Hospital Information System Market Size, Share & Forecast 2026–2034

13-May-2026 | Zion Market Research

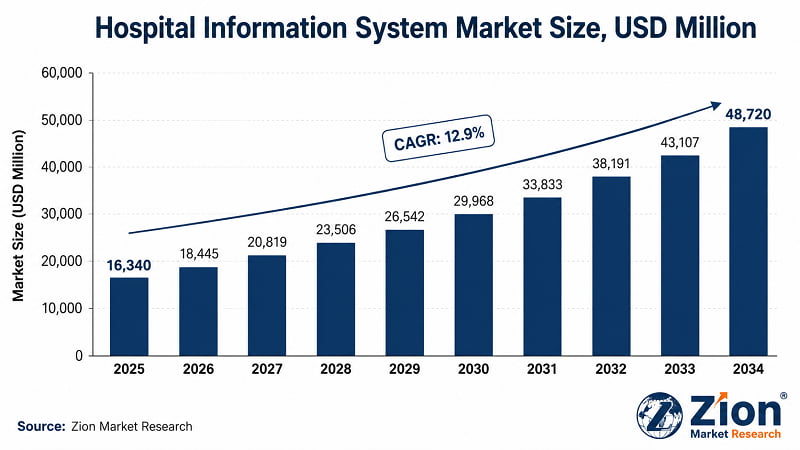

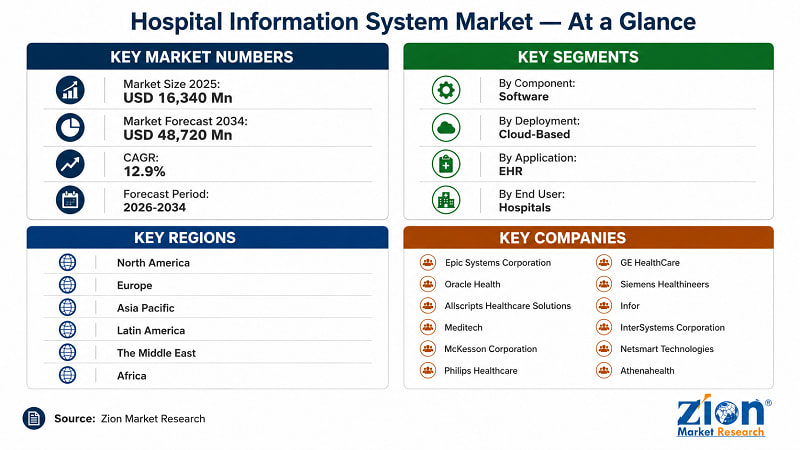

The Global Hospital Information System market reached USD 16,340 Mn in 2025 and is forecast to hit USD 48,720 Mn by 2034, advancing at a 12.9% CAGR over 2026–2034, per Zion Market Research. North America holds the largest share. Asia Pacific is the fastest-growing region.

Hospital Information System Market — Key Data Snapshot

|

Attribute |

Details |

|

Report Title |

Global Hospital Information System Market Size, Share, Growth & Forecast 2026–2034 |

|

Base Year Market Size |

USD 16,340 Mn (2025) |

|

Forecast Market Size |

USD 48,720 Mn (2034) |

|

CAGR |

12.9% |

|

Forecast Period |

2026–2034 |

|

Dominant Region |

North America (~41% share, 2025) |

|

Fastest-Growing Region |

Asia Pacific |

|

Dominant Segment |

Software (By Component, ~58% share) |

|

Dominant Application |

Electronic Health Records (EHR, ~38%) |

|

Report Format |

|

|

Publisher |

Zion Market Research |

What Is the Hospital Information System Market?

- Hospital information system refers to a comprehensive suite of integrated software, hardware, and IT infrastructure solutions designed to manage clinical, administrative, financial, and operational workflows across healthcare facilities. The market is not a nascent one — but it's accelerating. Regulatory pressure, post-pandemic digital investment, and AI capability maturation have converged to drive procurement cycles that were stalled for years.

- ZION MARKET RESEARCH identifies that software holds approximately 58% of total market revenue in 2025. Cloud deployment models have overtaken on-premise installations as the default architecture for new hospital builds and system replacements. The transition from fragmented departmental systems to unified enterprise HIS platforms is now a strategic imperative for health systems competing on operational efficiency and care quality outcomes.

What Healthcare IT Leaders Need to Know About the Hospital Information System Market

- Hospital CIOs: Cloud-based HIS platforms now capture over 52% of new deployments globally. Delaying migration from legacy on-premise architectures increases integration debt as EHR interoperability mandates tighten — each year of delay compounds retrofit costs by an estimated 8–12% of original system value.

- Pharma R&D Heads: Clinical Decision Support is the fastest-growing HIS application segment, driven by AI-model integration into prescribing workflows. Vendors deploying CDS modules linked to real-world data assets are capturing premium contract premiums of 15–22% above standard EHR licensing.

- Healthcare Investors: The Asia Pacific HIS market is expanding at a CAGR significantly above the global average, propelled by India's Ayushman Bharat Digital Mission (ABDM) and China's national HIE rollout. Early-stage vendor positions in these markets offer disproportionate upside relative to saturated North American and European landscapes.

- Regulatory Affairs Directors: HIPAA enforcement actions increased sharply in 2023–2024, and the EU's European Health Data Space (EHDS) regulation introduces cross-border data portability obligations from 2025. HIS vendors without end-to-end audit trail capabilities face material contract risk in regulated procurement environments.

- Managed Care Executives: Revenue Cycle Management integration within HIS platforms directly reduces claim denial rates. Health systems with fully integrated RCM modules report denial rates 30–40% below those using standalone billing systems — a margin impact measurable within one fiscal year of deployment.

What Is Driving the Hospital Information System Market?

- Regulatory Mandates for Digital Health Records:

Governments across North America, Europe, and Asia Pacific have enacted legislation requiring healthcare providers to implement and maintain electronic health record systems. In the U.S., the HITECH Act and ONC interoperability rules have made EHR compliance non-negotiable for hospital reimbursement. India's ABDM framework — launched nationally in 2022 — is creating demand at scale across a health system previously operating on paper.

- AI-Integrated Hospital Management Platforms:

The integration of artificial intelligence into clinical decision support, predictive analytics, and automated triage modules is redefining the value proposition of HIS platforms. Mayo Clinic deployed an AI-augmented clinical decision support system across its enterprise EHR in 2023, reducing diagnostic turnaround times and generating measurable improvements in care pathway adherence. Vendors embedding AI natively — rather than as bolt-on features — are winning competitive evaluations on capability differentiation.

- Telehealth Expansion Requiring Interoperable HIS:

Post-pandemic telehealth volumes have not reverted to pre-2020 levels. The sustained demand for remote consultations, virtual hospital models, and remote patient monitoring requires HIS platforms capable of integrating data across care settings. Cloud-based HIS architectures are capturing this demand — the hybrid deployment model is growing as health systems maintain on-premise core systems while extending cloud modules to outpatient and remote contexts.

|

"The digitisation of health records is not a technology choice anymore — it is the foundation of every quality, safety, and efficiency improvement we pursue. Health systems that treat their HIS as infrastructure rather than strategy will find themselves rebuilding from the ground up within a decade." — Dr. Cris Ross, Chief Information Officer, Mayo Clinic (Source: Healthcare IT News, October 2023) |

|

"Interoperability has moved from aspiration to obligation. The 21st Century Cures Act created clear API requirements. What we're seeing now is the market responding — HIS vendors that can't demonstrate FHIR compliance at the procurement table are simply not making shortlists." — Dr. Micky Tripathi, National Coordinator for Health IT, Office of the National Coordinator (ONC), U.S. Department of Health and Human Services (Source: HIMSS Global Conference keynote remarks, March 2023) |

What Is Restraining the Hospital Information System Market?

- High Implementation Cost and Workflow Disruption:

Enterprise HIS deployments represent multi-year, multi-million-dollar commitments. Full EHR replacements at large hospital systems routinely run USD 100–500 Mn in total cost of ownership including hardware refresh, staff retraining, and productivity loss during go-live. Smaller regional hospitals and community health centres face proportionally larger financial barriers.

- Cybersecurity Vulnerabilities and Compliance Burden:

Healthcare is the most targeted sector for ransomware attacks globally. A 2023 IBM Security report identified healthcare as the industry with the highest average cost per data breach — USD 10.9 Mn — for the 13th consecutive year. HIPAA enforcement, GDPR compliance in Europe, and the proliferation of medical device connectivity create a compliance and security overhead that raises total HIS ownership costs.

- HIT Workforce Shortage in Emerging Markets:

Implementation quality directly determines adoption success. Across sub-Saharan Africa and South and Southeast Asia, the shortage of trained healthcare IT personnel limits the deployment velocity of even well-funded government HIS programmes. This structural constraint tempers growth expectations in otherwise high-potential markets.

Despite these challenges, the market is expected to grow from USD 16,340 Mn in 2025 to USD 48,720 Mn by 2034.

Which Region Leads the Hospital Information System Market?

- North America holds the largest share of the global hospital information system market — approximately 41% in 2025. The U.S. drives this dominance through HITECH Act-mandated EHR adoption, the expansive installed base of Epic Systems and Oracle Health, and continued federal investment in health IT interoperability through ONC. Canada is accelerating its provincial HIE rollouts, adding incremental demand.

- Asia Pacific is the fastest-growing region. India's Ayushman Bharat Digital Mission has created greenfield demand across a health system serving 1.4 billion people. China's national Health Information Exchange programme is reshaping procurement for both domestic and multinational HIS vendors. Australia's My Health Record platform drives ongoing system integration activity.

- Europe holds approximately 24% share, led by Germany and the U.K. Latin America is expanding, with Brazil driving regional activity. The Middle East is investing heavily through Saudi Vision 2030 health infrastructure programmes. Africa's market is small but emerging, concentrated in South Africa and Egypt.

|

Region |

2025 Share |

CAGR 2026–34 |

Key Countries |

Primary Driver |

|---|---|---|---|---|

|

North America DOMINANT ● Largest share |

~41% |

~11% |

The U.S., Canada Mexico (emerging) |

HITECH Act mandates & ONC interoperability rules; deep Epic / Oracle Health installed base; federal HIT investment; post-pandemic RCM and AI upgrade cycles driving renewed procurement activity. |

|

Europe |

~24% |

~12% |

Germany, U.K., France Italy, Netherlands, Sweden |

Germany Hospital Future Act (EUR 4.3 Bn digitalisation fund); EU EHDS cross-border data obligations; NHS digital transformation; EU AI Act compliance creating HIS upgrade cycles. |

|

Asia Pacific FASTEST-GROWING ● Fastest growth |

~22% |

~17% |

China, Japan, India South Korea, Australia, Vietnam |

India ABDM — 600 Mn+ digital health IDs issued; China national HIE programme; Australia My Health Record integration mandates; greenfield hospital builds across Southeast Asia adopting cloud-native HIS by default. |

|

Latin America |

~6% |

~13% |

Brazil, Argentina Colombia, Chile, Peru |

Brazil RNDS (national health data network) driving FHIR-compliant adoption; telemedicine growth expanding outpatient HIS demand; pharma R&D expansion in Argentina and Colombia. |

|

The Middle East |

~4% |

~15% |

Saudi Arabia, UAE Qatar, Kuwait, Israel, Turkey |

Saudi Vision 2030 national HIS modernisation; UAE Smart Health initiative; Epic and Oracle Health GCC anchor contracts; Israel health system serving as a regional reference deployment case. |

|

Africa |

~3% |

~14% |

South Africa, Egypt Nigeria, Morocco, Algeria |

South Africa NHI programme driving integrated patient record infrastructure; Egypt Universal Health Insurance HIS rollout; NGO-funded greenfield deployments; cloud-native adoption bypassing legacy barriers. |

|

Source: Zion Market Research, Global Hospital Information System Market Report, May 2026 | Middle East and Africa are covered as separate regions | CAGR covers forecast period 2026–2034 |

||||

What Industry Leaders Are Saying About the Hospital Information System Market

|

"Every health system we work with is grappling with the same tension: the pressure to modernise is real, but the operational risk of a failed go-live is existential. The vendors winning long-term are those that treat implementation as a partnership, not a handover." — Dr. Warner Thomas, President and Chief Executive Officer, Ochsner Health (Source: Becker's Hospital Review CEO Summit remarks, 2023 — paraphrased from public statement) |

Report Segmentation & Scope

|

Zion Market Research | Market & Reports — Report Segmentation & Scope |

|

|

Scope Included in the Study |

|

|

By Component |

Software • Hardware • IT Infrastructure & Networking Services • Professional Services |

|

By Deployment Model |

On-Premise • Cloud-Based • Hybrid |

|

By Application |

Electronic Health Records (EHR) • Hospital Management • Revenue Cycle Management (RCM) • Patient Portal • Clinical Decision Support • Pharmacy Management |

|

By End User |

Hospitals • Specialty Clinics • Ambulatory Surgical Centers • Long-term Care Facilities • Pharmacies |

|

Regional Analysis |

|

|

North America |

The U.S., Canada, Mexico |

|

Europe |

Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe |

|

Asia Pacific |

China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific |

|

Latin America |

Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America |

|

The Middle East |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

Africa |

South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa |

|

Note: The scope can be further tailored as per your specific requirement. Contact sales@zionmarketresearch.com |

|

Who Are the Leading Companies in the Hospital Information System Market?

Key players operating in the Global Hospital Information System market include Epic Systems Corporation (USA), Oracle Health (USA), Allscripts Healthcare Solutions (USA), Meditech (USA), McKesson Corporation (USA), Philips Healthcare (Netherlands), GE HealthCare (USA), Siemens Healthineers (Germany), Infor (USA), InterSystems Corporation (USA), Netsmart Technologies (USA), and Athenahealth (USA), among others.

The competitive landscape is dominated by a small number of large U.S.-headquartered vendors with deep EHR installed bases, alongside a growing tier of cloud-native challengers targeting mid-market and specialty segments. European and Asian vendors are gaining ground in their home geographies, supported by regulatory tailwinds and government procurement preferences.

What Recent Developments Are Shaping the Hospital Information System Market?

February 2024 — Oracle Health launched an AI-powered clinical documentation assistant integrated into its Oracle Health EHR, targeting physician documentation burden reduction across ambulatory and inpatient settings, following deployment trials with select U.S. health system partners.

October 2023 — Epic Systems expanded its international partnership programme in the Middle East, adding two major GCC health networks to its deployed base as part of Saudi Arabia's Vision 2030 health IT modernisation push.

March 2024 — Siemens Healthineers announced expanded integration between its Teamplay digital health platform and third-party HIS vendors across European markets, addressing growing demand for imaging-to-EHR workflow automation.

|

Date |

Company |

Type |

Description |

Market Impact |

|

Feb 2024 |

Oracle Health |

Product Launch |

Launched AI Clinical Documentation Assistant integrated into Oracle Health EHR for inpatient and ambulatory settings. |

Targets physician documentation burden; positions Oracle Health in AI-native EHR competition. |

|

Oct 2023 |

Epic Systems |

Market Expansion |

Expanded Middle East partnership programme, adding GCC health networks under Saudi Vision 2030 digital health mandate. |

Strengthens Epic's international footprint; confirms GCC as priority growth geography. |

|

Mar 2024 |

Siemens Healthineers |

Partnership |

Announced expanded Teamplay Digital Health Platform integration with third-party European HIS vendors. |

Accelerates imaging-to-EHR workflow automation across European markets. |

|

Jan 2024 |

Philips Healthcare |

Product Launch |

Launched AI-powered radiology workflow integration module connecting PACS and EHR systems. |

Deepens imaging informatics integration; strengthens Philips in radiology-adjacent HIS. |

|

Sep 2023 |

Athenahealth |

Platform Update |

Expanded athenaOne network intelligence features for ambulatory care revenue cycle optimisation. |

Reinforces Athenahealth position in ambulatory EHR and cloud-native RCM segment. |

|

Nov 2023 |

GE HealthCare |

Partnership |

Extended Edison AI platform partnerships with EHR vendors for care area management data integration. |

Broadens GE HealthCare AI capabilities beyond imaging into operational HIS. |

About Us:

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, the company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is been updated constantly in order to fulfill our clients with prompt and direct online access to our database. Keeping in mind the client’s needs, we have included expert insights on global industries, products, and market trends in this database. Last but not the least, we make it our duty to ensure the success of clients connected to us—after all—if you do well, a little of the light shines on us.

Author:

Mr. Nilesh Patil

Director at Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067