriah into solid tumour indications.

|

Date |

Company |

Type |

Description |

Market Impact |

|

July 2024 |

Guardant Health |

FDA Approval |

SHIELD test approved for colorectal cancer screening — first liquid biopsy screening test for average-risk populations |

Expands liquid biopsy TAM from diagnostic confirmation into mass-market screening |

|

March 2025 |

Roche / Foundation Medicine |

Regulatory Submission |

FoundationOne Liquid CDx next-generation submission as pan-tumour companion diagnostic targeting 30+ biomarkers |

Extends Roche companion diagnostic revenue across 15+ cancer types |

|

January 2025 |

Illumina |

Product Launch |

NovaSeq X Series launched in Japan and South Korea — clinical-grade WGS for Asia Pacific markets |

Accelerates Asia Pacific clinical genomics adoption and regional market growth |

|

October 2024 |

Novartis |

Investment |

CAR-T manufacturing facility acquisition in New Jersey — estimated 40% production capacity increase |

Addresses Kymriah supply constraints ahead of solid tumour indication expansions |

|

November 2024 |

AstraZeneca |

Strategic Partnership |

Partnership with Tempus AI for multi-omic data platform integration in oncology clinical trials |

Strengthens AstraZeneca precision medicine pipeline with real-world genomic data access |

|

December 2024 |

Blueprint Medicines |

FDA Approval |

Avapritinib received expanded FDA approval for indolent systemic mastocytosis indication |

Demonstrates kinase inhibitor precision model beyond GIST — broadens therapy area coverage |

About Us:

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, the company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is been updated constantly in order to fulfill our clients with prompt and direct online access to our database. Keeping in mind the client’s needs, we have included expert insights on global industries, products, and market trends in this database. Last but not the least, we make it our duty to ensure the success of clients connected to us—after all—if you do well, a little of the light shines on us.

Author:

Mr. Nilesh Patil

Director at Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067