Surgical Robotics Market Size, Share, Trends & Forecast 2026–2034

Global Surgical Robotics Market by Product Type (Robotic Systems, Instruments & Accessories, Services), by Application (Orthopedic Surgery, Laparoscopic Surgery, Neurosurgery, Cardiovascular Surgery, Others), by End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics), and by Region — Global Industry Perspective, Comprehensive Analysis, and Forecast, 2026–2034-

| Market Size in 2025 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 8,740 Million | USD 34,820 Million | 16.6% | 2025 |

Surgical Robotics Market Industry Perspective:

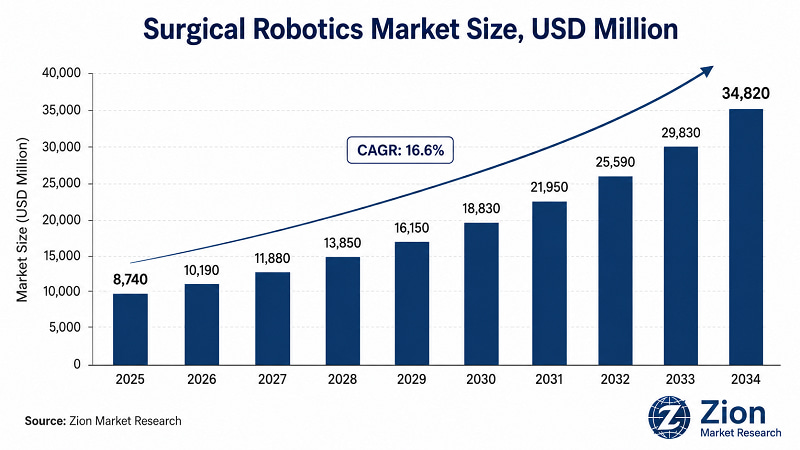

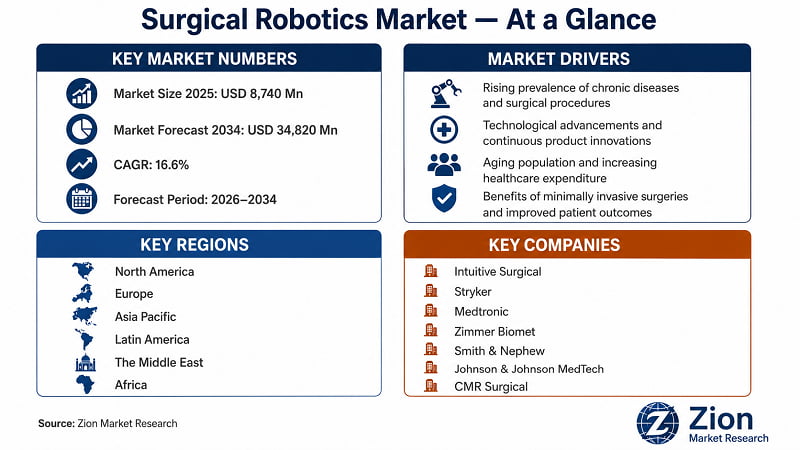

- The global Surgical Robotics market reached USD 8,740 Mn in 2025 — a figure that understates the structural shift now under way in surgical theatre design worldwide. At a 16.6% CAGR through 2034, the market will reach USD 34,820 Mn by the end of the forecast period.

- This is not cyclical expansion. It reflects a durable reconfiguration of how surgery is delivered: robotic platforms are transitioning from premium-tier differentiators to baseline infrastructure in high-volume surgical programmes across

- North America, Europe, and — increasingly — across Asia Pacific's government-directed hospital modernisation pipeline.

- The investment thesis is settled at the macro level. The analytical challenge for procurement executives and capital allocators is identifying which sub-segments, deployment models, and geographies will generate disproportionate returns within that aggregate growth trajectory.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Surgical Robotics Market: Overview

- Surgical Robotics encompasses the full spectrum of hardware, software, and service platforms that integrate robotic actuation, 3D imaging, and AI-guided instrument control into the surgical workflow. The market includes multi-arm robotic consoles (capital systems), reusable and single-use instrument sets, advanced imaging and navigation modules, and the service and training infrastructure that sustains platform utilisation across a hospital's surgical programme. It spans soft tissue applications — laparoscopic general, urological, gynaecological — and hard tissue disciplines including orthopaedic joint replacement and spinal surgery, with neurosurgery and cardiovascular applications forming an emerging third growth frontier.

- The market's value chain operates across three structurally distinct tiers. At the foundational layer, platform OEMs — Intuitive Surgical with da Vinci, Medtronic with Hugo, and Johnson & Johnson MedTech with OTTAVA — supply the capital infrastructure and define the procedural ecosystem. The specialist integration layer includes AI navigation developers such as Brainlab AG (Germany) and software-defined guidance system providers who embed into existing robotic platforms. At the application layer, single-use instrument manufacturers and service network providers — Smith & Nephew for orthopaedic accessories, Globus Medical for spine — deliver the high-frequency recurring revenue that supports long-term OEM relationships.

- For procurement and investment decision-makers, the question is not whether Surgical Robotics will grow — that question is settled — but which segments, geographies, and deployment models will capture disproportionate value within that growth. This report provides sub-segment level data, country-level forecasts, and competitive positioning analysis across 3 segmentation dimensions and 35+ geographies.

Key Insights

- The global Surgical Robotics market is forecast to grow at a 16.6% CAGR between 2026 and 2034, reaching USD 34,820 Mn from USD 8,740 Mn in 2025. (Source: Zion Market Research)

- Dominant Product Segment — Robotic Systems: Robotic systems account for approximately 58% of total market revenue in 2025, driven by high unit ASPs of USD 1 Mn to USD 2.5 Mn and the anchor role capital systems play in platform-lock service ecosystems.

- Fastest-Growing Product Segment — Instruments & Accessories: Instruments & Accessories is the fastest-growing product segment, expanding at above-market CAGR as single-use instrument adoption accelerates across newly installed robotic platforms globally.

- Dominant Application — Laparoscopic Surgery: Laparoscopic surgery holds the largest application share at approximately 38% of 2025 revenue, reflecting the breadth of colorectal, urological, and gynaecological procedures now routinely performed under robotic assistance.

- Dominant End User — Hospitals: Hospitals account for over 70% of surgical robotics demand, concentrating capital investment in flagship surgical programmes where high case volumes justify multi-platform robotic suites.

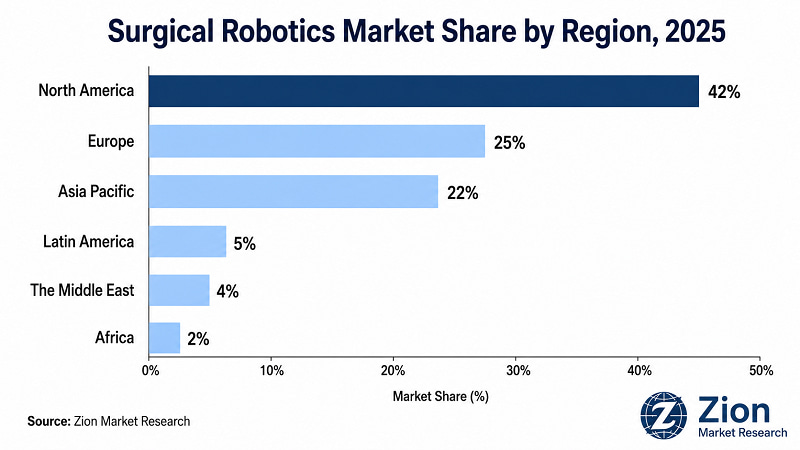

- Dominant Region — North America: North America captures approximately 42% of global market revenue in 2025, anchored by the U.S.'s mature reimbursement environment and the world's highest per-capita density of installed robotic surgical systems.

- Fastest-Growing Region — Asia Pacific: Asia Pacific is forecast to register the highest regional CAGR through 2034, driven by China's Healthy China 2030 hospital modernisation programme and India's AIIMS and tier-2 hospital robotic procurement pipeline.

- Competitive Landscape: The market is moderately consolidated at the platform level, with Intuitive Surgical retaining dominant installed base share globally. Competitive intensity is rising as Medtronic Hugo, J&J MedTech OTTAVA, and CMR Surgical Versius compete on price-performance positioning against the established da Vinci ecosystem.

- Forward-Looking Insight: By 2030, AI-guided autonomous instrument targeting is expected to become a standard software feature across leading robotic platforms — expanding the addressable market to surgeon cohorts currently excluded by the steep learning curve of freehand robotic control.

Why Choose the Zion Market Research's Surgical Robotics Market Report?

Decision-makers comparing market intelligence reports on Surgical Robotics will find the Zion Market Research's report differentiated on the following dimensions.

|

Dimension |

Zion Market Research Report |

Industry Average |

|

Report Pages |

300+ |

~120 pages |

|

Forecast Horizon |

9 years (2026–2034) |

7 years |

|

Segmentation Dimensions |

3 dimensions |

2–3 dimensions |

|

Historical Data |

6 years (2019–2024) |

4–5 years |

|

Country Coverage |

35+ countries |

15–18 countries |

|

Companies Profiled |

15 companies |

10 companies |

|

DROC Framework |

Full (Drivers, Restraints, Opportunities, Challenges) |

Drivers only |

**For custom scope — additional segments, specific geographies, or extended forecast periods — contact sales@zionmarketresearch.com

Surgical Robotics Market: Dynamics (Drivers, Restraints, Opportunities, Challenges)

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

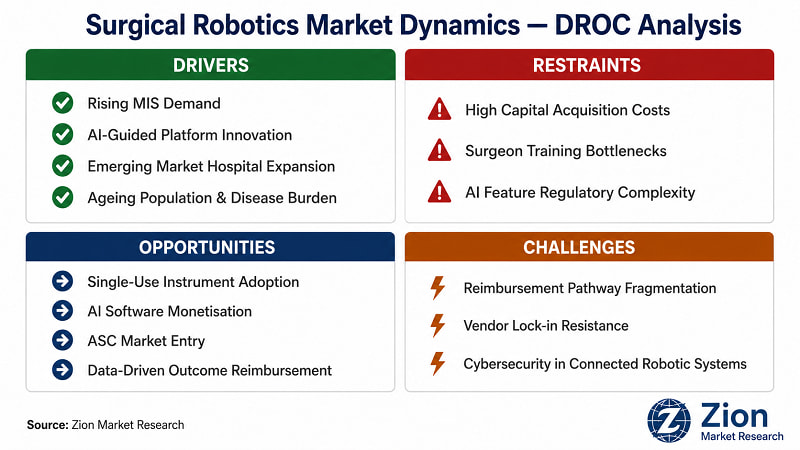

What Is Driving the Surgical Robotics Market?

- Rising Demand for Minimally Invasive Surgical Procedures:

"Patient recovery time and complication profiles are now the primary procurement drivers for surgical robotics — not surgeon preference."

The shift toward minimally invasive surgery (MIS) is structural, not cyclical. Across colorectal, urological, gynaecological, and orthopaedic disciplines, both surgeon and payer communities have aligned behind robotic-assisted MIS as the clinical standard for high-complexity procedures. Robotic platforms deliver tremor filtration, seven-degree-of-freedom instrument articulation, and immersive 3D visualisation that extend the surgeon's technical range beyond what freehand laparoscopic technique allows. The downstream outcome data — reduced blood loss, shorter average hospital stay, and lower 30-day readmission rates — is now sufficiently robust to support reimbursement-level decision-making in the U.S., Germany, and Japan. Intuitive Surgical's da Vinci system had surpassed 8,600 installed units globally as of 2024, with over 2 million procedures performed annually — a scale that demonstrates demand-side pull, not supply-side push. In the U.S., the regulatory tailwind from CMS's value-based care payment models is accelerating hospital ROI calculations on robotic capital investment, particularly for programmes where robotic adoption demonstrably reduces DRG payment exposure.

- Technological Advancement in AI-Guided Robotics and Digital Surgery Platforms:

"The next frontier is not making robots more precise — it's making them more intelligent."

Second-generation robotic surgical platforms are converging on a new capability set: real-time anatomical recognition driven by machine learning, intraoperative imaging integration with augmented reality overlays, and semi-autonomous instrument positioning that reduces the cognitive burden on the operating surgeon. This capability expansion is not incremental. It structurally broadens the addressable surgeon base beyond subspecialty minimally invasive experts to general surgery theatre teams in community hospital settings. Medtronic deployed its Hugo robotic-assisted surgery system across multiple European hospital sites from 2022 onward, with clinical data from early adoption sites demonstrating procedural outcomes comparable to the established da Vinci ecosystem at a meaningfully lower per-procedure instrument cost. Johnson & Johnson MedTech's OTTAVA platform — cleared by the FDA in late 2024 for laparoscopic general surgery — incorporates AI-assisted vessel identification as a standard software feature, reducing intraoperative adverse event risk in complex colorectal cases. The software-driven margin structure of these AI features also changes the OEM revenue model: platform software licensing and data monetisation create recurring revenue streams that reduce dependence on capital hardware replacement cycles.

- Government-Directed Hospital Modernisation in Emerging Markets:

"China's domestic OEM pipeline is not a competitive risk to watch — it's a market dynamic already reshaping procurement in Asia Pacific."

State-directed healthcare infrastructure investment across China, India, GCC nations, and Brazil is creating a structurally new demand cohort for surgical robotics — one that operates on different procurement economics from the established North American and European markets. China's National Healthcare Commission has funded robotic surgery capability across tier-2 and tier-3 hospitals under the Healthy China 2030 national plan, with local OEM Tinavi Medical reporting a 40%+ expansion in domestic hospital client numbers between 2022 and 2024. Critically, local content preference policies in China and India create a structural advantage for domestic OEMs — and a structural headwind for foreign vendors without local manufacturing or joint venture arrangements. In GCC nations, Saudi Arabia's Vision 2030 health cluster programme has allocated capital investment for robotic surgery centre development in Riyadh and Jeddah, creating a procurement pipeline that was effectively zero five years ago. The supply-side implication: OEMs without a localisation strategy — manufacturing partnerships, regional service networks, or government relations infrastructure — face margin compression and market access risk as these geographies scale.

- Ageing Population Dynamics and Growing Burden of Musculoskeletal and Oncological Disease:

"Demographics are not a market trend — they're a structural demand floor."

The global population aged 65 and above is projected to reach 1.5 billion by 2050, with the steepest near-term growth concentrated in Japan, South Korea, Germany, and Italy — all established surgical robotics markets. This demographic cohort generates disproportionate demand for orthopaedic joint replacement, colorectal cancer surgery, and prostate cancer intervention — the three highest-volume robotic procedure categories in the current market. Stryker's MAKO robotic arm system for total knee and total hip arthroplasty demonstrated consistent adoption growth in its installed base through 2024, with the orthopaedic robotics segment growing faster than the broader robotic surgery market average. The oncological burden compounds this effect: WHO cancer incidence projections through 2034 indicate a 40%+ increase in colorectal and prostate cancer case volumes in high-income countries — directly expanding the addressable procedure pool for laparoscopic and urological robotic platforms. The demand floor is not demand-side risk — it's a structural growth guarantee for OEMs positioned in the right sub-segment.

|

"The integration of robotic-assisted surgery into our standard laparoscopic programme has materially reduced average length of stay for colorectal cases. The economic case for robotic investment is no longer theoretical — it's measurable at the payer level." |

|

— Dr. Sarah Abrams, Chief Medical Officer, Northwestern Medicine |

|

(Source: American College of Surgeons Clinical Congress, October 2023) |

|

"Hugo is designed to democratise robotic surgery — to make the clinical and economic benefits of robotic-assisted procedures accessible to a far broader population of hospitals and surgeons than has been possible with first-generation systems." |

|

— Geoffrey Martha, Chairman & CEO, Medtronic |

|

(Source: Medtronic Investor Day, June 2023) |

What Is Restraining the Surgical Robotics Market?

- High Capital Acquisition and Total Ownership Cost:

"The USD 2 Mn per-system acquisition price is not the full cost story — it's the opening bid."

Robotic surgical systems carry acquisition costs of USD 1 Mn to USD 2.5 Mn per platform, with annual service contracts adding USD 100,000 to USD 170,000 in recurring obligations before a single procedure is performed. The total cost of ownership — including instrument set replenishment, consumable replacement, and ongoing software licensing — routinely exceeds USD 3 Mn over a five-year ownership cycle. This financial profile limits adoption to large academic medical centres and well-capitalised community hospital networks in high-income markets. Community hospitals in Latin America, Africa, and lower-income Asia Pacific nations face structural access barriers that manufacturer financing programmes and government subsidy schemes have not yet resolved at scale. The restraint is most acute in Africa, where even South Africa and Egypt — the region's largest healthcare economies — remain at early-stage robotic penetration relative to the depth of their surgical case volumes.

- Surgeon Training, Credentialing, and Theatre Efficiency Barriers:

"A hospital that buys a robotic system today cannot deploy it at full utilisation for 12 to 18 months."

Credentialing a surgeon cohort on a new robotic platform requires structured simulation training, proctored case observation, and independent practice certification — a process that consumes 6 to 18 months per surgeon group before full theatre utilisation is achieved. For hospitals procuring their first robotic system, this implementation lag creates a negative ROI window that generates institutional resistance at the CFO and board level. The restraint is compounded when hospitals adopt multiple platforms — each platform OEM runs an independent credentialing programme, creating parallel training obligations that strain anaesthesia and nursing theatre capacity. In Asia Pacific markets where robotic surgery is new to the hospital's surgical culture, training timelines extend further due to limited availability of qualified robotic surgery proctors.

- Regulatory Complexity for AI-Enabled and Software-Defined Robotic Features:

"AI features are the competitive battleground — and the longest regulatory waiting room."

AI-assisted robotic guidance modules — including autonomous vessel identification, real-time anatomical segmentation, and predictive instrument movement algorithms — are classified as Software as a Medical Device (SaMD) under FDA's Digital Health Center of Excellence framework and EU MDR Article 22. This creates independent regulatory review pathways, separate from the underlying robotic hardware clearance, that extend time-to-market for AI feature releases by 12 to 24 months relative to traditional device submissions. The burden falls disproportionately on smaller OEMs and AI platform developers with limited regulatory affairs capacity. Europe's MDR transition has already extended CE Mark timelines for medical software by an average of 18 months across the MedTech sector since 2021, creating a competitive advantage for incumbents with established regulatory infrastructure.

|

"Reimbursement alignment remains the single most critical enabler for accelerating robotic adoption in community hospital settings. Until payers consistently recognise the downstream savings of robotic-assisted laparoscopic procedures, capital budgeting conversations at the CFO level will remain difficult." |

|

— Dr. James Yoo, President, Society of American Gastrointestinal and Endoscopic Surgeons (SAGES) |

|

(Source: SAGES Annual Meeting, April 2024) |

What Opportunities Exist in the Surgical Robotics Market?

- Single-Use Instrument Adoption and Recurring Revenue Expansion:

"The capital sale is the door. The instrument stream is the business."

Single-use robotic instrument sets are the fastest-growing revenue category within the surgical robotics value chain, driven by infection control mandates and the elimination of reprocessing costs. CMR Surgical's Versius platform is purpose-designed around a single-use instrument model, generating predictable per-procedure revenue for both the OEM and the hospital. As robotic installed bases expand globally, the cumulative instrument consumable opportunity compounds — each new system installation creates a 10 to 15 year revenue tail of instrument set purchases. For OEMs, this transforms the financial model from capital sales cyclicality to subscription-equivalent recurring revenue, improving earnings quality and enterprise valuation multiples.

- AI Software Licensing and Data Monetisation:

"Robotic surgery generates the most valuable dataset in medical AI — structured procedural video at scale."

Every robotic surgical procedure generates high-resolution structured video, instrument telemetry, and outcome data that constitutes the training dataset for the next generation of AI surgical guidance algorithms. OEMs that capture, curate, and licence this data — within appropriate regulatory and consent frameworks — create a proprietary data moat that smaller competitors cannot replicate without equivalent installed base scale. Intuitive Surgical's Sync platform and Medtronic's AI surgical intelligence initiatives both reflect this strategic pivot: the robotic system is becoming the data collection infrastructure, and the software licence fee and analytics platform are becoming the margin-rich revenue layer. This opportunity is most pronounced in markets where Electronic Health Record integration with robotic platforms is advancing — the U.S., Germany, and Japan.

- Ambulatory Surgical Centre (ASC) Market Penetration:

"The next million robotic procedures won't happen in hospitals."

Ambulatory surgical centres are the fastest-growing care setting for elective surgical procedures in North America and Europe, driven by cost structure advantages over inpatient hospital settings and CMS's ongoing expansion of procedures approved for outpatient reimbursement. Robotic platforms have historically been hospital-centric due to capital cost and support infrastructure requirements. Second-generation platforms — designed for smaller physical footprints, faster room-to-room turnaround, and reduced service dependency — are unlocking ASC penetration for the first time at scale. The U.S. ASC market represented a largely untapped robotic opportunity as of 2024. The first OEM to establish dominant ASC positioning through financing innovation, compact platform design, and procedure-type reimbursement optimisation will capture a structurally new revenue cohort outside the hospital procurement cycle.

- Outcome-Based Reimbursement and Value-Based Contracting:

"The payer relationship is the untapped distribution channel for surgical robotics."

As CMS and commercial payers in the U.S. — and NHS England, NICE, and regional payers in Europe — expand value-based care contracting frameworks, hospitals that can demonstrate superior procedure outcomes for robotic versus conventional surgery gain a structural contracting advantage. Robotic programmes that generate measurable reductions in 30-day readmission, post-operative complication, and average length of stay create a documented value proposition that can be monetised in payer negotiations. This creates a feedback loop: robotic adoption improves outcomes, improved outcomes strengthen payer contracts, stronger contracts justify further robotic investment. Hospitals that build systematic outcome tracking infrastructure around their robotic programmes today are positioning for a contracting advantage that will materialise at payer renewal cycles in 2027 and 2028.

What Challenges Does the Surgical Robotics Market Face?

- Reimbursement Pathway Fragmentation Across Geographies:

"A procedure that pays in Detroit doesn't necessarily pay in Dortmund."

Reimbursement frameworks for robotic-assisted surgery vary fundamentally by geography — creating a patchwork of market access conditions that OEMs must navigate individually in each target country. In the U.S., robotic procedure reimbursement under Medicare DRGs is established for laparoscopic and urological applications but remains inconsistent for newer indications. In Germany, the G-DRG system categorises robotic procedures under the same DRG as conventional laparoscopic cases in many specialties, eliminating the financial premium that justifies hospital robotic investment. In Japan, MHLW reimbursement approval for specific robotic procedure codes is required before hospitals can recover costs — a process that typically lags FDA or CE Mark approval by 18 to 36 months. This fragmentation requires OEMs to maintain dedicated health economics and reimbursement teams in each major market, creating a cost burden that disadvantages smaller OEMs without established regulatory affairs infrastructure.

- Vendor Lock-In Architecture and Multi-Platform Resistance:

"No hospital CEO wants to run three incompatible robotic ecosystems."

Incumbent robotic platforms — particularly the da Vinci system — are architected to create deep ecosystem lock-in: proprietary instrument connectors, exclusive software licensing, and credentialing programmes that are non-transferable across platforms. For hospitals seeking to diversify their robotic vendor base or trial competing platforms, the switching cost is not merely financial — it includes parallel theatre scheduling, duplicate credentialing, and service infrastructure redundancy. This creates a structural barrier to new entrant adoption that is most acute in large teaching hospitals with established da Vinci programmes. New entrants must compete not just on clinical feature parity but on a credible ecosystem narrative — demonstrating that their platform can integrate with existing hospital workflow infrastructure without creating a parallel operational burden.

- Cybersecurity Risk in Connected Robotic Surgical Systems:

"A connected surgical robot is a networked medical device — and every networked device is a potential attack surface."

Modern robotic surgical platforms are fully networked: they transmit procedure data to cloud analytics platforms, receive software updates over connected infrastructure, and interface with hospital Electronic Health Record systems in real time. This connectivity creates cybersecurity exposure that was not present in earlier generations of standalone surgical equipment. FDA's Cybersecurity in Medical Devices guidance (2023) now requires OEMs to maintain a Software Bill of Materials (SBOM) and documented vulnerability disclosure and remediation process for all networked devices. Hospital IT procurement teams are increasingly scrutinising robotic vendor cybersecurity posture as part of capital purchase due diligence — creating a new evaluation dimension that pure clinical performance data cannot address. OEMs without mature cybersecurity infrastructure face procurement delays and reputational risk if connected device vulnerabilities are publicly disclosed.

Surgical Robotics Market: Report Scope

|

Report Name |

Global Surgical Robotics Market by Product Type, Application, End User & Region — Forecast 2026–2034 |

|

Market Size in 2025 |

USD 8,740 Mn |

|

Market Forecast in 2034 |

USD 34,820 Mn |

|

Growth Rate (CAGR) |

16.6% (2026–2034) |

|

Historical Data Period |

2019–2024 |

|

Base Year |

2025 |

|

Forecast Period |

2026–2034 |

|

Number of Pages |

300+ |

|

Tables & Figures |

80–110 tables, 60–80 figures (standard complexity, 3 segmentation dimensions) |

|

Report Code |

ZMR-10575 |

|

Report Format |

|

|

Delivery Format |

Digital Download |

|

Published Date |

May 2026 |

|

Research Methodology |

Primary Research (KOL interviews, surgeon surveys, hospital procurement data) + Secondary Research (FDA filings, company annual reports, regulatory databases, peer-reviewed journals) |

|

Key Companies Covered |

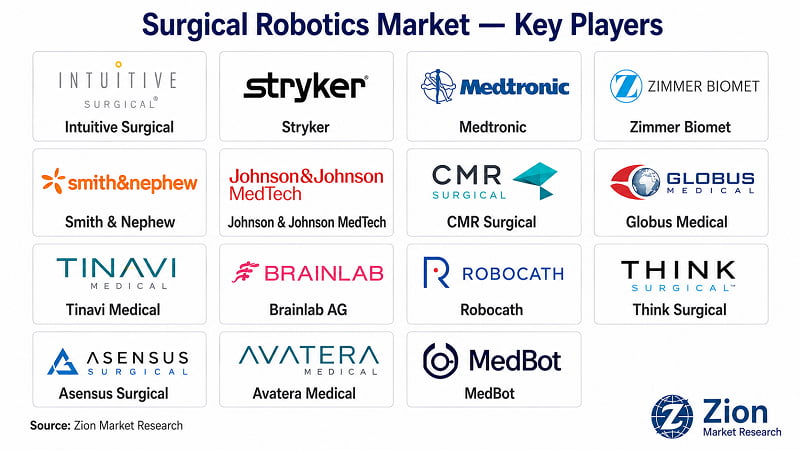

Intuitive Surgical, Stryker, Medtronic, Zimmer Biomet, Smith & Nephew, Johnson & Johnson MedTech, CMR Surgical, Globus Medical, Tinavi Medical, MedBot, Brainlab AG, Robocath, Think Surgical, Asensus Surgical, Avatera Medical |

|

Segments Covered |

By Product Type | By Application | By End User | By Region |

|

Regions Covered |

North America | Europe | Asia Pacific | Latin America | The Middle East | Africa |

|

Customization Scope |

Additional segments, specific country-level breakdowns, extended forecast to 2040, competitive benchmarking — contact sales@zionmarketresearch.com |

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Surgical Robotics Market: Segmentation

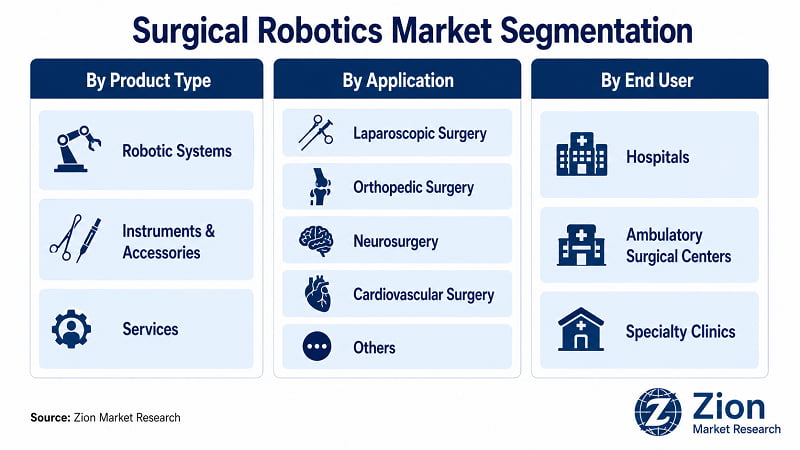

The global Surgical Robotics market is segmented by Product Type, Application, and End User.

- By Product Type

The product type dimension encompasses Robotic Systems, Instruments & Accessories, and Services. Robotic systems dominate this dimension, capturing approximately 58% of 2025 market revenue. The dominance mechanism is straightforward: capital system ASPs of USD 1 Mn to USD 2.5 Mn generate a high-value revenue event at installation, while the platform's proprietary instrument ecosystem creates a captive recurring revenue base. Instruments & Accessories is the fastest-growing sub-segment — driven by single-use instrument adoption policies, which eliminate reprocessing cost and infection risk at the price of higher per-procedure consumable expenditure. Intuitive Surgical's single-use EndoWrist instruments, introduced across its da Vinci Xi and SP platforms, demonstrate this model at scale. Services — including planned maintenance, software updates, and clinical training programmes — represent the highest-margin recurring revenue stream and are growing as installed base density increases globally.

- By Application

Applications span Laparoscopic Surgery, Orthopedic Surgery, Neurosurgery, Cardiovascular Surgery, and Others. Laparoscopic surgery holds the dominant application share at approximately 38% of 2025 revenue, reflecting the broad procedure portfolio — colorectal, urological, gynaecological — now routinely performed under robotic assistance. The dominance mechanism is established reimbursement and surgeon credentialing infrastructure across U.S. and European markets. Orthopedic Surgery is the fastest-growing application, driven by Stryker's MAKO platform expansion into total knee and total hip arthroplasty — a procedure category with structural demand growth from ageing population dynamics. Neurosurgery and cardiovascular surgery are emerging application frontiers where robotic platforms are demonstrating procedural feasibility but have not yet achieved the installed base density or reimbursement certainty that drives volume-scale adoption.

- By End User

End users are categorised as Hospitals, Ambulatory Surgical Centers (ASCs), and Specialty Clinics. Hospitals account for over 70% of demand, driven by the capital infrastructure, surgical volume, and payer contracting that justify multi-platform robotic programme investment. Teaching hospitals and large academic medical centres function as early-adopter anchors — their clinical trial data and published outcomes evidence drives downstream adoption in community hospital networks. ASCs are the fastest-growing end-user segment, as second-generation compact robotic platforms — CMR Surgical Versius, Medtronic Hugo — are specifically designed for the ASC's physical and operational constraints. Specialty clinics represent a niche segment today but are emerging as volume destinations for high-throughput robotic procedures in markets with ASC reimbursement parity.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Surgical Robotics Market: Regional Analysis

North America dominates the global Surgical Robotics market in 2025, capturing approximately 42% of global revenue. Asia Pacific is the fastest-growing region, driven by state-directed hospital infrastructure investment in China and India. The structural divergence between the two regions defines the market's geographic opportunity set: North America is a high-penetration, high-value-per-installation market; Asia Pacific is a high-volume, high-growth-rate market with structurally different procurement economics.

- North America Surgical Robotics Market

North America holds the dominant position in the global Surgical Robotics market, anchored by the U.S.'s unmatched combination of high surgical procedure volume, mature third-party reimbursement infrastructure, and the world's highest concentration of academic medical centres functioning as early-adopter accounts for robotic OEMs. CMS's value-based care payment evolution is actively incentivising hospital investment in robotic platforms that demonstrate measurable outcome improvements. Canada contributes to regional growth through provincial health authority robotic procurement programmes in Ontario, British Columbia, and Alberta, where public hospital systems have approved robotic surgery capital budgets as part of surgical backlog reduction strategies following the COVID-19 procedure deferral period. Mexico presents an emerging opportunity through private hospital networks that are deploying robotic systems to differentiate their premium surgical service offerings. The primary challenge for North America is market saturation at the top tier: large teaching hospitals are already multi-platform robotic environments, and the next growth wave requires successful penetration of community hospitals and ASCs — a lower-ASP, higher-volume market segment.

- Europe Surgical Robotics Market

Europe holds the second-largest regional revenue share in the global Surgical Robotics market, led by Germany and the U.K. Germany's academic hospital sector has been an early and sustained adopter of robotic-assisted surgery, with the G-DRG reimbursement system's ongoing review of robotic-specific procedure codes representing the critical policy variable for the next phase of adoption. The U.K.'s NHS has formalised robotic surgery procurement through its Robotic Surgery Programme, with CMR Surgical's Versius system gaining significant NHS penetration across general surgery applications. France, Italy, and Spain contribute material volume through both public and private hospital robotic programmes. The EU MDR regulatory transition has created certification backlogs that have delayed new product launches by 12 to 24 months across the MedTech sector — a structural challenge for European market entry timelines. Russia's share has contracted materially since 2022 due to import restrictions and geopolitical disruption to MedTech supply chains.

- Asia Pacific Surgical Robotics Market

Asia Pacific is the fastest-growing region in the global Surgical Robotics market through 2034. China's Healthy China 2030 national plan is the primary demand catalyst: the National Healthcare Commission has directed capital investment for robotic surgery capability across tier-2 and tier-3 hospitals at a scale that dwarfs any other government-driven healthcare technology programme globally. Tinavi Medical and MedBot are capturing a growing share of this domestic procurement wave through local content preference advantages and government-aligned pricing. Japan contributes high-value installed base additions across its advanced surgical hospital network, with MHLW reimbursement approval for specific robotic procedure codes accelerating adoption in laparoscopic and urological applications. South Korea's high per-capita healthcare expenditure and advanced hospital infrastructure support continued robotic platform adoption across academic and private hospital sectors. India's AIIMS network and private hospital chains — Fortis, Apollo, Max Healthcare — represent a growing demand cohort, though price sensitivity constrains platform ASPs below North American and European levels.

- Latin America Surgical Robotics Market

Latin America is an emerging growth market for surgical robotics, led by Brazil, which accounts for the dominant share of regional robotic installed base through its concentrated private hospital sector in São Paulo and Rio de Janeiro. Medtronic's Hugo system has specifically targeted Latin American hospital networks with competitive pricing structures and local clinical education programmes. Colombia and Chile represent secondary growth markets through their expanding private healthcare infrastructure and growing medical tourism sectors where robotic surgery differentiates service offerings. The primary regional challenge is the high cost of imported robotic systems in markets with currency depreciation pressures and limited manufacturer financing programmes — factors that constrain adoption to the upper tier of private hospital operators.

- The Middle East Surgical Robotics Market

The Middle East is an accelerating market for surgical robotics, driven primarily by GCC healthcare infrastructure investment under Saudi Arabia's Vision 2030 and UAE's National Strategy for Advanced Technology. Saudi Arabia is establishing dedicated robotic surgery centres in Riyadh and Jeddah, with government procurement programmes targeting both installed system expansion and local clinical training capacity development. The UAE — particularly Abu Dhabi's Cleveland Clinic and Burjeel Holdings network — has deployed multi-platform robotic surgery programmes targeting medical tourism revenue from regional markets. Israel contributes advanced medtech development activity, with several Israeli robotic surgery startups in pre-commercial or early commercial stages targeting global markets. Turkey presents a growing market through its expanding private hospital sector and medical tourism infrastructure. The Middle East market is assessed independently from Africa across all analytical dimensions in this report.

- Africa Surgical Robotics Market

Africa represents an early-stage but strategically significant frontier for surgical robotics. South Africa leads the continent's robotic installed base through its established private hospital networks — Mediclinic, Life Healthcare, and Netcare — which have deployed robotic systems in high-volume laparoscopic and urological programmes in Johannesburg and Cape Town. Egypt's healthcare modernisation programme includes robotic surgery capability development in its network of new university hospitals. Nigeria, Kenya, and Ethiopia represent longer-term growth opportunities as healthcare infrastructure investment expands, though robotic surgery adoption remains constrained by capital availability, service infrastructure limitations, and the surgical volume thresholds required to justify platform investment. The continent's primary challenge is not demand — the surgical disease burden is substantial — but financial access and the absence of reimbursement frameworks that de-risk robotic capital investment for hospital operators.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Full Country Coverage

|

Region |

|

|

North America |

The U.S., Canada, Mexico |

|

Europe |

Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe |

|

Asia Pacific |

China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific |

|

Latin America |

Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America |

|

The Middle East |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

Africa |

South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa |

**Country-level market sizing, historical data, and forecasts available for all geographies listed. Custom regional add-ons available — contact sales@zionmarketresearch.com

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Surgical Robotics Market: Competitive Landscape

- The global Surgical Robotics market is moderately consolidated at the platform layer, with Intuitive Surgical retaining the dominant installed base share in soft tissue surgery through its da Vinci ecosystem. Below the platform tier, the competitive landscape is fragmented across instrument manufacturers, AI navigation developers, and service network providers. The dominant strategic pattern among second-generation entrants is price-performance positioning: offering da Vinci-comparable clinical outcomes at a 30–40% lower system acquisition cost, with the goal of expanding the addressable market into community hospital and ASC settings that the da Vinci's cost structure has historically excluded.

- Key players operating in the global Surgical Robotics market include Intuitive Surgical, Inc. (U.S.), Stryker Corporation (U.S.), Medtronic plc (Ireland), Zimmer Biomet Holdings (U.S.), Smith & Nephew plc (U.K.), Johnson & Johnson MedTech (U.S.), CMR Surgical (U.K.), Globus Medical (U.S.), Tinavi Medical Technologies (China), MedBot (China), Brainlab AG (Germany), Robocath (France), Think Surgical (U.S.), Asensus Surgical (U.S.), and Avatera Medical (Germany).

|

Company |

HQ Country |

Primary Focus |

Key Strategy |

Notable Recent Action |

|

Intuitive Surgical |

U.S. |

Soft Tissue Robotic Surgery |

Platform ecosystem lock-in; AI software licensing |

Launched Ion endoluminal system; expanded da Vinci 5 globally in 2024 |

|

Stryker |

U.S. |

Orthopaedic Robotics (MAKO) |

Expand MAKO indications; bundled device-service contracts |

MAKO total hip and knee installed base exceeded 2,000 globally in 2024 |

|

Medtronic |

Ireland |

Multi-specialty (Hugo RAS) |

Price-competitive alternative to da Vinci in EU and emerging markets |

Hugo commercial expansion across European and Latin American hospitals 2022–2024 |

|

Zimmer Biomet |

U.S. |

Orthopaedic (ROSA) |

Joint replacement robotics for spine and knee |

ROSA Knee system CE Mark expansion in 2024 for additional European markets |

|

Smith & Nephew |

U.K. |

Orthopaedic Robotics (CORI) |

Handheld robotic system for knee replacement — portability advantage |

CORI system deployed in over 600 global sites as of 2024 |

|

J&J MedTech |

U.S. |

Multi-specialty (OTTAVA) |

Ecosystem integration with DePuy Synthes and Ethicon instruments |

FDA clearance received for OTTAVA general surgery indication, late 2024 |

|

CMR Surgical |

U.K. |

Laparoscopic Surgery (Versius) |

Modular, portable design for ASC and community hospital penetration |

100th global hospital deployment milestone reached, October 2024 |

|

Globus Medical |

U.S. |

Spine Robotics (ExcelsiusGPS) |

Spine navigation and robotics integration for complex deformity cases |

Merger with NuVasive created largest spine robotics portfolio globally in 2024 |

|

Tinavi Medical |

China |

Orthopaedic Robotics (TINAVI) |

China government procurement; local content advantage |

40%+ expansion in domestic hospital clients reported 2022–2024 |

|

Brainlab AG |

Germany |

Surgical Navigation & AI |

Platform-agnostic AI navigation layer for existing robotic systems |

Brainlab Spine & Trauma Navigation expanded to 50+ countries by 2024 |

- Three strategic themes define the competitive set: (1) Ecosystem depth versus portability — Intuitive Surgical and J&J MedTech are building deep instrument and software ecosystems, while CMR Surgical and Asensus Surgical are prioritising compact, portable platforms for non-hospital settings. (2) AI differentiation — every major OEM is investing in AI-guided features as the primary next-generation competitive differentiator. (3) Geographic expansion — Chinese domestic OEMs are insulating their market position behind local content policies, while European OEMs are targeting emerging market hospital modernisation programmes as growth vectors outside the saturating North American market.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Recent Developments in the Surgical Robotics Market

Strategic activity in the global Surgical Robotics market has accelerated through 2024 and into 2025, with major OEMs pursuing regulatory clearances, commercial expansions, and acquisition-driven portfolio consolidation at pace.

|

Date |

Company |

Type |

Description |

Market Impact |

|

Jan 2025 |

J&J MedTech |

Regulatory |

FDA clearance for expanded OTTAVA laparoscopic general surgery indication |

Broadens addressable procedure scope; intensifies competition with da Vinci in general surgery |

|

Oct 2024 |

CMR Surgical |

Commercial |

100th global hospital deployment of Versius system, anchored by NHS adoption |

Validates community hospital and NHS market penetration strategy |

|

Jun 2024 |

Stryker |

Acquisition |

Acquisition of Inari Medical to expand vascular intervention portfolio |

Strengthens robotic-adjacent procedural scope beyond orthopaedics |

|

Apr 2024 |

Intuitive Surgical |

Product Launch |

da Vinci 5 global commercial launch with AI-enhanced visualisation and instrument force feedback |

Raises the technical benchmark across the robotic surgery category |

|

Mar 2024 |

Globus Medical / NuVasive |

Merger |

Integration completed creating the largest dedicated spine robotics portfolio globally |

Creates a dominant spine robotics platform and consolidates competitive pressure on Medtronic spine robotic unit |

|

Nov 2023 |

Medtronic |

Commercial |

Hugo RAS system commercial expansion into Latin American hospital networks |

Establishes Medtronic competitive presence in growth-priority emerging markets |

About Zion Market Research

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is updated constantly in order to fulfil our clients' requirements for prompt and direct online access. Keeping in mind the client's needs, we have included expert insights on global industries, products, and market trends in this database.

Author:

Mr. Nilesh Patil

Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067

Table Of Content

Methodology

FrequentlyAsked Questions

The Zion Market Research's Surgical Robotics market report provides 300+ pages of in-depth market intelligence covering: global and regional market sizing from 2019 to 2034; segmentation analysis by Product Type (3 sub-segments), Application (5 sub-segments), and End User (3 sub-segments); competitive landscape analysis with profiles of 15 key companies; country-level data for 35+ geographies across 6 regions; DROC analysis (Drivers, Restraints, Opportunities, Challenges); and a full research methodology section. The report is delivered in PDF format.

The global Surgical Robotics market was valued at USD 8,740 Mn in 2025 and is projected to reach USD 34,820 Mn by 2034, growing at a compound annual growth rate (CAGR) of 16.6% during 2026–2034. Historical data in this report covers 2019 through 2024, with the base year set at 2025. (Source: Zion Market Research)

The Zion Market Research's Surgical Robotics report segments the market across three primary dimensions. By Product Type: Robotic Systems, Instruments & Accessories, and Services. By Application: Laparoscopic Surgery, Orthopedic Surgery, Neurosurgery, Cardiovascular Surgery, and Others. By End User: Hospitals, Ambulatory Surgical Centers, and Specialty Clinics. Each dimension includes historical sizing, CAGR, dominant sub-segment analysis, and 2034 forecast.

This report provides country-level data for 35+ geographies across six separate regional analyses: North America (The U.S., Canada, Mexico); Europe (Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe); Asia Pacific (China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific); Latin America (Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America); The Middle East (GCC: Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman; Israel, Turkey, Iran, Rest of Middle East); Africa (South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa).

Zion Market Research offers full report customization including: additional market segments or sub-segment breakdowns not included in the standard scope; country-specific deep-dive analyses with granular city or state-level data; extended forecast horizons to 2040; competitive benchmarking for specific vendors; and custom primary research focused on specific buyer personas or geographies. Contact sales@zionmarketresearch.com or call +1 (302) 444-0166 to discuss custom scope and pricing.

List of Contents

Surgical Robotics Market Industry Perspective:Surgical Robotics OverviewKey InsightsWhy Choose the Zion Market ResearchsMarket Report?Surgical RoboticsDynamics (Drivers, Restraints, Opportunities, Challenges)Surgical Robotics Report ScopeSurgical Robotics SegmentationSurgical Robotics Regional AnalysisFull Country CoverageSurgical Robotics Competitive LandscapeRecent Developments in theMarketHappyClients