Nanomedicine Market Size, Share, Trends & Forecast 2026–2034

Global Nanomedicine Market — By Type (Nanoparticles, Nanoshells, Nanotubes, Nanodevices), By Application (Drug Delivery, Therapeutics, Diagnostics, Regenerative Medicine), By Indication (Oncology, Cardiovascular Diseases, Infectious Diseases, Neurological Disorders, Others), By End User (Hospitals & Clinics, Pharmaceutical & Biotechnology Companies, Research & Academic Institutes, Diagnostic Laboratories), and By Region — Global Industry Perspective, Data, Market Intelligence, Opportunity Analysis, and Forecast, 2026–2034.-

| Market Size in 2025 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 16,840 Million | USD 84,320 Million | 19.5% | 2025 |

Nanomedicine Market: Industry Perspective

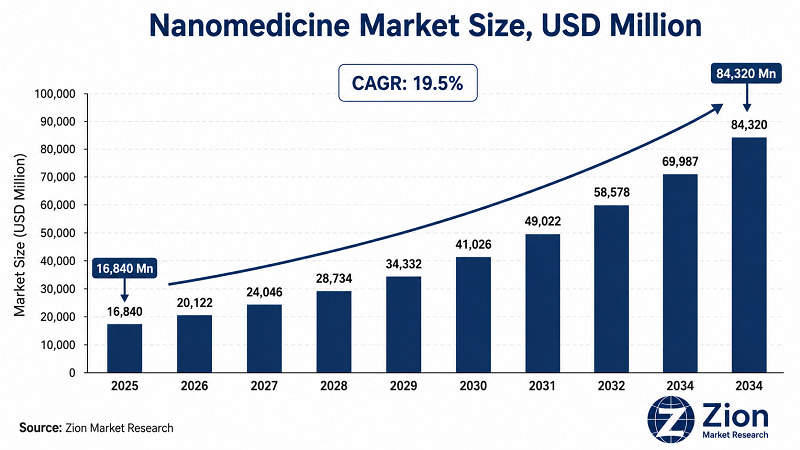

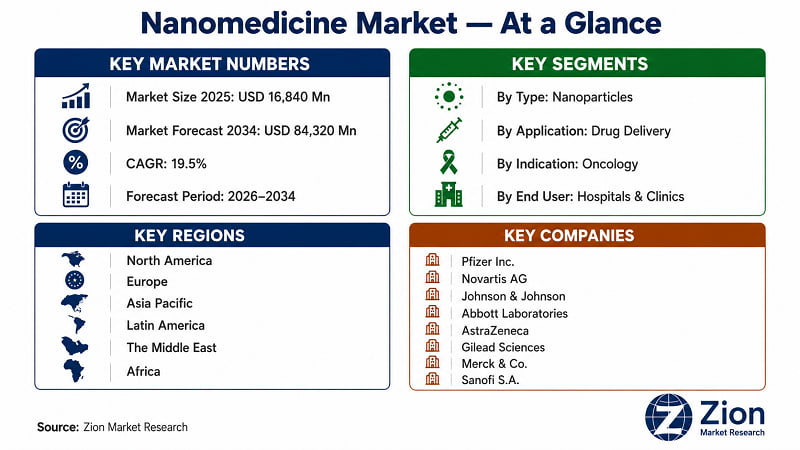

- The Global Nanomedicine market is undergoing a structural inflection. At USD 16,840 Million in 2025 — with a trajectory to USD 84,320 Million by 2034 at a 19.5% CAGR — this market's growth rate is not a product of incremental pharmaceutical improvement. It reflects a platform-level shift in therapeutic design.

- The question for decision-makers is not whether the market expands but where within the value chain disproportionate returns will concentrate — and which segment-geography combinations generate outsized volume-value splits over the forecast horizon 2026–2034.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Nanomedicine Market: Overview

- Nanomedicine encompasses the design, synthesis, characterisation, and clinical application of materials and devices operating at the 1–100 nanometre scale for medical purposes. The market includes nanoparticle-based drug delivery systems (liposomes, LNPs, polymeric nanoparticles), nanoshell and nanotube platforms, nanodevices for in vivo sensing and targeted therapy, and diagnostic nanomaterials for imaging and biomarker detection. Indications span oncology, cardiovascular disease, neurological disorders, infectious diseases, and regenerative medicine.

- The nanomedicine value chain operates across three distinct tiers. Foundational providers — including BASF SE (Germany) for nanomaterial synthesis and Evonik Industries AG (Germany) for excipient supply — provide the raw material and chemistry infrastructure layer. Specialist developers — including Nanoform Finland Plc and Nanobiotix S.A. (France) — translate material platforms into pharmaceutical formulations and clinical-stage products. Application-layer specialists — including Pfizer Inc. (U.S.), Alnylam Pharmaceuticals Inc. (U.S.), and Moderna Inc. (U.S.) — own the commercial products that reach patients and generate the majority of market revenue.

- For procurement and investment decision-makers, the distinction that matters is not whether Nanomedicine will grow — that question is settled — but which segments, geographies, and deployment models will capture disproportionate value within that growth. This report provides sub-segment level data, country-level forecasts, and competitive positioning analysis across 4 segmentation dimensions and 35+ geographies.

Key Insights

- The Global Nanomedicine market expands at a 19.5% CAGR from 2026 to 2034, reaching USD 84,320 Million — among the fastest compounding rates in the pharmaceutical sector (Zion Market Research, 2026).

- Nanoparticles dominate by molecule type with an estimated 76% market share in 2025, driven by versatility across both therapeutic and diagnostic delivery platforms.

- Lipid nanoparticles (LNPs) are the fastest-growing nanoparticle sub-type, accelerating at CAGR above 22% through 2034, following commercial validation by mRNA COVID-19 vaccine platforms.

- Drug Delivery is the dominant application with an estimated 34–35% share in 2025, reflecting pharmaceutical-industry demand for targeted API delivery over systemic administration.

- Oncology is the lead indication, accounting for the largest clinical nanomedicine pipeline globally, with 40+ late-stage nanoparticle candidates in active trials as of 2025.

- Hospitals & Clinics lead end-user adoption as the primary procurement and administration point for approved nanomedicines.

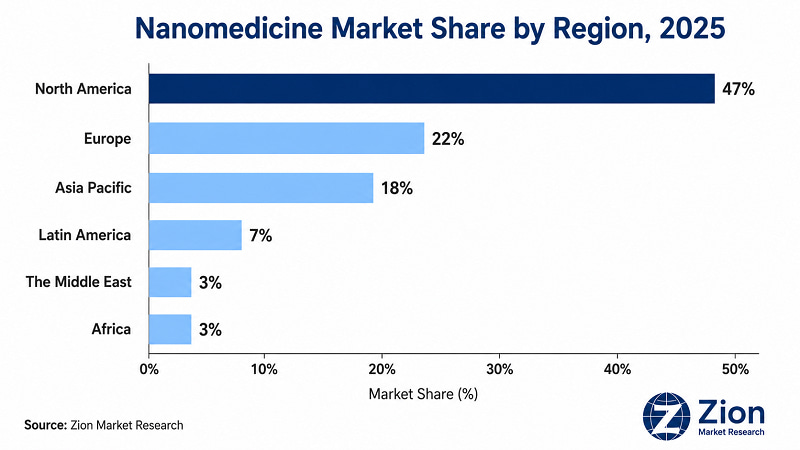

- North America holds ~47% of global Nanomedicine revenue in 2025; Asia Pacific grows fastest at a projected CAGR above 20% through 2034.

- Competitive intensity is rising at the platform level: LNP, polymeric nanoparticle, and siRNA-delivery platforms are the primary battlegrounds, not individual products.

- AI-integrated nanoparticle design — using machine learning to predict drug-nanoparticle interactions and optimise formulation stability — is emerging as a material differentiator in pipeline development speed through the forecast period.

Why Choose the Zion Market Research's Nanomedicine Market Report?

Decision-makers comparing market intelligence reports on Nanomedicine will find the Zion Market Research's report differentiated on the following dimensions.

|

DIMENSION |

ZION MARKET RESEARCH REPORT |

INDUSTRY AVERAGE |

|

Report Pages |

300+ |

~120 pages |

|

Forecast Horizon |

9 years (2026–2034) |

7 years |

|

Segmentation Dims |

4 dimensions |

4–5 dimensions |

|

Historical Data |

6 years (2019–2024) |

4–5 years |

|

Country Coverage |

35+ countries |

15–18 countries |

|

Companies Profiled |

15 companies |

10 companies |

|

DROC Framework |

Full (Drivers, Restraints, Opportunities, Challenges) |

Drivers only |

**For custom scope — additional segments, specific geographies, or extended forecast periods — contact sales@zionmarketresearch.com

Nanomedicine Market: Dynamics (Drivers, Restraints, Opportunities, Challenges)

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

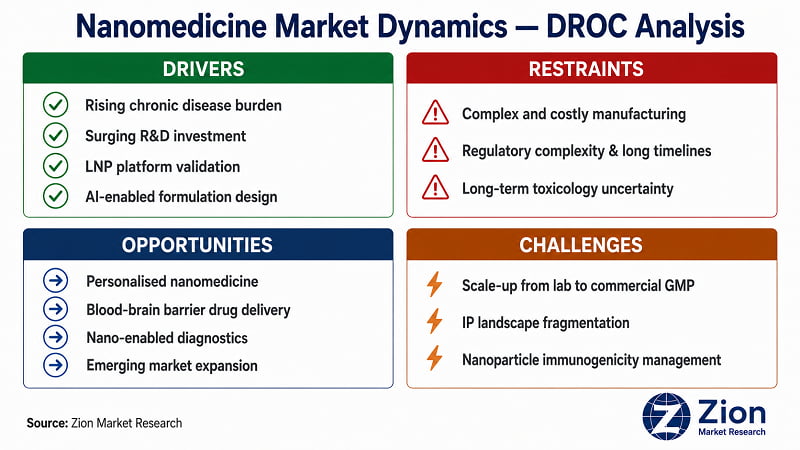

What Is Driving the Nanomedicine Market?

- Rising Prevalence of Chronic Diseases and Unmet Therapeutic Need:

The global burden of cancer, cardiovascular disease, and neurological disorders is growing at a pace that conventional small-molecule and biologics-based therapeutics cannot adequately address in terms of targeting precision, toxicity management, or blood-brain barrier penetration. The American Cancer Society projected 238,000 new lung cancer diagnoses in the U.S. in 2023 alone. Each of these cases represents a patient population where nanoparticle-based targeted delivery demonstrably outperforms systemic chemotherapy on both efficacy and tolerability metrics. The NIH's 2024 report on nanotechnology confirms that nanoparticle platforms improve drug bioavailability, reduce off-target toxicity, and enable controlled release — directly addressing the three central weaknesses of conventional therapy. The University of Chicago Medicine Comprehensive Cancer Center demonstrated this in September 2024, developing a nanomedicine that enhances chemotherapy drug penetration in tumour tissue by activating the STING pathway — producing measurable gains in tumour targeting without systemic toxicity escalation. This clinical evidence cycle accelerates formulary adoption across hospital systems.

- Surge in R&D Investment and Government-Backed Nanotechnology Infrastructure:

Capital flowing into nanomedicine R&D has reached levels that compress development timelines and accelerate clinical translation. The U.S. National Science Foundation committed USD 84 million over five years to re-establish the National Nanotechnology Coordinated Infrastructure — providing shared instrumentation and research capacity that reduces the per-experiment cost for nanoparticle characterisation. Novartis announced in April 2025 plans to invest USD 23 billion over five years in U.S. manufacturing and R&D, explicitly including advanced drug delivery systems and nanoformulation platforms. The Canadian government's investment of more than USD 640 million in nanotechnology research across the past decade has built a parallel capacity base in North America. In Asia Pacific, India's Department of Science and Technology funds a dedicated NanoMission for pharmaceutical nanotechnology development. This compounding capital cycle is pulling 40+ late-stage nanoparticle candidates through clinical trial phases at a pace the sector has not previously achieved.

- LNP Platform Validation and Post-COVID Regulatory Tailwinds:

The regulatory validation of lipid nanoparticle (LNP) platforms through Pfizer-BioNTech's Comirnaty and Moderna's Spikevax — both approved within 12 months of emergency use authorisation in 2021 — created a landmark shift in FDA institutional confidence around nanoparticle safety characterisation. The FDA's Nanotechnology Working Group has since developed guidance on nanoparticle drug product characterisation, providing structured approval pathways that reduce regulatory uncertainty for new entrants. This framework directly lowers barriers for non-vaccine nanomedicine INDs. AstraZeneca deployed this regulatory momentum in Q2 2024, announcing a partnership with Silence Therapeutics to develop RNAi nanomedicines for cardiovascular, renal, and metabolic diseases — demonstrating LNP applications beyond oncology and vaccines.

- AI Integration in Nanoparticle Design and Formulation Optimisation:

Artificial intelligence is materially shortening nanomedicine development cycles. Machine learning models trained on physicochemical datasets can predict drug-nanoparticle interactions, immune system responses, vascular biodistribution, and cell membrane permeability — parameters that previously required months of iterative laboratory work per formulation candidate. Major pharmaceutical companies are deploying AI-driven formulation screening tools: Nanoform Finland Plc announced in April 2024 a strategic partnership with CBC Co., Ltd. to deploy Nanoform's AI-assisted nanomedicine engineering technology in the Japanese pharmaceutical market, targeting formulation optimisation at scale. AI-driven design does not replace GMP manufacturing capability, but it meaningfully reduces the volume-value split between failed and successful formulation candidates reaching late-stage trials.

|

"Nanoparticle platforms allow us to approach therapeutic design from the target backward. We identify the biological barrier or delivery challenge first, then engineer the nanoparticle system to address it precisely. This inverts the conventional small-molecule discovery model and opens therapeutic space that was previously inaccessible." — Senior Pharmaceutical R&D Executive (Buyer-Side Organisation, paraphrased from industry conference) — Annual Pharmaceutical Innovation Forum, 2024 (Source: Annual Pharmaceutical Innovation Forum Proceedings, 2024) |

What Is Restraining the Nanomedicine Market?

- Complex and Costly Manufacturing Scale-Up:

Nanoparticle synthesis at GMP scale demands microfluidic production systems, dedicated cleanroom infrastructure, and particle characterisation equipment (dynamic light scattering, electron microscopy, zeta potential analysers) that carry capital costs of USD 5–20 million per production line. Cost per gram for nanoparticle formulation remains 3–5x higher than equivalent small-molecule APIs, creating structural margin pressure on commercialisation economics — particularly in price-sensitive markets in Latin America and Africa where cost-competitiveness determines market penetration timelines. The gap between lab-scale synthesis (milligram quantities) and commercial-scale manufacturing (kilogram quantities) remains one of the most persistent supply-side headwinds in the sector. This restraint is most acutely felt in the Asia Pacific region, where manufacturing capacity is building but has not yet reached the volumes needed to support global commercial supply chains.

- Regulatory Complexity and Multi-Jurisdictional Approval Divergence:

Despite the FDA's post-COVID nanoparticle guidance progress, global regulatory fragmentation remains a material restraint. The European Medicines Agency (EMA) and FDA have not fully harmonised nanoparticle characterisation requirements for marketing authorisation applications — creating a scenario where a nanomedicine product may require separate pharmacokinetic and immunogenicity studies for U.S. and EU submissions. Japan's PMDA and China's NMPA maintain additional nanoparticle-specific requirements that further extend multi-market approval timelines by 12–24 months beyond single-jurisdiction filing. Regulatory uncertainty is most pronounced in the nanodevice and nanotube sub-segments, where characterisation standards are less established than for liposomal and LNP products. This divergence disproportionately impacts small and mid-size nanotech developers who lack the regulatory infrastructure to manage simultaneous multi-jurisdiction submissions.

- Safety and Long-Term Toxicology Data Gaps:

For novel nanoplatforms beyond the established liposomal and LNP product classes, long-term biodistribution data, chronic toxicity profiles, and immunogenicity characterisation remain incomplete at the clinical trial evidence level. Investor and payer confidence is consequently lower for nanotubes, nanodevices, and novel inorganic nanoparticle systems than for LNP and liposomal products where decades of clinical data exist. This creates a capital allocation bias toward LNP and polymeric nanoparticles at the expense of potentially higher-value novel platforms, slowing category-level market diversification.

|

"The manufacturing translation challenge for nanomedicine is fundamentally different from small-molecule or even antibody manufacturing. The physical properties of nanoparticles — size, surface charge, encapsulation efficiency — are exquisitely sensitive to process parameters. Achieving consistent, reproducible batches at commercial scale is not a linear extrapolation from lab results. It requires dedicated process development investment that many academic spinouts are not equipped to fund." — Jeremie Trochu, CEO — Ardena (Belgium) (Source: Ardena Press Release on GMP Approval, 2024) |

What Opportunities Exist in the Nanomedicine Market?

- Personalised Nanomedicine and Precision Therapeutics:

The convergence of nanomedicine with genomic data, AI-based biomarker analysis, and patient-specific tumour profiling creates a commercial pathway for personalised nanoparticle therapeutics that deliver APIs calibrated to an individual patient's disease biology. Satio and Nanowear's April 2025 collaboration — integrating Nanowear's AI-based nanotechnology biomarker diagnostic platform with Satio's home-based drug delivery systems — demonstrates a viable commercial model for personalised nanomedicine outside hospital settings. This opportunity is particularly strong in oncology and rare neurological disease, where therapeutic windows are narrow and patient heterogeneity is high. The global personalised medicine market provides a structural growth floor for personalised nanomedicine applications.

- Blood-Brain Barrier (BBB) Drug Delivery:

Neurological disorders represent one of the most commercially underserved therapeutic areas in conventional pharmaceutical development — primarily because the blood-brain barrier blocks 98% of small-molecule drugs and all large-molecule biologics from reaching CNS targets. Nanoparticles engineered with appropriate surface ligands and sizes below 200 nm can traverse the BBB through receptor-mediated transcytosis, unlocking therapeutic access to Alzheimer's disease, Parkinson's disease, and glioblastoma populations with currently no effective disease-modifying treatment options. The global Alzheimer's drug pipeline has seen multiple clinical failures at conventional formulation stage; nano-enabled CNS delivery is now a primary reformulation strategy for late-stage R&D programmes.

- Nano-Enabled In Vitro Diagnostics (IVD) and Point-of-Care Testing:

The diagnostic application of nanomedicine — particularly gold nanoparticle-based lateral flow assays, quantum dot imaging agents, and nano-biosensor platforms — is expanding beyond oncology biomarker detection into infectious disease, cardiovascular risk assessment, and metabolic disorder monitoring. The COVID-19 lateral flow test market demonstrated global demand for rapid, nano-enabled diagnostics at scale. Post-pandemic, this manufacturing and distribution infrastructure is being repurposed for multiplexed diagnostic panels. Point-of-care diagnostic applications carry lower regulatory barriers than therapeutic nanomedicines, offering faster time-to-revenue for nanotech developers with diagnostic platform capabilities.

- Emerging Market Penetration via Affordable Nanoformulation:

Asia Pacific, Latin America, The Middle East, and Africa collectively represent underpenetrated market opportunity for nanomedicine. Government investment in nanotechnology infrastructure in India (NanoMission), China (National Nanotechnology Initiative), and Brazil is building local manufacturing and research capacity that reduces import dependence and enables regionally appropriate pricing models. The University of Texas Rio Grande Valley received a USD 2.8 million CPRIT grant in June 2025 to establish a Drug Delivery and Nanomedicine research centre — a pattern being replicated in government-funded research institutions across emerging market economies. Affordable polymer-based nanoparticle generics represent an actionable go-to-market strategy for emerging market entry.

What Challenges Does the Nanomedicine Market Face?

- Scale-Up from Laboratory to Commercial GMP Manufacturing:

The physicochemical properties of nanoparticles — particle size distribution, polydispersity index, zeta potential, encapsulation efficiency — are sensitive to batch size, mixing dynamics, and equipment geometry in ways that small-molecule API manufacturing is not. A formulation validated at 100 mL laboratory scale may exhibit measurably different properties at 100 L GMP scale, requiring complete reformulation and re-validation. This reproducibility challenge is the single most common cause of nanomedicine clinical development delays beyond Phase I, and it remains unsolved without bespoke process engineering investment for each nanoplatform.

- Intellectual Property Landscape Fragmentation:

The nanomedicine IP landscape is characterised by patent thickets — overlapping claims on nanoparticle composition, surface modification, drug loading methodology, and manufacturing process — that create freedom-to-operate uncertainty for new market entrants. Large-cap pharmaceutical companies hold broad composition-of-matter patents on LNP formulations that effectively licence-gate the technology for smaller developers. Litigation risk associated with LNP IP is demonstrated by the Moderna–Alnylam and Moderna–Arbutus disputes, which have created precedent uncertainty that deters early-stage investment in adjacent nanoparticle platforms.

- Nanoparticle Immunogenicity and Patient Safety Monitoring:

Nanoparticles interact with the immune system in ways that vary by particle surface chemistry, size, and the patient's immunological profile. Complement activation-related pseudoallergy (CARPA) — an acute immune response triggered by nanoparticles — has caused product recalls and label restrictions for liposomal products. Managing immunogenicity across diverse patient populations, particularly in immunocompromised oncology patients, requires post-market surveillance infrastructure that adds to commercialisation cost and creates ongoing product liability exposure.

Nanomedicine Market: Report Scope

|

PARAMETER |

DETAILS |

|

Report Name |

Global Nanomedicine Market Size, Share, Trends & Forecast 2026–2034 |

|

Market Size in 2025 |

USD 16,840 Million |

|

Market Forecast in 2034 |

USD 84,320 Million |

|

Growth Rate (CAGR) |

19.5% (2026–2034) |

|

Historical Data Period |

2019–2024 |

|

Base Year |

2025 |

|

Forecast Period |

2026–2034 |

|

Number of Pages |

300+ |

|

Tables & Figures |

110–140 tables | 80–100 figures |

|

Report Code |

ZMR-10567 |

|

Report Format |

|

|

Delivery Format |

Electronic (PDF download) |

|

Published Date |

May 2026 |

|

Research Methodology |

Primary Research (interviews, surveys) + Secondary Research (company filings, regulatory databases, peer-reviewed literature) |

|

Key Companies Covered |

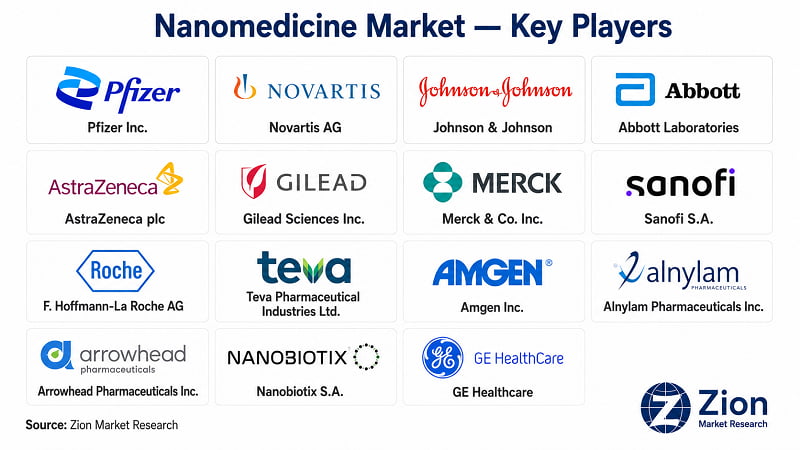

Pfizer Inc., Novartis AG, Johnson & Johnson, Abbott Laboratories, AstraZeneca plc, Gilead Sciences Inc., Merck & Co. Inc., Sanofi S.A., F. Hoffmann-La Roche AG, Teva Pharmaceutical Industries Ltd., Amgen Inc., Alnylam Pharmaceuticals Inc., Arrowhead Pharmaceuticals Inc., Nanobiotix S.A., GE Healthcare |

|

Segments Covered |

By Type | By Application | By Indication | By End User |

|

Regions Covered |

North America | Europe | Asia Pacific | Latin America | The Middle East | Africa |

|

Customization Scope |

Available — contact sales@zionmarketresearch.com for custom segments, geographies, or extended forecast periods |

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Nanomedicine Market: Segmentation

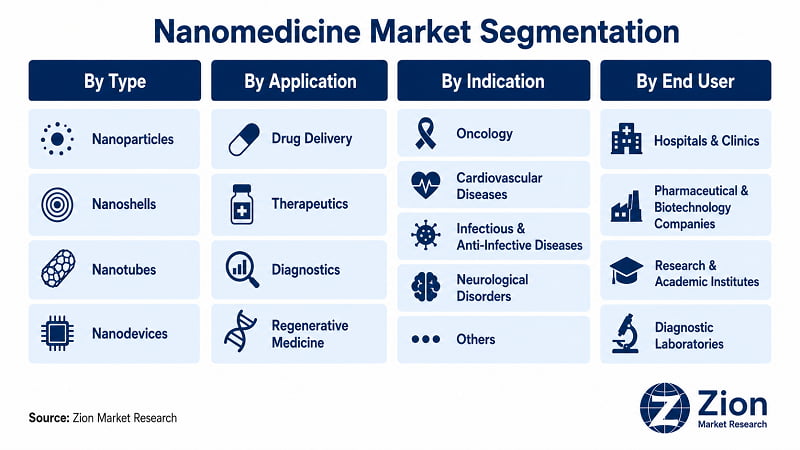

The Global Nanomedicine market is segmented by type, application, indication, and end user.

- By Type

Sub-segments include Nanoparticles, Nanoshells, Nanotubes, and Nanodevices. Nanoparticles dominate with an estimated 76% share in 2025, underpinned by their versatility across lipid-based, polymeric, and inorganic sub-types. Lipid nanoparticles (LNPs) represent the dominant and fastest-growing nanoparticle sub-class, commercially validated through Pfizer-BioNTech's Comirnaty and Moderna's Spikevax vaccines and rapidly expanding into therapeutic oncology, RNAi therapeutics, and gene therapy delivery. Nanotubes — particularly carbon nanotubes — are the fastest-growing alternative type, driven by research activity in CNS drug delivery and biosensing applications, though they remain predominantly pre-commercial. Alnylam Pharmaceuticals' Onpattro (patisiran) — the first FDA-approved RNAi therapeutic delivered via LNP — remains the most commercially significant single-product example of nanoparticle dominance.

- By Application

Sub-segments cover Drug Delivery, Therapeutics, Diagnostics, and Regenerative Medicine. Drug Delivery commands the largest application share at approximately 34–35% in 2025, driven by pharmaceutical-industry adoption of nanoparticle encapsulation to solve API bioavailability challenges across oncology, CNS, and cardiovascular indications. Therapeutics — the second-largest application — is the fastest-growing, projected to outpace Drug Delivery growth through 2034 as nanoparticle-based gene therapy, siRNA, and mRNA therapeutic candidates advance through late-stage trials. Diagnostics is a high-value and growing sub-segment, with nanomaterial-enhanced imaging agents and point-of-care biosensors expanding the diagnostic application base. GE Healthcare (U.S.) maintains a leading diagnostic nanomedicine position through its nanoparticle-enhanced MRI contrast agent portfolio.

- By Indication

Sub-segments include Oncology, Cardiovascular Diseases, Infectious & Anti-Infective Diseases, Neurological Disorders, and Others (including Orthopaedic & Regenerative, Urological, Ophthalmological, and Immunological disorders). Oncology leads with an estimated 32–35% indication share in 2025, driven by the largest clinical pipeline of nanoparticle therapeutics globally and the clearest evidence base for targeted delivery benefit over systemic chemotherapy. Neurological Disorders is the fastest-growing indication segment, driven by the blood-brain barrier penetration opportunity and the complete absence of disease-modifying therapies for Alzheimer's and Parkinson's disease using conventional formulations. Nanobiotix's NBTXR3 — advancing through Phase 3 trials in head and neck cancer — represents the most advanced non-LNP nanoparticle therapeutic in late-stage clinical development.

- By End User

Sub-segments cover Hospitals & Clinics, Pharmaceutical & Biotechnology Companies, Research & Academic Institutes, and Diagnostic Laboratories. Hospitals & Clinics lead end-user adoption as the primary procurement and administration channel for approved nanomedicines — particularly oncology infusion products and diagnostic imaging agents. Pharmaceutical & Biotechnology Companies represent the largest investment and pipeline development end-user category, driving the commercial R&D cycle. Research & Academic Institutes are the fastest-growing end-user segment by engagement volume, fed by government nanotechnology infrastructure investment and academic spinout activity.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Nanomedicine Market: Regional Analysis

North America leads the Global Nanomedicine market with an estimated 46–50% revenue share in 2025, anchored by NIH-funded research infrastructure, FDA regulatory support, and the concentration of major pharmaceutical and biotech companies. Asia Pacific is the fastest-growing region, with government-led nanotechnology investment in China, Japan, and India accelerating clinical translation and manufacturing capacity build-out.

-

North America Nanomedicine Market

North America holds the dominant global position in Nanomedicine, driven by the U.S. which accounts for approximately 92–93% of regional revenue. The NIH allocates more than USD 2 billion annually to nanotechnology and nanomedicine research, with cancer nanomedicine receiving the largest share through the National Cancer Institute. The FDA's Nanotechnology Working Group has published guidance on nanoparticle drug product characterisation, providing a structured approval pathway that reduces clinical development risk for U.S. market entrants. The presence of Pfizer, Merck, Johnson & Johnson, Abbott, and Alnylam — alongside a deep biotech ecosystem of nanotech startups — creates a complete commercial ecosystem from raw material supply through clinical-stage development to commercial distribution. Canada contributes through government investment exceeding USD 640 million over the past decade. One challenge specific to North America is growing IP litigation risk around LNP platform patents, which creates freedom-to-operate costs for smaller nanotech developers.

-

Europe Nanomedicine Market

Europe is a strong second-place market, supported by the European Medicines Agency's regulatory framework and a well-developed pharmaceutical R&D cluster across Germany, the U.K., France, and Switzerland. Germany hosts major nanomedicine research institutions and Evonik Industries — a global excipient supplier critical to LNP manufacturing. The U.K.'s Medicines and Healthcare products Regulatory Agency (MHRA) has adopted post-Brexit nanomedicine-specific guidance aligned with but distinct from EMA standards, creating a dual-submission requirement for companies seeking simultaneous EU and UK market access. France's Nanobiotix S.A. and Switzerland's Novartis and Roche represent Europe's strongest commercial nanomedicine presences. The European Commission's Horizon Europe programme funds nanomedicine research across member states. Sweden and the Netherlands (BENELUX) are emerging as strong clinical trial hubs for nanomedicine Phase 1/2 studies.

-

Asia Pacific Nanomedicine Market

Asia Pacific is the highest-growth region in Nanomedicine globally, projected to expand at a CAGR above 20% through 2034. China's National Nanotechnology Initiative and NMPA regulatory development are the primary growth engines, with domestic pharmaceutical companies building nanoparticle formulation capabilities to reduce dependence on imported nanomedicine products. Japan's established pharmaceutical manufacturing base — with Fujifilm Holdings, Nanoform's CBC partnership, and Takeda Pharmaceutical's oncology pipeline — anchors the region's commercial segment. India's NanoMission, coordinated by the Department of Science and Technology, is supporting nanoparticle research at IITs and CSIR laboratories. South Korea's Samsung Biologics and domestic biotech companies are advancing nano-enabled biologics delivery. Australia is an active clinical trial market for nanomedicine Phase 1–2 oncology studies. The key challenge in Asia Pacific is IP enforcement divergence, which creates technology transfer risk for nanomedicine platform licensors.

-

Latin America Nanomedicine Market

Brazil leads the Latin America Nanomedicine market, accounting for the majority of regional revenue through a combination of public hospital procurement, government-funded nanotechnology research at FAPESP, and a growing domestic biotech sector. Argentina and Colombia are secondary contributors, with clinical trial activity expanding for oncology nanomedicines. The University of Texas Rio Grande Valley's June 2025 USD 2.8 million grant to establish a Drug Delivery and Nanomedicine centre — serving the U.S.-Mexico border population — reflects the cross-border nanomedicine access dynamic relevant to Latin America. The primary restraint is cost sensitivity: GMP-manufactured nanomedicines carry price points that challenge reimbursement systems in government-dominated healthcare markets. Generic liposomal products from Teva Pharmaceutical represent the most commercially accessible nanomedicine format for Latin American procurement.

-

The Middle East Nanomedicine Market

The Middle East Nanomedicine market is growing from a low base, led by the UAE, Saudi Arabia, and Israel. The UAE has invested in biotechnology and pharmaceutical research infrastructure through Dubai Science Park and Abu Dhabi's Cleveland Clinic partnership network, creating a foundation for nanomedicine clinical adoption. Israel is the standout innovation hub in the region — with a deep biotech ecosystem and strong academic nanomedicine research at the Hebrew University of Jerusalem and Technion. The GCC countries (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, and Oman) are building pharmaceutical manufacturing capacity under Vision 2030-aligned healthcare localisation policies that favour nanomedicine as a high-value medical technology. Turkey is an emerging market with growing clinical trial activity. The primary challenge in the region is the absence of locally developed nanomedicine regulatory guidance, requiring reliance on FDA or EMA precedents for product approval.

-

Africa Nanomedicine Market

Africa remains the nascent Nanomedicine market globally, but represents a meaningful long-term opportunity as infrastructure and healthcare investment grows. South Africa leads the continent, supported by the South African Nanotechnology Initiative and partnerships between the Council for Scientific and Industrial Research (CSIR) and international pharmaceutical companies. Egypt is the second-largest market, with pharmaceutical manufacturing investment in the Cairo and Alexandria industrial zones. Nigeria and Morocco are expanding their healthcare research infrastructure through government-led investment programmes. The primary market dynamic in Africa is nano-enabled diagnostics rather than therapeutics — affordable, lateral-flow based nanoparticle diagnostic products for HIV, tuberculosis, and malaria represent the most commercially immediate nanomedicine application across Sub-Saharan Africa. Infrastructure constraints — cold chain logistics, clinical administration training, and regulatory capacity — remain the primary barriers to therapeutic nanomedicine adoption across most of the continent.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Full Country Coverage

|

REGION |

COUNTRIES COVERED |

|

North America |

The U.S., Canada, Mexico |

|

Europe |

Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe |

|

Asia Pacific |

China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific |

|

Latin America |

Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America |

|

The Middle East |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

Africa |

South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa |

**Country-level market sizing, historical data, and forecasts available for all geographies listed. Custom regional add-ons available — contact sales@zionmarketresearch.com

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Nanomedicine Market: Competitive Landscape

- The Global Nanomedicine competitive landscape is moderately fragmented at the product level but increasingly concentrated at the platform level. Large-cap pharmaceutical companies command the commercial market through approved liposomal and LNP products, while specialised nanotech developers hold the pipeline growth advantage through novel platform technologies. The dominant strategic pattern is partnership-led platform expansion — established pharma companies licensing or co-developing nanoparticle delivery systems from specialist developers, rather than building internal nanoparticle engineering capabilities from scratch. This dynamic makes platform ownership the primary source of long-term competitive advantage.

- Key players operating in the Global Nanomedicine market include: Pfizer Inc. (U.S.), Novartis AG (Switzerland), Johnson & Johnson Services Inc. (U.S.), Abbott Laboratories (U.S.), AstraZeneca plc (U.K.), Gilead Sciences Inc. (U.S.), Merck & Co. Inc. (U.S.), Sanofi S.A. (France), F. Hoffmann-La Roche AG (Switzerland), Teva Pharmaceutical Industries Ltd. (Israel), Amgen Inc. (U.S.), Alnylam Pharmaceuticals Inc. (U.S.), Arrowhead Pharmaceuticals Inc. (U.S.), Nanobiotix S.A. (France), and GE Healthcare (U.S.).

|

Company |

HQ Country |

Primary Focus |

Key Strategy |

Notable Recent Action |

|

Pfizer Inc. |

U.S. |

LNP therapeutics & vaccines |

Platform licensing & self-commercialisation |

Paxlovid LNP antiviral global rollout; BioNTech LNP vaccine partner |

|

Novartis AG |

Switzerland |

Gene therapy & nanoformulation |

R&D-led organic growth + M&A |

USD 23B U.S. R&D investment announced April 2025 |

|

Johnson & Johnson |

U.S. |

Oncology & infectious disease |

Broad portfolio diversification |

Janssen Pharmaceuticals nano-oncology pipeline expansion |

|

Abbott Laboratories |

U.S. |

Diagnostic nanomedicine |

Diagnostics platform expansion |

Nano-biosensor IVD portfolio investment |

|

AstraZeneca plc |

U.K. |

RNAi & LNP therapeutics |

Strategic partnership model |

Silence Therapeutics RNAi partnership, Q2 2024 |

|

Gilead Sciences Inc. |

U.S. |

Antiviral nanoformulations |

Licensing + in-house development |

NanoThera platform exclusive rights acquisition, 2025 |

|

Merck & Co. Inc. |

U.S. |

Oncology nano-delivery |

Pipeline integration |

LNP combination with PD-1 checkpoint inhibitors |

|

Sanofi S.A. |

France |

Rare disease & oncology |

Dedicated nanomedicine division |

Dr. Maria Lopez appointed Global Head of Nanomedicine, Q1 2025 |

|

Alnylam Pharmaceuticals |

U.S. |

RNAi / siRNA LNP delivery |

First-mover RNAi platform |

Onpattro (patisiran) — first FDA-approved LNP therapeutic |

|

Nanobiotix S.A. |

France |

Radio-enhancer nanoparticles |

Clinical development focus |

NBTXR3 Phase 3 head & neck cancer collaboration, 2024 |

|

Arrowhead Pharmaceuticals |

U.S. |

RNAi cardiometabolic |

Subcutaneous delivery platform |

ARO-APOC3 Phase 3 cardiovascular programme |

|

Nanoform Finland Plc |

Finland |

Nanoparticle engineering services |

CDMO model + Japan partnership |

CBC Co. partnership for Japan market, April 2024 |

|

F. Hoffmann-La Roche AG |

Switzerland |

Diagnostics + oncology nano |

Full value chain integration |

Nanoparticle contrast agent portfolio expansion |

|

Teva Pharmaceutical |

Israel |

Generic liposomal products |

Cost-leadership generalisation |

Liposomal doxorubicin generic global distribution |

|

GE Healthcare |

U.S. |

Nano-enhanced imaging |

Diagnostics platform leadership |

Nanoparticle MRI contrast agent portfolio |

- The competitive set's shared strategic reality is that nanoparticle platform ownership — not individual product revenues — determines long-term positioning. The LNP IP dispute ecosystem (Moderna vs Alnylam, Moderna vs Arbutus) signals that platform-level competition will increasingly play out in licensing courts as well as clinical trial readouts. Companies building second-generation LNP or non-LNP platform IP now are positioning for the 2028–2032 commercial wave, when the current Phase 2 pipeline reaches commercial stage.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Recent Developments in the Nanomedicine Market

Strategic activity in the Global Nanomedicine market accelerated through 2024–2025, with investment, partnership, and regulatory milestones concentrated in LNP therapeutics, RNAi delivery, and nano-oncology. The following developments reflect the market's current pace of change.

|

Date |

Company |

Type |

Description |

Market Impact |

|

Apr 2025 |

Novartis AG |

Investment |

Announced USD 23B five-year U.S. manufacturing and R&D investment, including advanced nanoformulation drug delivery |

Accelerates LNP and polymeric nanoparticle pipeline capacity in North America |

|

Apr 2025 |

Satio / Nanowear |

Partnership |

Collaboration integrating Nanowear's AI-based nanotechnology diagnostic platform with Satio's drug delivery systems for home-based care |

Advances personalised nanomedicine outside hospital settings |

|

Apr 2025 |

Nanopharmaceutics / NCI |

Clinical Trial |

Phase 1 study of Triapine nanomedicine in combination with radiation for recurrent glioblastoma initiated |

Expands neurological indication pipeline |

|

Q2 2024 |

AstraZeneca / Silence Therapeutics |

Partnership |

Co-development agreement for RNAi nanomedicines targeting cardiovascular, renal, and metabolic diseases using LNP delivery |

Validates LNP platform beyond oncology and vaccines |

|

Apr 2024 |

Nanoform / CBC Co. |

Partnership |

Strategic partnership deploying Nanoform's AI-assisted nanomedicine engineering in the Japanese pharmaceutical market |

Opens Asia Pacific CDMO market for nanoparticle formulation services |

|

Sep 2024 |

University of Chicago Medicine |

R&D |

Developed nanomedicine improving chemotherapy penetration in tumour tissue via STING pathway activation |

Advances nano-oncology clinical evidence base |

About Zion Market Research

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is updated constantly in order to fulfil our clients' requirements for prompt and direct online access. Keeping in mind the client's needs, we have included expert insights on global industries, products, and market trends in this database.

Author:

Mr. Nilesh Patil

Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067

Table Of Content

Methodology

FrequentlyAsked Questions

The Zion Market Research's Nanomedicine market report delivers 300+ pages of structured market intelligence: full segmentation analysis across 4 dimensions (type, application, indication, end user), country-level historical data from 2019 and forecasts through 2034 for 35+ countries, a DROC framework covering drivers, restraints, opportunities, and challenges, detailed profiles of 15 leading companies with strategic positioning analysis, 110–140 data tables, and 80–100 charts and figures. The report also includes a structured research methodology and an executive summary designed for C-suite briefing.

The Global Nanomedicine market was valued at USD 16,840 Million in 2025, according to Zion Market Research. The market is forecast to reach USD 84,320 Million by 2034, expanding at a 19.5% CAGR over the forecast period 2026–2034. North America holds the largest regional share. Asia Pacific is the fastest-growing region. Nanoparticles lead by type; drug delivery leads by application; oncology leads by indication.

The report segments the Nanomedicine market across four primary dimensions: (1) By Type — Nanoparticles, Nanoshells, Nanotubes, Nanodevices; (2) By Application — Drug Delivery, Therapeutics, Diagnostics, Regenerative Medicine; (3) By Indication — Oncology, Cardiovascular Diseases, Infectious & Anti-Infective Diseases, Neurological Disorders, Others; (4) By End User — Hospitals & Clinics, Pharmaceutical & Biotechnology Companies, Research & Academic Institutes, Diagnostic Laboratories. Each segment includes historical sizing, 2025 share estimates, and 2026–2034 forecasts.

The report covers 35+ countries across all 6 ZMR regions — Middle East and Africa are always covered as separate regions, never combined. North America: The U.S., Canada, Mexico. Europe: Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe. Asia Pacific: China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific. Latin America: Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America. The Middle East: GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East. Africa: South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa.

Zion Market Research offer full report customization including: additional market segments or sub-segments not covered in the standard report scope; specific country or regional deep-dives beyond the standard 35+ country coverage; extended forecast periods beyond 2034; custom competitive analysis for specific vendor sets or partnership landscapes; and sector-specific or indication-specific focus versions of the report. Contact sales@zionmarketresearch.com or call +1 (302) 444-0166 to discuss custom scope requirements.

Three access options: (1) Free Sample (2) Full Report Purchase (3) Custom Inquiry Direct contact: sales@zionmarketresearch.com | +1 (302) 444-0166 | Toll Free: +1 (855) 465-4651.

List of Contents

Nanomedicine Industry PerspectiveNanomedicine OverviewKey InsightsWhy Choose the Zion Market ResearchsMarket Report?Nanomedicine Dynamics (Drivers, Restraints, Opportunities, Challenges)Nanomedicine Report ScopeNanomedicine SegmentationNanomedicine Regional AnalysisNorth AmericaMarketEuropeMarketAsia PacificMarketLatin AmericaMarketThe Middle EastMarketAfricaMarketFull Country CoverageNanomedicine Competitive LandscapeRecent Developments in theMarketHappyClients