North America Anti-Counterfeit Packaging Market Size, Share Report 2034

North America Anti-Counterfeit Packaging Market By Technology (Mass Encoding, RFID, Holograms, Forensic Markers, Tamper Evidence, and Others), By End-Use Industry (Food & Beverages, Pharmaceutical, Apparel & Footwear, Automotive, Personal Care, Electronics & Electrical, Luxury Goods, and Others), and By Region - Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 58.72 Billion | USD 146.74 Billion | 12.13% | 2024 |

North America Anti-Counterfeit Packaging Industry Perspective:

What will be the size of the North America anti-counterfeit packaging market during the forecast period?

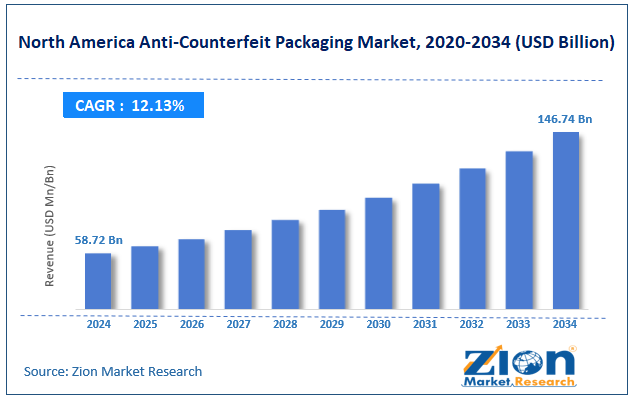

The North America anti-counterfeit packaging market size was around USD 58.72 billion in 2024 and is projected to reach USD 146.74 billion by 2034, with a compound annual growth rate (CAGR) of roughly 12.13% between 2025 and 2034.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Key Insights:

- As per the analysis shared by our research analyst, the North America anti-counterfeit packaging market is estimated to grow annually at a CAGR of around 12.13% over the forecast period (2025-2034)

- In terms of revenue, the North America anti-counterfeit packaging market size was valued at around USD 58.72 billion in 2024 and is projected to reach USD 146.74 billion by 2034.

- The North America anti-counterfeit packaging market is projected to grow significantly owing to strong regulatory and compliance requirements, increasing consumer demand for product authenticity, and supply chain transparency and traceability needs.

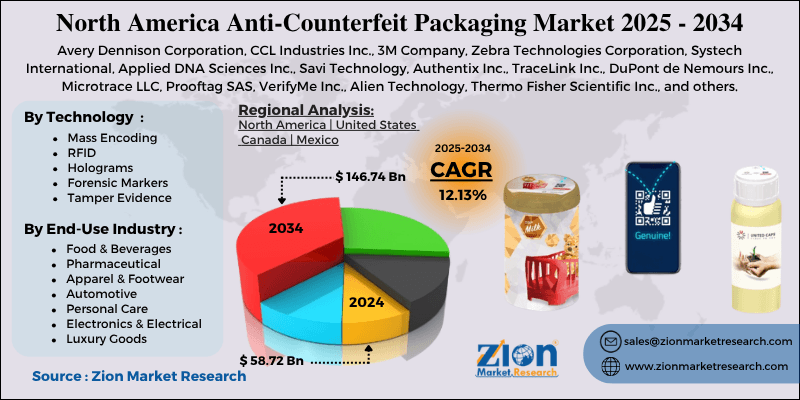

- Based on technology, the mass encoding s segment is expected to lead the market, while the RFID segment is expected to grow considerably.

- Based on end-use industry, the pharmaceutical segment is expected to lead the market, followed by the food & beverages segment.

- By region, the United States is projected to dominate the market during the forecast period, followed by Canada.

North America Anti-Counterfeit Packaging Market: Overview

The North America anti-counterfeit packaging emphasizes integrating technologies such as RFID tags, holograms, and tamper-evident seals to protect products from counterfeiting and ensure supply chain security. Growing consumer awareness, strict regulations, and high-value industries such as electronics, pharmaceuticals, and luxury goods are driving its adoption. The North America anti-counterfeit packaging market is projected to grow substantially, driven by rising counterfeit incidents, stringent regulatory frameworks, and the expansion of e-commerce channels. Counterfeit products in electronics, pharmaceuticals, and luxury goods continue to grow, causing serious financial losses and safety issues. Companies are under increasing pressure to protect both their consumers and revenue from fraudulent items. Anti-counterfeit packaging offers an effective solution to promise product authenticity and secure the supply chain.

Regulatory authorities in the region are enforcing strict guidelines for product safety, anti-tamper measures, and serialization. Manufacturers should comply with these norms to avoid penalties and industry restrictions. This regulatory pressure fuels broader adoption of anti-counterfeit packaging solutions. Furthermore, the rapid expansion of e-commerce has created multiple points of entry where products can be counterfeited or intercepted. As more goods are shipped through complex networks, the risk of tampering increases significantly. Anti-counterfeit packaging solutions help secure online sales and maintain customer trust.

Although drivers exist, the market faces challenges such as a lack of standardization and complex integration requirements. Different industries and regions follow varying anti-counterfeit protocols, creating market fragmentation. Manufacturers face challenges in deploying uniform solutions across all products. Inconsistent standards hamper smooth integration and supply chain security. Likewise, implementing serialization, authentication, and tracking needs overhauling existing IT systems and production lines. These complex integrations demand specialized expertise and extended schedules. Companies may hesitate to adopt due to operational disturbances.

Even so, the North America anti-counterfeit packaging industry is well-positioned by blockchain-based technologies, AI & ML for authentication, and smartphone-enabled consumer solutions. Blockchain technology allows immutable tracking of products from the manufacturer to the end consumer. This promises authenticity, transparency, and traceable proof of ownership. Its adoption can transform consumer trust and supply chain security. AI can monitor supply chains, detect counterfeit threats in real time, and identify anomalies. ML algorithms enhance detection efficiency and reduce manual oversight. This enhances proactive anti-counterfeit measures for brands. Additionally, scanning tools and apps allow consumers to instantly verify product authenticity. This empowers end-users and strengthens engagement with brands. These solutions expand the reach and effectiveness of anti-counterfeit packaging.

North America Anti-Counterfeit Packaging Market: Dynamics

Growth Drivers

How is the North America anti-counterfeit packaging market bolstered by escalating demand in the pharmaceutical and healthcare sectors?

Within the region, the healthcare and pharmaceutical sectors are among the key drivers of demand for anti-counterfeiting packaging. Counterfeit drugs offer severe risks to patient safety, resulting in industry stakeholders and regulators investing heavily in sterilization and track-and-trace technologies. The pharmaceutical segment consistently demonstrates high adoption rates of anti-counterfeiting measures due to product complexity and stringent safety mandates. This growth is mirrored across the wider healthcare supply chain, where secure packaging ensures authenticity from the factory to the pharmacy. The healthcare sector’s prioritization of compliance and patient safety continues to drive substantial growth in the North America anti-counterfeit packaging market.

How are technological improvements in security features significantly fueling the growth of the North America anti-counterfeit packaging market?

Advances in packaging technologies, such as digital watermarks, RFID, smart labels, and blockchain traceability, are enabling stronger authentication and greater supply chain transparency. These advancements make it notably complex for counterfeiters to replicate legitimate products, even with sophisticated tools. Smart packaging also facilitates consumer engagement through real-time tracking and mobile verification, improving brand trust. As technology costs decrease and integration becomes more unified, adoption is expanding into mid-tier product categories. This ongoing advancement cycle continues to stimulate the market growth and diversify security offerings.

Restraints

Limited standardization across industries negatively impacts the market progress

Anti-counterfeit packaging lacks uniform standards in different sectors and industries. Diverse regulatory needs and customer expectations create fragmented solutions. Suppliers cannot always offer universally compatible solutions. Brands may hesitate to adopt solutions that are not broadly recognized. Lack of standardization complicates cross-industry deployment. This ultimately slows consistent adoption and scaling in North America.

Opportunities

How does consumer engagement through digital verification create advantageous conditions for the growth of the North America anti-counterfeit packaging market?

Anti-counterfeit packaging can improve brand engagement through interactive features and mobile verification. Scannable codes can share product information, rewards programs, and origin details. Consumers gain assurance while brands strengthen their reputation and loyalty. Apps and smartphones facilitate broader verification. Engagement-driven packaging combines security with marketing value. This dual utility fuels adoption and innovation in the North America anti-counterfeit packaging industry.

Challenges

Balancing security with sustainability goals restricts the market growth

Brands are under pressure to make their packaging more eco-friendly or recyclable. Some anti-counterfeit technologies, like multi-layer films or RFID chips, conflict with sustainability requirements. Designing secure yet environmentally friendly packaging is technically complex. Companies should meet consumer sustainability and regulatory expectations. Balancing these priorities adds complexity to product development. Security-sustainability trade-offs challenge long-term adoption.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

North America Anti-Counterfeit Packaging Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | North America Anti-Counterfeit Packaging Market |

| Market Size in 2024 | 58.72 Billion |

| Market Forecast in 2034 | 146.74 Billion |

| Growth Rate | CAGR of 12.13% |

| Number of Pages | 230 |

| Key Companies Covered | Avery Dennison Corporation, CCL Industries Inc., 3M Company, Zebra Technologies Corporation, Systech International, Applied DNA Sciences Inc., Savi Technology, Authentix Inc., TraceLink Inc., DuPont de Nemours Inc., Microtrace LLC, Prooftag SAS, VerifyMe Inc., Alien Technology, Thermo Fisher Scientific Inc., and others. |

| Segments Covered | By Technology, By End-Use Industry, and By Region |

| Regions Covered in North America | The U.S., Canada, Mexico, and Rest of North America |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

North America Anti-Counterfeit Packaging Market: Segmentation

The North America anti-counterfeit packaging market is segmented based on technology, end-use industry, and region.

Why is the Mass Encoding segment projected to dominate the North America anti-counterfeit packaging market?

Based on technology, the North America anti-counterfeit packaging industry is divided into mass encoding, RFID, holograms, forensic markers, tamper-evident features, and others. The mass encoding segment leads the market with 38% of the total share. It is widely used via QR codes, barcodes, and unique serial numbers to enable unit-level traceability. It is largely scalable and integrates easily with existing packaging lines in consumer goods, logistics, and pharmaceuticals. The technology promises compliance with regulatory mandates while enhancing product security.

On the other hand, the RFID segment ranks second in the market with over 28% share in North America. It offers real-time tracking, enhanced supply chain visibility, and automated authentication. It is primarily used in electronics, healthcare, and luxury goods for connected, smart packaging solutions. The technology reduces manual scanning, enhances inventory accuracy, and strengthens anti-counterfeit measures.

What are the key reasons for the leadership of the Pharmaceutical segment in the North America anti-counterfeit packaging market?

Based on end-use industry, the North America anti-counterfeit packaging market is segmented into food & beverages, pharmaceutical, apparel & footwear, automotive, personal care, electronics & electrical, luxury goods, and others. The pharmaceutical segment accounts for over 40% of total market share due to strict regulatory mandates, such as the DSCSA, that require traceability, anti-tamper solutions, and serialization. The segment addresses critical safety concerns and combats high levels of drug counterfeiting, which poses legal and health risks.

However, the food & beverage segment holds the second-largest market share, with approximately 25%, as it faces growing challenges from adulteration, food fraud, and labeling misrepresentation. Secure packaging improves traceability, regulatory compliance, and safety assurance, which are increasingly demanded by authorities and consumers. Food & beverage ranks second after pharmaceuticals in the regional market.

North America Anti-Counterfeit Packaging Market: Regional Analysis

What enables the United States strong foothold in the North America Anti-Counterfeit Packaging Market?

The United States is likely to sustain its leadership in the North America anti-counterfeit packaging market, with a 10.1% CAGR, driven by strong regulatory frameworks, a large pharmaceutical and healthcare sector, and advanced technological infrastructure. The United States has strict regulations, such as trace-and-trace requirements and sterilization, primarily in the food and pharmaceutical sectors. These norms compel manufacturers to adopt advanced anti-counterfeit packaging solutions. Regulatory enforcement promises broader, more consistent implementation across industries. Moreover, the U.S. is home to the world's leading pharmaceutical markets, which are highly vulnerable to counterfeiting. This fuels major demand for traceable, secure, and tamper-evident packaging. High compliance requirements further accelerate the adoption of advanced technologies.

Furthermore, the country benefits from well-developed technological and digital ecosystems supporting blockchain, RFID, and smart packaging. Companies can easily integrate anti-counterfeiting solutions into existing supply chains. This technological readiness improves industry growth and advancements.

Why does Canada rank second in the North America anti-counterfeit packaging Market?

Canada continues to hold the second-highest share, with a 9.1% CAGR in the North America anti-counterfeit packaging industry, owing to strong pharmaceutical and healthcare standards, growing focus on traceability and food safety, and technological adoption and innovation. Canada’s healthcare system prioritizes authenticity and drug safety, driving demand for secure packaging. Pharmaceutical companies adopt sterilization and tamper-evident solutions to prevent counterfeit drugs. This reinforces the role of anti-counterfeit technologies in the sector. Growing concerns about contamination and food fraud push Canadian companies to adopt secure packaging solutions. Anti-counterfeit technologies help ensure product quality and authenticity. This improves regulatory compliance and consumer trust.

Additionally, Canada is actively investing in advanced technologies such as QR codes, RFID, and blockchain to enhance supply chain transparency. Businesses are adopting smart packaging solutions to enhance authentication and tracking. This technological shift supports industry growth.

North America Anti-Counterfeit Packaging Market: Competitive Analysis

The leading players in the North America anti-counterfeit packaging market are:

- Avery Dennison Corporation

- CCL Industries Inc.

- 3M Company

- Zebra Technologies Corporation

- Systech International

- Applied DNA Sciences Inc.

- Savi Technology

- Authentix Inc.

- TraceLink Inc.

- DuPont de Nemours Inc.

- Microtrace LLC

- Prooftag SAS

- VerifyMe Inc.

- Alien Technology

- Thermo Fisher Scientific Inc.

What are the key trends in the North America anti-counterfeit packaging Market?

Integration of smart packaging technologies:

Smart packaging using NFC, QR codes, and RFID is increasingly being implemented for real-time authentication. These solutions improve inventory management, customer engagement, and anti-counterfeiting protection. The shift toward connected packaging is transforming traditional packaging into digital security tools.

Growth of e-commerce and supply chain transparency needs:

The rapid growth of e-commerce has increased the risk of counterfeit infiltration into distribution networks. Companies are adopting secure packaging to ensure authenticity during shipping and delivery. This trend focuses on traceability, transparency, and consumer trust in diverse online channels.

The North America anti-counterfeit packaging market is segmented as follows:

By Technology

- Mass Encoding

- RFID

- Holograms

- Forensic Markers

- Tamper Evidence

- Others

By End-Use Industry

- Food & Beverages

- Pharmaceutical

- Apparel & Footwear

- Automotive

- Personal Care

- Electronics & Electrical

- Luxury Goods

- Others

By Region

- North America

- United States

- Canada

- Mexico

Table Of Content

Methodology

FrequentlyAsked Questions

The North America anti-counterfeit packaging market emphasizes integrating technologies such as RFID tags, holograms, and tamper-evident seals to protect products from counterfeiting and ensure supply chain security. Growing consumer awareness, strict regulations, and high-value industries such as electronics, pharmaceuticals, and luxury goods are driving its adoption.

The North America anti-counterfeit packaging market is projected to grow due to the rising incidence of product counterfeiting, the growth of e commerce and online marketplaces, and the expansion of pharmaceutical and healthcare packaging.

According to a study, the North America anti-counterfeit packaging market size was around USD 58.72 billion in 2024 and is expected to grow to around USD 146.74 billion by 2034.

What will be the CAGR value of the North America anti-counterfeit packaging market during 2025-2034?

The CAGR value of the North America anti-counterfeit packaging market is expected to be around 12.13% during 2025-2034.

Emerging trends and innovations include AI driven authentication, blockchain enabled traceability, smart packaging with NFC/RFID, sustainable security materials, and consumer centric mobile verification tools.

The North America anti-counterfeit packaging market has grown steadily due to regulatory compliance and rising counterfeiting concerns, and is expected to expand further with the adoption of smart packaging technologies and increased traceability.

The key players profiled in the North America anti-counterfeit packaging market include Avery Dennison Corporation, CCL Industries Inc., 3M Company, Zebra Technologies Corporation, Systech International, Applied DNA Sciences Inc., Savi Technology, Authentix Inc., TraceLink Inc., DuPont de Nemours Inc., Microtrace LLC, Prooftag SAS, VerifyMe, Inc., Alien Technology, and Thermo Fisher Scientific Inc.

Stakeholders should focus on supply chain traceability, advanced technologies, consumer authentication, strategic partnerships, and sustainable packaging to stay competitive in the North America anti-counterfeit packaging market.

Key opportunities include investing in smart packaging and blockchain technologies, partnering with supply chain stakeholders and tech providers, and collaborating with regulatory bodies to improve anti counterfeit solutions.

The report examines key aspects of the North America anti-counterfeit packaging market, including a detailed analysis of current growth factors and restraints, as well as future growth opportunities and challenges that will impact the market.

List of Contents

North America Anti-Counterfeit PackagingIndustry Perspective:Key Insights:OverviewDynamicsReport ScopeSegmentationRegional AnalysisCompetitive AnalysisWhat are the key trends in the North America anti-counterfeit packaging Market?The North America anti-counterfeit packaging market is segmented as follows:HappyClients