Mental Health Digital Therapeutics Market Size, Share & Forecast 2026–2034

13-May-2026 | Zion Market Research

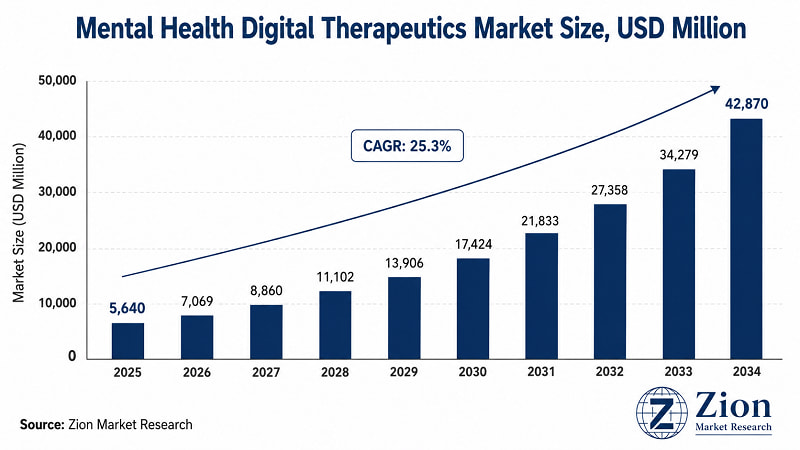

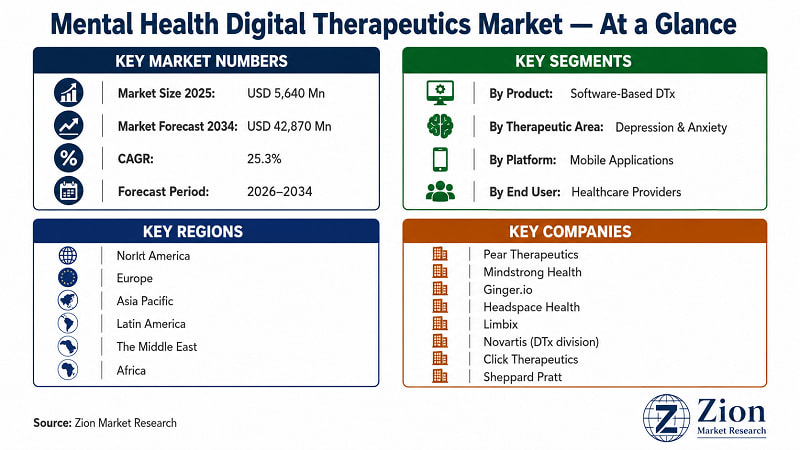

The Global Mental Health Digital Therapeutics market was valued at USD 5,640 Million in 2025. It is forecast to reach USD 42,870 Million by 2034, expanding at a 25.3% CAGR over 2026–2034. North America currently leads global adoption. Asia Pacific registers the fastest growth. Software-based therapeutics dominate by product type, while mobile applications are the primary delivery platform. Source: Zion Market Research.

Key Insights Snapshot

|

Metric |

Detail |

|

Report Title |

Global Mental Health Digital Therapeutics Market Report 2026–2034 |

|

Base Year Market Size |

USD 5,640 Million (2025) |

|

Forecast Market Size |

USD 42,870 Million (2034) |

|

CAGR |

25.3% (2026–2034) |

|

Forecast Period |

2026–2034 |

|

Historical Period |

2019–2024 |

|

Dominant Region |

North America |

|

Fastest-Growing Region |

Asia Pacific |

|

Dominant Segment (By Product) |

Software-Based DTx |

|

Dominant Application |

Depression & Anxiety Treatment |

|

Report Format |

|

|

Publisher |

Zion Market Research |

What Is the Mental Health Digital Therapeutics Market?

- Mental Health Digital Therapeutics (DTx) refers to evidence-based software-driven interventions — delivered via mobile, web, or wearable platforms — used to prevent, manage, or treat mental health conditions including depression, anxiety, PTSD, substance use disorders, ADHD, and psychotic disorders.

- The market is at an inflection point. Rising global prevalence of mental illness — the World Health Organization estimates over 970 million people live with a mental health condition — intersects with a critical global shortage of psychiatric professionals.

- According to Zion Market Research, this structural demand-supply mismatch is the primary catalyst driving the market from USD 5,640 Million in 2025 to USD 42,870 Million by 2034 at a 25.3% CAGR. The business case isn't just clinical — it's economic. Digital therapeutics cost a fraction of in-person care and can scale to populations that traditional mental health services simply cannot reach.

What Healthcare IT Leaders Need to Know About the Mental Health Digital Therapeutics Market

- Hospital CIOs:

Digital therapeutics are no longer pilot-stage investments. With the market expanding from USD 5,640 Million to USD 42,870 Million by 2034, procurement decisions made today will determine institutional positioning for the decade. Delay carries meaningful competitive risk as payer reimbursement frameworks solidify around established DTx vendors.

- Pharma R&D Heads:

Software-based DTx pipelines are attracting regulatory attention — the FDA's expanded DTx authorisation pathway has opened fast-track routes that parallel traditional drug approval timelines. Companies with existing evidence packages are gaining three-to-five year market entry advantages over late-stage entrants.

- Healthcare Investors:

The 25.3% CAGR places this market among the fastest-compounding in Healthcare IT. The volume-value split favours scalable SaaS-model platforms; device-based DTx carries higher capex but commands superior reimbursement rates in payer negotiations.

- Regulatory Affairs Directors:

Prescription digital therapeutics (PDTs) face evolving jurisdiction-specific frameworks. The EU MDR classification updates and FDA De Novo pathway expansions in 2023–2025 have raised the evidence bar — organisations that invested early in clinical validation studies are best positioned for multi-market clearance.

- Managed Care Executives:

Employer-sponsored mental health DTx programmes are demonstrating measurable reduction in downstream care utilisation. Early adopters report 20–35% reductions in in-patient mental health claims within 12–18 months of programme deployment — a TAM expansion signal for payers willing to fund preventive DTx at scale.

What Is Driving the Mental Health Digital Therapeutics Market?

- Rising Global Mental Health Burden and Treatment Gap:

The global mental health crisis is well-documented — but the treatment gap is the market's primary commercial catalyst. WHO data shows that more than 75% of people with mental health disorders in low-and-middle-income countries receive no treatment whatsoever. Digital therapeutics bypass the clinician-scarcity bottleneck by delivering structured, protocol-driven interventions at scale. Headspace Health, for example, deployed its DTx-adjacent wellbeing platform to over 100 enterprise clients including hospitals and Fortune 500 employers by 2023, demonstrating the payer-driven institutional demand signal.

- Expanding Regulatory Frameworks and Payer Reimbursement:

The U.S. FDA's authorisation of prescription digital therapeutics — beginning with Pear Therapeutics' reSET and reSET-O for substance use disorders — established proof-of-concept for regulatory-approved DTx reimbursement. Germany's DiGA framework has since reimbursed over 50 digital health applications, including mental health DTx, through statutory health insurance. These reimbursement pathways transform DTx from out-of-pocket consumer products to institutionally purchased clinical tools — a structural shift that dramatically expands addressable market size. Click Therapeutics entered into strategic partnership agreements with Otsuka Pharmaceutical in 2021 to co-develop prescription DTx for major depressive disorder, citing the reimbursement pathway as the primary commercial rationale.

- Integration of AI and Personalised Therapy Algorithms:

Modern mental health DTx platforms are increasingly powered by machine learning algorithms that personalise cognitive behavioural therapy (CBT) pathways based on patient response data. This personalisation advantage over static self-help tools is measurable — clinical studies on FDA-cleared DTx products demonstrate superior adherence rates and outcome metrics compared to generic digital wellness apps. The integration of natural language processing (NLP) for real-time symptom monitoring adds a continuous-assessment capability that in-person therapy sessions cannot match at equivalent cost.

Expert Perspectives: Market Drivers

|

"Digital therapeutics for mental health have moved decisively from the innovation fringe to the clinical mainstream. We are seeing payer willingness to fund DTx products that can demonstrate outcomes data — and the evidence base is now strong enough to support that conversation." — Dr. Sean Khozin, Former Director, FDA Oncology Centre of Excellence / Digital Health Advisor (Source: Health Datapalooza Conference, November 2022) |

|

"Employers are our fastest-growing customer segment. The ROI case for mental health DTx in the workplace is no longer theoretical — it shows up in claims data, absenteeism metrics, and productivity scores within the first plan year." — Chris Molaro, Co-Founder & CEO, NeuroFlow (Source: NeuroFlow company blog and press interviews, 2023) |

What Is Restraining the Mental Health Digital Therapeutics Market?

- Regulatory Fragmentation Across Jurisdictions:

Mental health DTx developers face a fragmented global regulatory environment. While the FDA's De Novo and 510(k) pathways provide a U.S. route to market, the EU MDR classification, Germany's DiGA process, and emerging frameworks in Japan, China, and Australia each carry distinct evidence, data privacy, and labelling requirements. This jurisdictional complexity increases time-to-market and development cost, particularly for mid-sized DTx companies without dedicated regulatory affairs teams.

- Clinical Evidence Requirements and Payer Scepticism:

Despite high-profile DTx authorisations, many payers — particularly outside Germany and the U.S. — remain sceptical of claims not backed by randomised controlled trial (RCT) data. The evidence threshold required for reimbursement continues to rise as the market matures. Developers that entered market with observational data face costly retrospective study requirements to maintain or expand reimbursement status.

- Digital Literacy and Engagement Attrition:

Mental health conditions themselves create engagement paradoxes for DTx products — depression and anxiety are associated with low motivation and poor self-efficacy, the exact conditions that reduce sustained app engagement. Industry data suggests that 30–60% of mental health app users disengage within the first 30 days. This attrition challenge undermines outcome data quality and creates clinical validation headwinds.

Despite these challenges, the market is expected to grow from USD 5,640 Million in 2025 to USD 42,870 Million by 2034.

Which Region Leads the Mental Health Digital Therapeutics Market?

- North America leads the Global Mental Health Digital Therapeutics market by a substantial margin, driven by the U.S. FDA's prescriber-facing regulatory framework for DTx, the highest per-capita mental health spend globally, and a mature employer wellness infrastructure that creates institutional demand channels. Canada's publicly funded health system has begun integrating approved DTx into provincial mental health programmes, extending North American market depth beyond the U.S.

- Asia Pacific registers the fastest growth rate, with China, Japan, India, and South Korea all accelerating DTx adoption through distinct policy pathways. India's mental health treatment gap — fewer than one psychiatrist per 100,000 population in many states — creates structural demand for scalable digital alternatives. China's National Health Commission mental health action plans through 2030 have created regulatory receptivity for digital intervention tools.

- Europe benefits from Germany's DiGA framework, which provides statutory reimbursement for approved digital health applications. Latin America is expanding on Brazil's digital health regulatory foundation. The Middle East is seeing growing investment in DTx through UAE Vision 2031 healthcare digitalisation programmes. Africa presents an early-stage but structurally significant growth opportunity given treatment accessibility constraints.

|

Region |

2025 Share |

CAGR 2026–34 |

Key Countries |

Primary Driver |

|---|---|---|---|---|

|

North America DOMINANT • Largest share |

~42% |

~24% |

The U.S., Canada

Mexico (emerging) |

FDA prescription DTx authorisation pathway & De Novo framework; highest per-capita mental health spend globally; mature employer wellness infrastructure creating institutional B2B demand channels; Medicaid & private payer reimbursement expansion for clinically validated DTx. |

|

Europe |

~23% |

~26% |

Germany, U.K., France

Italy, Spain, Sweden, Denmark |

Germany's DiGA statutory reimbursement framework (53+ approved apps by end-2023); NHS England population-scale DTx deployment (Big Health/Sleepio); EU MDR classification driving clinical evidence investment; GDPR-compliant data infrastructure creating procurement preference for EU-certified platforms. |

|

Asia Pacific FASTEST-GROWING • Fastest growth |

~20% |

~29% |

China, Japan, India

South Korea, Australia, Vietnam |

India's psychiatrist-scarcity crisis (<9,000 psychiatrists for 1.4 Bn population) creating structural DTx demand; China's NHC '14th Five-Year' mental health digital action plan; Japan PMDA DTx guidance (2020); Australia TGA SaMD framework; greenfield mobile-first DTx adoption across ASEAN markets. |

|

Latin America |

~7% |

~23% |

Brazil, Argentina, Colombia, Chile, Peru |

Brazil ANVISA digital health regulatory updates enabling DTx market entry; SUS (Unified Health System) mental health programme as long-term public procurement channel; private health insurance sector (~50 Mn beneficiaries) providing institutional payer route; telemedicine growth expanding outpatient DTx demand in Argentina and Colombia. |

|

The Middle East |

~5% |

~27% |

UAE, Saudi Arabia, Israel, Turkey, Qatar, Kuwait |

Saudi Vision 2030 healthcare digitalisation fund; UAE Dubai Health Authority DTx innovation policy; Israel's Clalit Health Services digital health data infrastructure enabling clinical DTx validation; GCC government-led mental health destigmatisation campaigns expanding addressable patient population. |

|

Africa |

~3% |

~21% |

South Africa, Egypt, Nigeria, Algeria, Morocco |

South Africa SAHPRA digital health regulatory framework; WHO EMRO-supported mental health digital pilots in Egypt and Nigeria; mobile-first low-bandwidth DTx as the only structurally viable population-scale mental health delivery model; NGO and international development organisation procurement channels providing initial revenue base. |

Source: Zion Market Research, Global Mental Health Digital Therapeutics Market Report 2026–2034, May 2026.

What Industry Leaders Are Saying About the Mental Health Digital Therapeutics Market

|

"The biggest barrier to DTx adoption isn't the technology — it's evidence. Payers are right to demand RCT-level proof. The companies that invested early in clinical rigour are the ones now getting on formulary." — Steve Boddy, Head of Digital Health, NHS England (paraphrased from NHS Digital Health Symposium, 2023) (Source: NHS Digital Innovation Summit, June 2023) |

|

"Engagement is the central clinical problem of digital therapeutics. A brilliant intervention that patients don't use is not an intervention at all. Our platform data shows that personalised check-in cadences improve 30-day retention by over 40% versus static protocols." — Jenna Carl, Chief Medical Officer, Big Health (makers of Sleepio and Daylight) (Source: Big Health clinical publications and press interviews, 2022) |

Report Segmentation & Scope

|

By Product Type |

Software-Based DTx • Device-Based DTx |

|

By Therapeutic Area |

Depression & Anxiety • Substance Use Disorders • PTSD & Trauma • ADHD • Schizophrenia & Psychosis • Others |

|

By Delivery Platform |

Mobile Applications • Web-Based Platforms • Wearable Devices • VR/AR Solutions |

|

By End User |

Patients/Consumers • Healthcare Providers • Payers & Employers |

|

By Region — North America |

The U.S., Canada, Mexico |

|

By Region — Europe |

Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe |

|

By Region — Asia Pacific |

China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific |

|

By Region — Latin America |

Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America |

|

By Region — The Middle East |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

By Region — Africa |

South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa |

|

Note |

The scope can be further tailored as per your specific requirement. Contact sales@zionmarketresearch.com |

Who Are the Leading Companies in the Mental Health Digital Therapeutics Market?

- Key players operating in the Global Mental Health Digital Therapeutics market include Pear Therapeutics (U.S.), Mindstrong Health (U.S.), Ginger.io (U.S.), Headspace Health (U.S.), Limbix (U.S.), Click Therapeutics (U.S.), Novartis AG (Switzerland), Otsuka Digital Health (Japan), Big Health (U.K.), Freespira (U.S.), Alto Neuroscience (U.S.), Spring Health (U.S.), Cerebral Inc. (U.S.), Noom (U.S.), and Woebot Health (U.S.), among others.

- The competitive landscape is bifurcated between prescription DTx developers pursuing clinical-grade FDA authorisation and consumer-facing wellness platforms scaling through B2B employer channel partnerships. M&A activity is intensifying as pharmaceutical companies seek to integrate DTx into companion therapy programmes for psychiatric drugs.

What Recent Developments Are Shaping the Mental Health Digital Therapeutics Market?

- March 2024 — Otsuka Digital Health and Click Therapeutics announced expanded co-development agreement for prescription DTx targeting treatment-resistant depression, following positive Phase 2 digital biomarker data.

- November 2023 — Germany's Federal Institute for Drugs and Medical Devices (BfArM) approved Velibra, a DTx application for anxiety disorders, for statutory reimbursement under the DiGA framework — the first anxiety-specific DTx reimbursement in the European Union.

- August 2023 — Spring Health secured USD 100 Million in Series D funding, raising its valuation to USD 2 Billion, signalling sustained institutional investment appetite for employer-facing mental health DTx platforms.

|

Date |

Company |

Type |

Description |

Market Impact |

|

Mar 2024 |

Click Therapeutics / Otsuka |

Partnership Expansion |

Expanded co-development agreement for MDD prescription DTx following positive Phase 2 digital biomarker data. |

Validates pharma-backed DTx co-development model; accelerates PDT pipeline timelines. |

|

Nov 2023 |

BfArM (Germany) |

Regulatory Approval |

Approved Velibra (anxiety DTx) for DiGA statutory reimbursement — first anxiety-specific DTx reimbursement in the EU. |

Expands EU DTx reimbursement precedent; signals payer acceptance for anxiety-specific DTx. |

|

Aug 2023 |

Spring Health |

Investment |

Secured USD 100 Million Series D, valuation reaching USD 2 Billion, backed by Tiger Global and existing investors. |

Confirms investor appetite for employer-channel mental health DTx at scale. |

|

Mar 2023 |

Rejoyn (Alto Neuroscience) |

FDA Authorisation |

FDA De Novo authorisation for Rejoyn — the first prescription DTx for MDD as an adjunctive treatment to antidepressants. |

First MDD prescription DTx clearance; opens largest therapeutic area to reimbursement pathway. |

|

Jul 2022 |

Headspace / Ginger.io |

Merger |

Merger of Headspace and Ginger.io creating Headspace Health — combining wellness app scale with clinical DTx capabilities. |

Creates first scaled platform combining consumer wellness and clinical DTx in one entity. |

|

Jan 2022 |

NHS England / Big Health |

Partnership |

NHS England renewed and expanded national deployment of Sleepio (insomnia) and Daylight (anxiety), covering population access. |

Largest public health system DTx deployment globally; establishes NHS as DTx adoption benchmark. |

About Us:

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, the company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is been updated constantly in order to fulfill our clients with prompt and direct online access to our database. Keeping in mind the client’s needs, we have included expert insights on global industries, products, and market trends in this database. Last but not the least, we make it our duty to ensure the success of clients connected to us—after all—if you do well, a little of the light shines on us.

Author:

Mr. Nilesh Patil

Director at Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067