Healthcare Command Centers Market Size, Share, Value and Forecast 2034

Healthcare Command Centers Market By Type (Operational Command Centers, Emergency & Disaster Response Command Centers, Patient Flow Command Centers, Clinical Command Centers and Integrated/Enterprise-Wide Command Centers), By Component (Software, Hardware and Services), By Application (Patient Flow & Capacity Management, Emergency Response & Crisis Management, Bed Management, Staff Allocation & Scheduling, Telehealth & Remote Care Coordination and Real-Time Decision Support), By End User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Multi-Hospital Health Systems and Government & Military Health Facilities), By Deployment Mode (On-Premise, Hybrid and Cloud-Based) and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

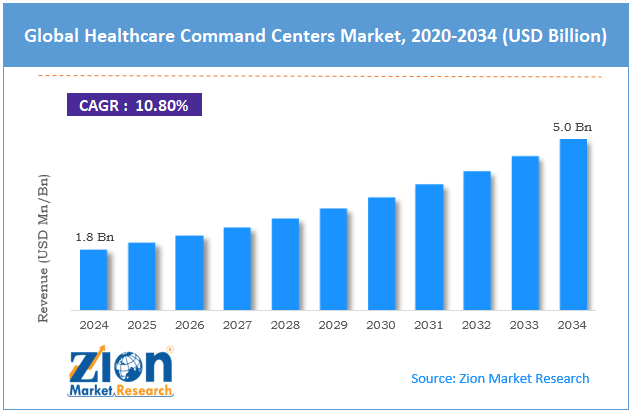

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 1.8 Billion | USD 5.0 Billion | 10.8% | 2024 |

Healthcare Command Centers Industry Perspective:

What will be the size of the global healthcare command centers market during the forecast period?

The global healthcare command centers market size was worth around USD 1.8 billion in 2024 and is predicted to grow to around USD 5.0 billion by 2034 with a compound annual growth rate (CAGR) of roughly 10.8% between 2025 and 2034.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Key Insights

- As per the analysis shared by our research analyst, the global healthcare command centers market is estimated to grow annually at a CAGR of around 10.8% over the forecast period (2025-2034).

- In terms of revenue, the global healthcare command centers market size was valued at around USD 1.8 billion in 2024 and is projected to reach USD 5.0 billion by 2034.

- Growing digital transformation of hospitals are expected to propel the healthcare command centers market over the projected period.

- Based on the type, in terms of revenue generation, the patient flow command centers segment will drive strong revenue for the healthcare command centers market.

- Based on the component, the software segment is accounted for the highest revenue share of 48% in the market.

- Based on the application, the patient flow & capacity management segment capture the largest market share in the healthcare command centers market.

- Based on the end user, the hospitals segment dominated the market in 2024.

- Based on the deployment mode, the cloud-based segment dominated the market with a revenue share of 49% in 2024.

- Based on region, North America accounted for the largest market share in 2024 of 41%.

Healthcare Command Centers Market: Overview

Healthcare command centers are centralized operating units that use information gathered from multiple platforms to monitor the clinical, administrative, and logistical aspects of the healthcare facility's operations and provide a clear view of all patient care activities in the hospital. The command centers can do so through the application of innovative technologies such as artificial intelligence (AI), predictive analytics, machine learning, Internet of Things (IoT) devices, and EHRs. The information is then used to ensure better patient flow, monitor bed occupancy levels, optimize workforce staffing, track equipment usage, and monitor emergency activities at the hospitals. With information from command center facilities, facility managers can make better decisions in their processes.

Impact of the USA-Israel War on Iran on the Healthcare Command Centers Market

The USA-Israel war against Iran has had a mixed but rather positive influence on the Healthcare Command Centers Market by increasing demand for real-time coordination of health activities, emergency management, resource optimization, and hospital resiliency in the event of an emergency. With the escalation of the USA-Israel war in different countries in the Middle East region, affecting the health facilities of these countries in one way or another, there has been a rush for healthcare establishments and government bodies to invest in command-and-control centers as a means of improving their operations. One of the main effects is an increase in the need for emergency management. Hospitals under attack by missiles or facing other emergencies need to coordinate aspects such as bed management, trauma care, staffing, ambulance dispatching, and others.

Healthcare Command Centers Market: Dynamics

Growth Drivers

Why does the rising need for efficient patient flow management drive the healthcare command centers market?

An increase in the demand for effective patient flow management in healthcare facilities is another factor propelling growth in the healthcare command centers market. Healthcare facilities have been facing many challenges, including increased patient volume, limited bed capacity, staffing shortages, and operational inefficiencies. These challenges create a problem commonly known as inefficient patient flow. Such a phenomenon involves emergency department congestion, long wait times for services, delayed patient admission and discharge, low bed capacity, and increased healthcare-related expenditures. The introduction of healthcare command centers helps manage patient flow by providing real-time information on patients moving through a hospital. In particular, these centers help monitor patients' admissions, transfers, discharges, bed capacity, and the use of other resources.

Using electronic health record data, bed management systems, staffing platforms, and clinical workflow solutions, healthcare command centers help identify bottlenecks and predict patient demand. In this manner, hospitals can ensure that patient waiting time is shortened, bed turnovers increase, care is delivered more quickly, and, thus, a positive patient experience is achieved. It is also noteworthy that efficient patient flow management helps optimize hospital capacity, reduce operational costs, and increase staff productivity. In this way, the increase in demand for efficient patient flow management among healthcare providers contributes to the growth of the healthcare command centers market.

Restraints

High initial implementation and infrastructure costs hamper the growth of the healthcare command centers industry

High implementation and infrastructure costs pose a significant barrier to the expansion of the healthcare command centers market, making it very costly for healthcare institutions to set up command centers. It is necessary to invest heavily in advanced software, AI and analytics technologies, data integration services, cloud and on-premises infrastructures, advanced visualization systems, cybersecurity measures, and staff training programs. Moreover, in many cases, healthcare institutions must improve their current IT infrastructure by implementing EHRs, HISs, and bed management systems, which increases deployment costs. High deployment and implementation costs translate into additional expenses associated with the process, such as customization, consulting, maintenance, and technical support services. Healthcare institutions often find themselves unable to spend large sums on setting up command centers because the benefits may take too long to be recognized by healthcare organizations facing financial hardships.

As a result, hospitals prefer to delay the implementation of command centers and focus on other investments that can deliver quicker financial benefits. High costs are a particularly critical issue for developing countries with insufficient funding for healthcare infrastructure. Therefore, cost-related challenges are the main constraints on the adoption of command centers in healthcare settings.

Opportunities

Why does the growing product launch offer a lucrative opportunity for the healthcare command centers market?

The growing product launch is expected to offer a potential opportunity to the healthcare command centers market growth over the projected period. Foe instance, in April 2026, ANSR, the world's leading GCC solutions vendor, recently introduced its new Healthcare GCC Accelerator Platform. This innovative platform will enable healthcare companies to establish AI-enabled GCCs faster and with greater assurance than ever before. In addition to the unique capabilities of its own GCC execution process, ANSR’s new Healthcare GCC Accelerator platform includes Optum’s state-of-the-art healthcare AI technologies.

As part of their collaboration, ANSR will benefit from Optum’s cutting-edge Optum.ai technology and deep healthcare experience to enable their customers’ operations modernization, AI integration, and the formation of next-generation global workforces. As more and more companies recognize the importance of GCCs as engines of their digital transformation and scalable operations, they are also increasingly concerned about responsible AI adoption. ANSR is here to meet this need by combining its strong GCC delivery with AI capabilities already in place in the healthcare industry.

Challenges

Why does the limited adoption in developing regions pose a significant challenge to the healthcare command centers market?

The inability to adopt technology in developing regions is another challenge for the development of the Healthcare Command Centers industry, as many healthcare providers in emerging markets face budget and technical limitations that make it impossible to integrate command centers into their routine. Advanced command centers require significant investments in digital infrastructure, advanced software and hardware, and connectivity solutions such as high-speed Internet. At the same time, many hospitals in developing countries are forced to invest little in information technology and to develop an adequate information network that would allow efficient use of command centers.

In addition, healthcare facilities in developing regions may prioritize the provision of basic health care, equipment purchases, and construction over investing in operational management tools. There is a shortage of professionals who know how to use these systems due to limited knowledge of healthcare informatics, artificial intelligence, analytics, and IT-related topics. Some regions lack sufficient digitalization to support the effective functioning of command centers and ensure consistent electricity, Internet connectivity, and other prerequisites. Finally, healthcare professionals in some countries fail to understand the advantages of implementing this innovation.

Healthcare Command Centers Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Healthcare Command Centers Market |

| Market Size in 2024 | USD 1.8 Billion |

| Market Forecast in 2034 | USD 5.0 Billion |

| Growth Rate | CAGR of 10.8% |

| Number of Pages | 227 |

| Key Companies Covered | GE HealthCare, ABOUT Healthcare Inc., Koninklijke Philips N.V., TeleTracking Technologies Inc., Siemens Healthineers, Qventus, Oracle (Cerner), Epic Systems, LeanTaaS, Dedalus, care.ai, Care Logistics, Constant Technologies Inc, L&T Technology Services Limited, Leidos, Systematic Healthcare, ASCEND Solutions, and others. |

| Segments Covered | By Type, By Component, By Application, By End User, By Deployment Mode, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Healthcare Command Centers Market: Segmentation

Type Insights

Why does the patient flow command centers dominate the healthcare command centers market?

In terms of revenue generation, the patient flow command centers segment will drive strong revenue for the healthcare command centers market due to the growing need for healthcare organizations to manage patient flow, improve bed occupancy, and avoid operational limitations. Increased admissions, overcrowded ERs, higher demand for healthcare services, and a labor shortage push healthcare organization to use patient flow command centers to ensure better medical assistance. Through such command centers, access to information on patients' admissions, transfers, discharges, available beds, and other factors becomes easier, and healthcare organizations can make decisions quickly with the help of AI technologies, predictions, and integration into hospitals' information systems. It results in reduced waiting times, shorter patient stays, higher bed turnover rates, and greater overall hospital efficiency.

Component Insights

How does the software segment capture the largest market share in the healthcare command centers market?

The software segment is accounted for the highest revenue share of 48% in the market due to the growing adoption of digital healthcare technologies, artificial intelligence (AI), predictive analytics, and operational management technologies in the healthcare industry. Healthcare command center software serves as the backbone of all the technology integrated into the system and as an aggregation tool that collects data from various sources, such as EHRs, hospital information systems, bed management systems, staff management software, medical devices, and other operational systems, all within a centralized platform.

Application Insights

How does the patient flow & capacity management segment capture the largest market share in the healthcare command centers market?

Revenue from patient flow and capacity management would grow significantly in the Healthcare command centers market as the importance of managing patient inflow and improving efficiency increases. Some hospitals have begun integrating systems to improve patient flow and capacity management due to problems such as overcrowding in the emergency room, a slow admission process, delays in discharging patients, insufficient beds, and staff shortages. The systems enable understanding of the process, including tracking patients, monitoring bed occupancy rates, managing transitions in patient care, and optimizing resource use.

End User Insights

Why does the hospitals segment capture the largest market share in the healthcare command centers market?

The hospitals segment dominated the market in 2024. The growth is driven by the need to centralize operations management, improve coordination of patient services, and more efficiently use resources. Hospitals face increasing difficulties due to higher patient admissions, overcrowding in the emergency department, limited beds, workforce limitations, and operational complexity. This situation leads to the emergence of solutions such as healthcare command centers. Healthcare command centers provide real-time information on the number of patients, their condition, the number of available beds and equipment, and other essential factors that enable quick decision-making. Moreover, the use of AI, predictive analytics, electronic medical records, and IoT-enabled technologies provides even greater flexibility.

Deployment Mode Insights

Does cloud-based segment capture the largest market share in the healthcare command centers market?

The cloud-based segment dominated the market with a revenue share of 49% in 2024. The growth of this market can be attributed to the increased deployment of scalable, flexible, and cost-effective digital healthcare infrastructure. Cloud-based healthcare command centers allow healthcare organizations to centralize and access real-time information on their operations, clinical, and administrative processes across their facilities without building extensive infrastructure within the organization. These cloud-based command centers facilitate easy integration with electronic health record (EHR) systems, hospital information systems, IoT-based medical devices, and analytics tools, providing insight into issues concerning patient throughput, bed availability, staffing, and resource allocation.

Regional Insights

Why does North America lead the healthcare command centers market?

North America accounted for the largest market share in 2024 of 41%. Factors responsible for growth include a highly developed healthcare infrastructure, the application of digital health technologies, and improvements in hospital operational efficiency. Healthcare institutions in the US and Canada have found it necessary to implement command centers to address challenges posed by high patient volumes, overcrowded emergency departments, inadequate staffing, and escalating healthcare costs. The implementation of EHRs, artificial intelligence, predictive analytics, cloud computing, and the Internet of Things in the healthcare systems makes it an appropriate environment for implementing a command center.

Healthcare Command Centers Market: Competitive Analysis

The global healthcare command centers market is dominated by players like:

- GE HealthCare

- ABOUT Healthcare Inc.

- Koninklijke Philips N.V.

- TeleTracking Technologies Inc.

- Siemens Healthineers

- Qventus

- Oracle (Cerner)

- Epic Systems

- LeanTaaS

- Dedalus

- care.ai

- Care Logistics

- Constant Technologies Inc

- L&T Technology Services Limited

- Leidos

- Systematic Healthcare

- ASCEND Solutions

The global healthcare command centers market is segmented as follows:

By Type

- Operational Command Centers

- Emergency & Disaster Response Command Centers

- Patient Flow Command Centers

- Clinical Command Centers

- Integrated/Enterprise-Wide Command Centers

By Component

- Software

- Hardware

- Services

By Application

- Patient Flow & Capacity Management

- Emergency Response & Crisis Management

- Bed Management

- Staff Allocation & Scheduling

- Telehealth & Remote Care Coordination

- Real-Time Decision Support

By End User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Multi-Hospital Health Systems

- Government & Military Health Facilities

By Deployment Mode

- On-Premise

- Hybrid

- Cloud-Based

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Healthcare command centers are centralized operating units that use information gathered from multiple platforms to monitor the clinical, administrative, and logistical aspects of the healthcare facility's operations and provide a clear view of all patient care activities in the hospital.

The key growth drivers for the healthcare command centers market include the rising need for efficient patient flow management, increasing adoption of AI and predictive analytics, growing hospital digitalization, workforce shortages, and the demand for real-time operational visibility and resource optimization.

The major challenges restraining the growth of the healthcare command centers market include high implementation and infrastructure costs, complex integration with legacy healthcare systems, data interoperability issues, cybersecurity concerns, shortages of skilled personnel, and limited adoption in developing regions.

Based on the application, the patient flow & capacity management segment is expected to dominate the healthcare command centers market growth during the projected period.

Emerging trends and innovations impacting the healthcare command centers market include the integration of artificial intelligence (AI) and predictive analytics, adoption of cloud-based command center platforms, real-time patient flow and capacity management solutions, IoT-enabled healthcare monitoring, digital twin technology, advanced data interoperability frameworks, and the development of smart hospital ecosystems that enhance operational efficiency, resource optimization, and patient care coordination.

According to the report, the global healthcare command centers market size was worth around USD 1.8 billion in 2024 and is predicted to grow to around USD 5.0 billion by 2034.

The global healthcare command centers market is expected to grow at a CAGR of 10.8% during the forecast period.

The global healthcare command centers industry growth is expected to be led by North America over the forecast period.

The global healthcare command centers market is dominated by players like GE HealthCare, ABOUT Healthcare, Inc., Koninklijke Philips N.V., TeleTracking Technologies, Inc., Siemens Healthineers, Qventus, Oracle (Cerner), Epic Systems, LeanTaaS, Dedalus, care.ai, Care Logistics, Constant Technologies, Inc, L&T Technology Services Limited, Leidos, Systematic Healthcare, and ASCEND Solutions among others.

The market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients