Linear Encoder Market Size, Share, Growth, Opportunities 2034

Linear Encoder Market By Type (Incremental Linear Encoders and Absolute Linear Encoders), By Output Signal (Transistor-Transistor Logic (TTL), High Threshold Logic (HTL), Analog Output, and Digital Output), By Application (Machine Tools, Measuring Instruments, Motion Systems, Elevator, and Other Applications), By End-User (Medical, Printing, Semiconductors, Industrial, and Other End-Users) and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 1.3 Billion | USD 3.2 Billion | 9.5% | 2024 |

Linear Encoder Industry Perspective:

What will be the size of the global linear encoder market during the forecast period?

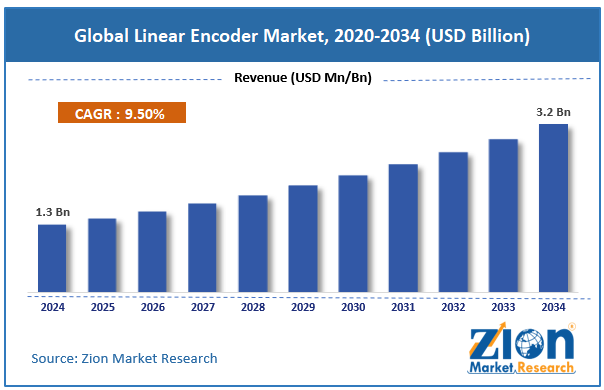

The global linear encoder market size was worth around USD 1.3 billion in 2024 and is predicted to grow to around USD 3.2 billion by 2034, with a compound annual growth rate (CAGR) of roughly 9.5% between 2025 and 2034.

Key Insights

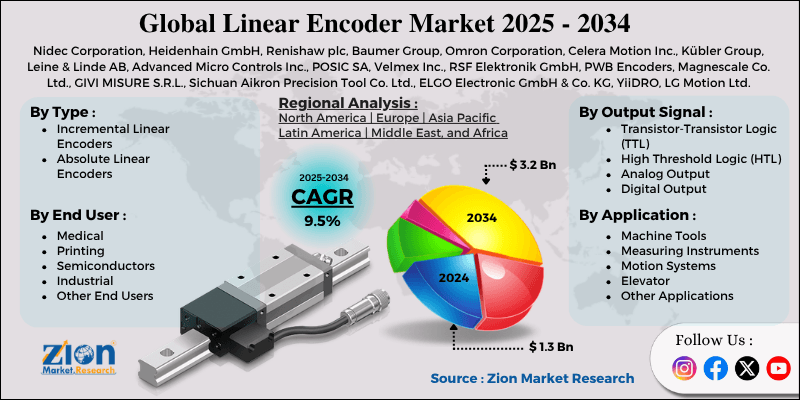

- As per the analysis shared by our research analyst, the global linear encoder market is estimated to grow annually at a CAGR of around 9.5% over the forecast period (2025-2034).

- In terms of revenue, the global linear encoder market size was valued at around USD 1.3 billion in 2024 and is projected to reach USD 3.2 billion by 2034.

- Increasing maritime tourism is expected to propel the linear encoder market over the projected period.

- Based on the type, the incremental linear encoders segment captures the largest market share in 2024.

- Based on the output signal, the Transistor-Transistor Logic (TTL) captures the largest revenue share in 2024.

- Based on the application, the machine tools are growing at a significant rate over the projected period.

- Based on the end-user, the medical segment is growing at a significant rate over the projected period.

- Based on region, North America accounted for the highest market share in the linear encoder market.

Linear Encoder Market: Overview

A linear encoder, also known as a linear variable differential transformer (LVDT) or linear sensor, is a type of position sensor that provides an accurate measurement of linear position, displacement, or motion along a single axis via an electrical output signal for recording or feedback control. They are generally made of a scale or measuring track and a readhead or sensor that moves in the same direction as the tracked object and registers its position changes. They rely on optical, magnetic, or capacitive sensing to provide measurements with sub-nanometer resolution. They are used in motion control systems, including circuit boards, CNC (computer-numerically-controlled) machines, industrial automotive systems, robotics, and semiconductor manufacturing, for accurate position feedback in guidance control.

Linear Encoder Market: Dynamics

Growth Drivers

Why do rising industrial automation and Industry 4.0 adoption drive the linear encoder market?

The increasing acceptance of industrial automation and Industry 4.0 technologies is the key factor driving the linear encoder market, as these high-end automation systems require real-time feedback on machine and part position, as well as accurate motion control. Governments around the world are encouraging and supporting the adoption of advanced manufacturing technologies to advance the smart manufacturing concept through policies and investments. As stated by India’s Press Information Bureau (PIB), referring to the Indian manufacturing sector’s shift to automated, process-centric operational models to increase productivity and efficiency, automation is a top priority for the country.

Similarly, the Indian government has promoted the use of automation solutions through incentive schemes, such as the Production Linked Incentive (PLI) Scheme, with an estimated expenditure of around $ 24 billion. The scheme meant to promote consumption and advancement of Production and other advanced manufacturing technologies, such as automation, robotics, IoT, and AI, is part of the Industry 4.0 revolution, and last but not least, they require highly accurate and sensitive feedback devices, such as linear encoders, to ensure proper positioning and movement in machines and robotic arms. From a statistical point of view, demand for industrial automation is growing rapidly, with Indian manufacturing enterprises investing more than 12,000 crores in automation systems in 2023 alone (to reduce downtime and labor costs and increase precision). The number of robotics units installed in the Indian manufacturing sector reached 8,510 in 2023, with a year-over-year growth rate of 59% (the 3rd-highest in the world), as reported by the International Federation of Robotics. This increase in industrial-automation robot penetration will inevitably drive greater demand for linear encoders.

Restraints

The high initial cost of advanced linear encoders is hindering the linear encoder market

The cost of advanced linear encoders is one of the main limiting factors of the linear encoder market. Large capital expenditure goes into producing advanced linear encoders, optical/laser, high-resolution variants due to the requirements in terms of quality of manufacturing materials involved, accurate geometric tolerances, point-to-point tolerances, accuracy of sensing element, and others. These factors increase the product's cost, leading to a higher end-user price. This becomes prohibitively expensive for medium and small enterprises that intend to use linear encoder technology but cannot justify the added cost of these sophisticated measurement systems vis-à-vis other low-cost alternatives (such as rotary encoders and low-cost position sensors).

Most SMEs may be tempted to use cheaper alternatives if the required degree of linearity or precision is relatively low, thereby making capital investment less justified. The total cost of ownership of the advanced linear encoder also includes installation, calibration, and system integration costs. The need for a compatible control system and the maintenance staff's necessary expertise led to higher initial implementation costs. This is a significant factor in enabling industries in developing nations to avail of advanced linear encoder technology and poses a significant entry barrier into the market. Therefore, the high cost of advanced linear encoders is a factor limiting their market growth.

Opportunities

Why does the increasing adoption of linear encoders in healthcare equipment offer a lucrative opportunity for the linear encoder market?

The increasing adoption of sophisticated technologies in the medical industry is providing a lucrative platform for the linear encoder market. Conventional equipment is now being replaced by technologically advanced instruments where precision is of utmost importance. For instance, high-precision motion control systems are employed in MRI and CT scanners, laser and robotic surgical equipment, X-ray imaging equipment, and other healthcare tools and apparatus. Present-day medical instrumentation requires accurate, efficient, and highly precise positioning. This can be achieved by employing linear encoders, which deliver micron-level accuracy in today's medical devices, thereby improving imaging clarity, treatment efficacy, instrument targeting precision, and overall treatment quality.

As the world is witnessing a rising incidence of complex diseases, demand for progressive diagnostic equipment is also escalating. Parallel to this, a significant increase in the number of minimally invasive procedures is also being observed. Surgeons performing such procedures are increasingly equipping their robotic systems with high-accuracy encoders that provide real-time feedback and enhance precision. Industrial applications, driven by government aid and healthcare expenditure, are also augmenting market growth. In the specified market, high-cost investments by healthcare providers are driving growth in the procurement of high-end equipment, which in turn is boosting sales of linear encoders. Furthermore, portable, compact medical instruments utilize miniaturized, high-performance encoders, thereby broadening the scope of this market.

Challenges

How does the competition from alternative position-sensing technologies pose a significant challenge to the linear encoder market?

Competition from alternative position-sensing technologies is a major factor inhibiting the linear encoder market's expansion in markets that do not demand ultra-high accuracy. A key challenge is that alternative technologies, such as rotary encoders, Hall-effect sensors, potentiometers, and laser displacement sensors, often deliver sufficient performance at lower cost. For many industrial applications, such as simple automation, truck loading, or consumer equipment, the additional accuracy provided by a linear encoder is not worth the added expense.

Therefore, the addressable linear encoder market will be constrained by the popularity of lower-cost alternatives. A second challenge that alternative sensing technologies will have to overcome is their comparative ease of integration and operation. Most other sensors, particularly those based on magnetic sensing, are easier to install and do not require the same degree of precision in loading and alignment as linear encoders. Linear encoders can take many hours to calibrate and align after installation, thereby increasing labor costs and installation time. Some competing sensor types are immune to conditions that hinder optical encoders, such as dust or dirt.

Linear Encoder Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Linear Encoder Market |

| Market Size in 2024 | USD 1.3 Billion |

| Market Forecast in 2034 | USD 3.2 Bllion |

| Growth Rate | CAGR of 9.5% |

| Number of Pages | 226 |

| Key Companies Covered | Nidec Corporation, Heidenhain GmbH, Renishaw plc, Baumer Group, Omron Corporation, Celera Motion Inc., Kübler Group, Leine & Linde AB, Advanced Micro Controls Inc., POSIC SA, Velmex Inc., RSF Elektronik GmbH, PWB Encoders, Magnescale Co. Ltd., GIVI MISURE S.R.L., Sichuan Aikron Precision Tool Co. Ltd., ELGO Electronic GmbH & Co. KG, YiiDRO, LG Motion Ltd., and others. |

| Segments Covered | By Type, By Output Signal, By Application, By End User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Linear Encoder Market: Segmentation

Type Insights

Why do the incremental linear encoders dominate the linear encoder market?

The incremental linear encoders segment captures the largest market share in 2024. The growth is mainly attributed to its affordability, simplicity, and general use in industrial automation. While absolute encoders provide absolute position feedback, incremental encoders provide relative position information, which is generally acceptable for most industrial applications, such as CNC machines, conveyor systems, packaging, and simple motion control systems. The lower market price also makes incremental encoders more appealing to SMEs and budget-constrained industries.

Output Signal Insights

Is Transistor-Transistor Logic (TTL) growing at the highest rate in the linear encoder market?

The Transistor-Transistor Logic (TTL) captures the largest revenue share in 2024. This is the most significantly growing one due to its high signal reliability, high-speed response, and excellent compatibility with industrial control systems. TTL output signals are used in many incremental linear encoders because they provide distinct digital signals, are less susceptible to noise, and are ideal for high-speed, high-accuracy motion control (for example, CNC machines, robots, production lines, and others).

Application Insights

Why are machine tools growing at a significant rate in the linear encoder market?

The machine tools are growing at a significant rate over the projected period. This segment is driven by a growing need for high-accuracy manufacturing and machining processes. In fact, linear encoders are mostly used in the machine tool industry, for instance, in CNC milling machines, lathes, grinding machines, and machining centers, where they serve to accurately determine the position of the machine tool and to ensure precise positioning of the tool to meet tight tolerances and higher product quality standards. The automotive, aerospace, and electronics industries are expected to be the strongest markets for high-precision machine tools, making them the strongest current end-use markets for linear encoders. This segment will also benefit from the rise of CNC (Computerized Numerical Control) machines, which require encoder position feedback to greatly improve positioning precision.

End User Insights

Why are medical end users growing at a significant rate in the linear encoder market?

The medical segment is growing at a significant rate over the projected period. This growth is attributable to the greater use of highly accurate diagnostic and therapeutic equipment. The extensive use of linear encoders in new and established medical equipment, such as MRIs, CT scanners, radiation therapy systems, and robotic surgery systems, reflects their vital role in the medical environment, enabling accurate positioning and smooth movement for precise diagnostics and effective therapies. The need for higher-quality medical services and imaging technologies can help linear encoders grow significantly.

Regional Insights

Why does North America lead the linear encoder market?

North America accounted for the highest share in the linear encoder market in 2024. The growth in North America is primarily attributed to a well-established manufacturing ecosystem in the region, along with early adoption of automation technologies and large investments made to develop high-precision industries. The established markets in electronics, aerospace, automotive, and semiconductor manufacturing ensure ever-growing demand for high-precision motion control solutions, and linear encoders are commonplace thanks to their high accuracy, reliability, and performance.

Another significant driver of growth for the linear encoders market in North America is the accelerated adoption of Industry 4.0 and smart factory capabilities by manufacturers in the region. Manufacturing companies are progressively deploying automation solutions, such as robots, CNC systems, and automated manufacturing lines, to improve productivity and efficiency and reduce downtime, thereby driving rising demand for linear encoders in the region.

Furthermore, North America continues to be a hotbed of technological innovation and research, and the constant increase in new developments in detection, digital control, and digital interfacing drives the linear encoders market in the region. The leading market players and technology providers have contributed to the region's overall market growth through investments and ongoing product development.

Linear Encoder Market: Competitive Analysis

The global linear encoder market is dominated by players like:

- Nidec Corporation

- Heidenhain GmbH

- Renishaw plc

- Baumer Group

- Omron Corporation

- Celera Motion Inc.

- Kübler Group

- Leine & Linde AB

- Advanced Micro Controls Inc.

- POSIC SA

- Velmex Inc.

- RSF Elektronik GmbH

- PWB Encoders

- Magnescale Co. Ltd.

- GIVI MISURE S.R.L.

- Sichuan Aikron Precision Tool Co. Ltd.

- ELGO Electronic GmbH & Co. KG

- YiiDRO

- LG Motion Ltd.

The global linear encoder market is segmented as follows:

By Type

- Incremental Linear Encoders

- Absolute Linear Encoders

By Output Signal

- Transistor-Transistor Logic (TTL)

- High Threshold Logic (HTL)

- Analog Output

- Digital Output

By Application

- Machine Tools

- Measuring Instruments

- Motion Systems

- Elevator

- Other Applications

By End User

- Medical

- Printing

- Semiconductors

- Industrial

- Other End Users

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

A linear encoder, also known as a linear variable differential transformer (LVDT) or linear sensor, is a type of position sensor that provides accurate measurement of linear position, displacement, or motion along a single axis in an electrical output signal for recording or feedback control purposes.

The key growth drivers for the linear encoder market include the rapid adoption of industrial automation and Industry 4.0 (driving demand for precise motion control), increasing need for high-accuracy positioning in manufacturing (ensuring better product quality), expansion of CNC machines and semiconductor industries (requiring reliable feedback systems), rising use of robotics and automated systems (enhancing efficiency and productivity), growing adoption in advanced healthcare equipment (enabling precise diagnostics and treatment), and continuous technological advancements (improving performance and expanding application areas).

The major challenges restraining the growth of the linear encoder market include the high initial cost of advanced linear encoders (limiting adoption among cost-sensitive users), complex installation and alignment requirements (increasing deployment time and technical difficulty), susceptibility of certain encoder types to harsh environmental conditions such as dust, vibration, and temperature variations (affecting performance and reliability), the need for skilled workforce for operation and maintenance (raising operational costs), and strong competition from alternative position-sensing technologies (offering lower-cost or easier-to-integrate solutions).

Based on the end-user, the medical segment is expected to dominate the linear encoder market growth during the projected period.

One of the most prominent trends is the increasing demand for ultra-high precision motion measurement, especially in industries such as semiconductor manufacturing and nanotechnology, where even nanometer-level accuracy is required. At the same time, manufacturers are focusing on smart encoder integration, enabling real-time data feedback, connectivity with industrial IoT systems, and seamless operation within Industry 4.0 environments.

According to the report, the global linear encoder market size was worth around USD 1.3 billion in 2024 and is predicted to grow to around USD 3.2 billion by 2034.

The global linear encoder market is expected to grow at a CAGR of 9.5% during the forecast period.

The global linear encoder industry growth is expected to be led by North America over the forecast period.

The global linear encoder market is dominated by players like Nidec Corporation, Heidenhain GmbH, Renishaw plc, Baumer Group, Omron Corporation, Celera Motion Inc., Kübler Group, Leine & Linde AB, Advanced Micro Controls Inc., POSIC SA, Velmex Inc., RSF Elektronik GmbH, PWB Encoders, Magnescale Co. Ltd., GIVI MISURE S.R.L., Sichuan Aikron Precision Tool Co. Ltd., ELGO Electronic GmbH & Co. KG, YiiDRO, and LG Motion Ltd., among others.

The linear encoder market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients