Vietnam Construction Market Size, Growth, Global Trends, Forecast 2034

Vietnam Construction Market By Sector (Residential, Commercial, and Infrastructure), By Construction Type (Renovation and New Construction), By Investment Source (Public and Private)- Country Specific Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

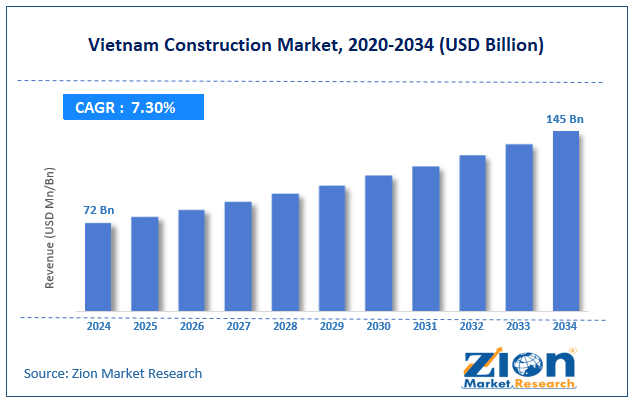

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

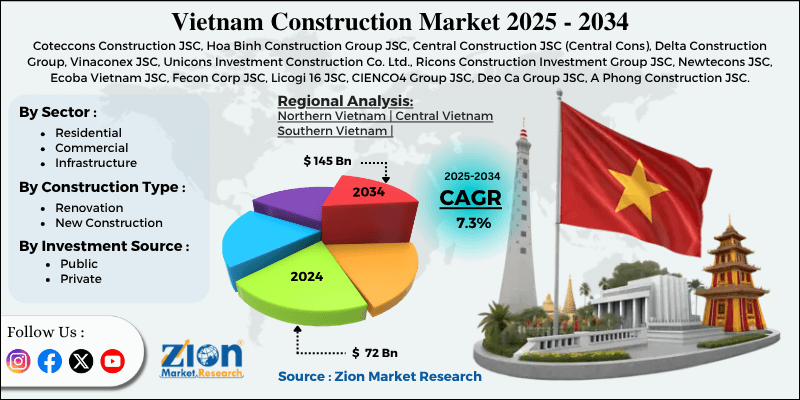

| USD 72 Billion | USD 145 Billion | 7.3% | 2024 |

Vietnam Construction Industry Perspective:

What will be the size of the Vietnam construction market during the forecast period?

The Vietnam construction market size was worth around USD 72 billion in 2024 and is predicted to grow to around USD 145 billion by 2034, with a compound annual growth rate (CAGR) of roughly 7.3% between 2025 and 2034.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Key Insights

- As per the analysis shared by our research analyst, the Vietnam construction market is estimated to grow annually at a CAGR of around 7.3% over the forecast period (2025-2034).

- In terms of revenue, the Vietnam construction market size was valued at around USD 72 billion in 2024 and is projected to reach USD 145 billion by 2034.

- Rising government funding is expected to drive the Vietnam construction market over the forecast period.

- Based on the sector, the residential sector segment holds the largest market share in 2024 of 38%.

- Based on the construction type, the new construction segment held the largest revenue share of over 65% in 2024.

- Based on the investment source, the public segment held the largest revenue share of over 60% in 2024.

Vietnam Construction Market: Overview

Construction is the process of defining, designing, and producing buildings, engineering, and other infrastructure or specialized industrial products. It involves a series of interrelated activities that take raw materials and engineering concepts and transform them into a physical asset, including buildings, roads, dams, airports, and bridges, as well as infrastructure that supplies human needs such as water, power, and gas. The construction industry ranges from civil engineering, architecture, project management, procurement, and skilled trades to organize, coordinate, and control resources to meet the safety, quality, and scheduling expectations of the client. Construction is grouped into segments based on the end use of projects, such as housing, apartments, office blocks, shopping malls, hotels, industrial manufacturing plants, factories, warehouses, and public infrastructure, such as roads, rail, and electricity supply.

Vietnam Construction Market: Dynamics

Growth Drivers

Why does the growing infrastructure development drive growth in the Vietnam construction market?

Across Vietnam, government-led projects are rapidly shifting the country’s mobility and logistics landscape. From investments in expressways to port infrastructure upgrades and rail developments, regional connectivity is being reshaped. Logistics activities in Da Nang, Can Tho, and other cities are on the rise, with clusters of logistics hubs and export zones developing.

For example, in April 2015, the Prime Minister of Vietnam officially inaugurated the construction of 80 major national and development projects. Over USD17.2 billion has been committed to executing the projects. These included 40 transportation projects, 12 civil and industrial construction projects, 12 educational projects, 9 social and cultural projects, 5 public health projects, and 2 irrigation projects. These infrastructure development projects are often backed by tax incentives and long leasing terms, increasingly drawing investments from local as well as international firms, which, in turn, is creating an increased demand for specialized equipment and smarter workflow solutions, thereby strengthening the construction machinery provider market in Vietnam. Foreign investment largely continues to flood into infrastructure and real estate projects. This not only brings investment capital but also new, modern design standards that fuel momentum in green-certified, energy-efficient projects, transforming developers' preferences and building interest in the Vietnam green building market.

Restraints

Labor shortage and workforce issues hamper the industry’s expansion

Labor shortages and workforce issues are predicted to be among the most significant constraints on growth in the construction industry, as they either temporarily or permanently restrict project volumes, escalate costs, and hold up project delivery. There is already a noted deficit of skilled engineers, project managers, operators, electricians, welders, and other skilled trades, which limits productivity and extends delivery timescales.

As an aging workforce retires and less trained and skilled individuals enter the industry, it becomes more difficult to replace technical capabilities, and as a result, projects become less efficient and lower quality. The labor issue also increases subcontracting and, therefore, overall project costs, while delays in delivery can result in initial contract penalties, total cost increases, and harmed developer confidence.

Opportunities

Why do tech integration and digital workflows present a potential opportunity for the Vietnam construction industry growth?

New construction techniques are increasing in purpose and speed, from residential towers in the Capital city to major industrial projects in the south. Digital tools like BIM, digital twins, variable repeatability, and modular construction offer developers a clear advantage in the Vietnam construction market. While smaller developers have been slow to pick up on the new techniques, costs and training are improving. Developers are designing the new-look residential blocks in terms of prioritized layouts, chosen material types, and construction schedules. These improvements are evident in Vietnam's residential development, which is dominated by a pipeline of all ongoing schemes, those under planning, and future schemes. In the coming years, the momentum will persist due to policy stability. Based on recent indicators, the Vietnam construction market in 2024 is set to outperform previous predictions, especially in the Housing and Transport sectors.

Challenges

Why does construction material price volatility pose a major challenge to the Vietnam construction market expansion?

Price fluctuations in construction materials are among the most significant barriers to market growth, affecting the construction industry from financial, project-scheduling, and investor-loyalty perspectives. Construction works involve a long planning process, during which material supplies, costs, and prices are agreed upon at a predetermined scope and at a fixed price. Material price fluctuations have a significant impact on construction costs, pushing the project beyond its profitability threshold and, due to business delays, causing lost time. Materials, which represent the main component of construction costs, such as cement, steel, aluminum, fuels, and electric power, are experiencing fluctuations, causing delays, postponing investments, cutting down the scope of projects, and increasing their complexity.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Vietnam Construction Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Vietnam Construction Market |

| Market Size in 2024 | 72 Billion |

| Market Forecast in 2034 | 145 Billion |

| Growth Rate | CAGR of 7.3% |

| Number of Pages | 223 |

| Key Companies Covered | Coteccons Construction JSC, Hoa Binh Construction Group JSC, Central Construction JSC (Central Cons), Delta Construction Group, Vinaconex JSC, Unicons Investment Construction Co. Ltd., Ricons Construction Investment Group JSC, Newtecons JSC, Ecoba Vietnam JSC, Fecon Corp JSC, Licogi 16 JSC, CIENCO4 Group JSC, Deo Ca Group JSC, A Phong Construction JSC, Phuc Hung Holdings JSC, and others. |

| Segments Covered | By Sector, By Construction Type, By Investment Source, and By Region |

| Regions Covered in Vietnam | Northern Vietnam, Central Vietnam, and Southern Vietnam |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Vietnam Construction Market: Segmentation

By Sector Insights

Why does the residential sector hold the dominant position in the Vietnam construction market?

The residential sector segment holds the largest market share in 2024 of 38%. Vietnam is experiencing rapid urbanization, unlike many other developing countries, and it is expected to have one of the fastest-growing middle classes, with increasing demand for affordable housing, which is the main driver of residential construction in Vietnam. With more and more people seeking jobs in the cities and higher disposable income in the hands of the average Vietnamese, demand for this kind of real estate will be indisputable. The trends in the Vietnam construction market and a positive policy environment encourage their rise. Not only from foreign investors but also from Vietnam, residential construction is the activity in the most well-known sector in real estate construction in Vietnam. Such growth will spur demand for the Vietnam construction materials.

By Construction Type Insights

How is the new construction segment growing significantly in the Vietnam construction industry?

The new construction segment held the largest revenue share of over 65% in 2024. Vietnam’s manufacturing base has attracted strong inflows of FDI, especially in the electronics, textiles, and industrial sectors. This has led to new construction of factories, logistics parks, and warehouses in key industrial provinces. The expansion of industrial parks and export-driven manufacturing is a major driver of revenue growth in new construction.

By Investment Source Insights

Does public funding dominate the Vietnam construction market?

The public segment held the largest revenue share of over 60% in 2024. The main growth engines are large-scale national key infrastructure construction, such as expressways, metro lines, airports, port expansion, and others. The construction of the North-South Expressway and Long Thanh International Airport in the package of the 10th National Party Congress is a huge inflow of State-owned Capital into the Construction Sector, providing high-value contracts and securing high-value revenue in the long term. These projects would also stimulate the demand for materials, engineering services, equipment leasing, and other related services.

Vietnam Construction Market: Competitive Analysis

The Vietnam construction market is dominated by players like:

- Coteccons Construction JSC

- Hoa Binh Construction Group JSC

- Central Construction JSC (Central Cons)

- Delta Construction Group

- Vinaconex JSC

- Unicons Investment Construction Co. Ltd.

- Ricons Construction Investment Group JSC

- Newtecons JSC

- Ecoba Vietnam JSC

- Fecon Corp JSC

- Licogi 16 JSC

- CIENCO4 Group JSC

- Deo Ca Group JSC

- A Phong Construction JSC

- Phuc Hung Holdings JSC

The Vietnam construction market is segmented as follows:

By Sector

- Residential

- Commercial

- Infrastructure

By Construction Type

- Renovation

- New Construction

By Investment Source

- Public

- Private

By Region

- Northern Vietnam

- Central Vietnam

- Southern Vietnam

Table Of Content

Methodology

FrequentlyAsked Questions

HappyClients