Generative AI in Healthcare Market Size, Share & Trends 2020-2034

Generative AI in Healthcare Market By Component (Solutions and Services), By Function (Medical Imaging & Diagnostics, Drug Discovery & Development, Clinical Documentation & Administrative Automation, Personalized Medicine & Treatment Planning, Robot-Assisted Surgery, and Others), By Application (Clinical and Non-Clinical), By End-Use (Healthcare Providers, Pharmaceutical & Biotechnology Companies, Healthcare Payers, and Others), By Deployment (Cloud-Based and On-Premise), By Technology (Large Language Models (LLMs), Natural Language Processing (NLP), Computer Vision, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2026–2034-

| Market Size in 2025 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 1,842 Million | USD 21,640 Million | 31.4% | 2025 |

INDUSTRY PERSPECTIVE

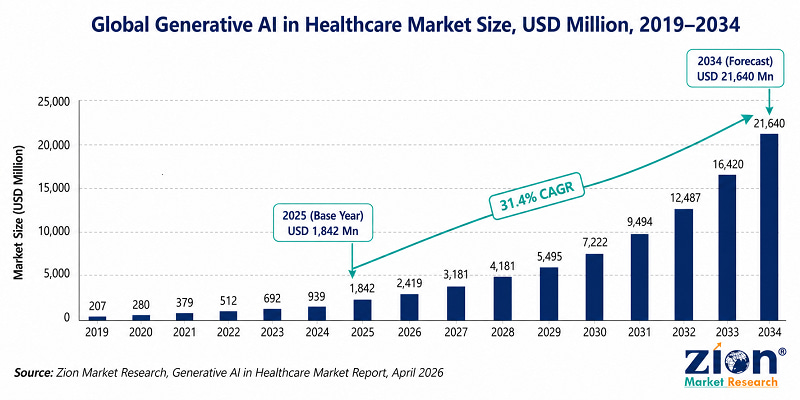

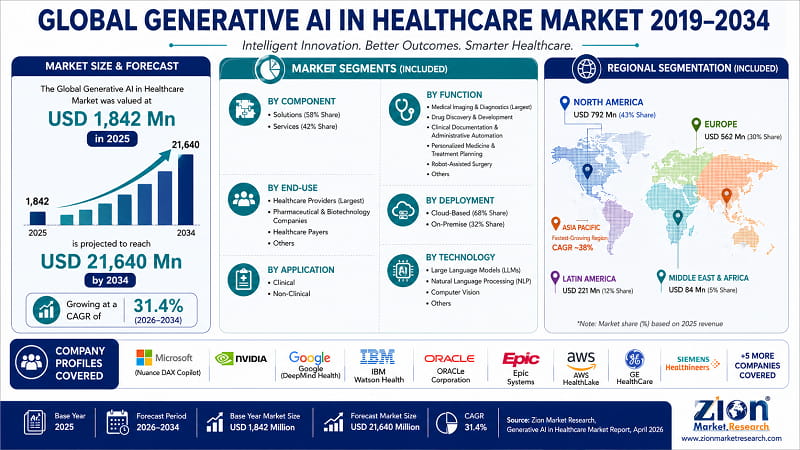

- The global Generative AI in Healthcare market size was valued at USD 1,842 million in 2025 and is predicted to reach USD 21,640 million by 2034, expanding at a CAGR of 31.4% during the forecast period 2026–2034, according to Zion Market Research. The absolute growth of USD 19,798 million over nine years — an 11.75x increase from the 2025 base — makes this one of the fastest absolute-value growth markets in the global Healthcare IT market sector.

- Generative AI in healthcare encompasses AI systems built on large language models (LLMs), diffusion models, graph neural networks, and other generative architectures that produce new clinical content, molecular structures, medical images, administrative documents, and patient communication outputs. The market's growth is not linear — it is characterised by discrete capability breakthroughs that drive step-change adoption events: an FDA clearance for a radiology AI tool, a Phase II clinical trial success for an AI-designed drug candidate, or an enterprise EHR platform embedding ambient AI scribing natively. Each such event expands the addressable market faster than gradual technology maturation curves.

- Healthcare executives, health system CIOs, pharmaceutical R&D strategy teams, and investors assessing the generative AI in healthcare opportunity should note that the market's 31.4% CAGR through 2034 reflects a genuine structural transformation — not a technology valuation premium. The clinical validation milestones achieved in medical imaging and drug discovery between 2023 and 2025 have converted this from an experimental category into a defensible enterprise procurement decision with documented ROI.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Key Insights

- The global Generative AI in Healthcare market is projected to grow at a CAGR of 31.4% from 2026 to 2034, reaching USD 21,640 million from a base of USD 1,842 million in 2025 — an 11.75x expansion, according to Zion Market Research

- The Solutions segment accounts for approximately 58% of market revenue in 2025, driven by healthcare providers' preference for integrated, EHR-compatible AI platforms over standalone point solutions

- Medical Imaging & Diagnostics is the leading functional segment, propelled by FDA-cleared AI radiology tools reducing radiologist report turnaround by 40–60% and false negative rates in cancer screening

- Clinical Documentation & Administrative Automation is the fastest-growing functional segment — ambient AI scribing tools generated approximately USD 600 million in U.S. revenue in 2025, growing 2.4x year-on-year

- Healthcare Providers are the dominant end-use segment (~47% share), driven by hospital IT procurement for clinical workflow AI; Pharmaceutical & Biotechnology Companies are the fastest-growing end-use

- Cloud-Based deployment accounts for approximately 68% of market revenue, driven by the scalability advantages of cloud AI infrastructure for hospital networks and pharma research environments

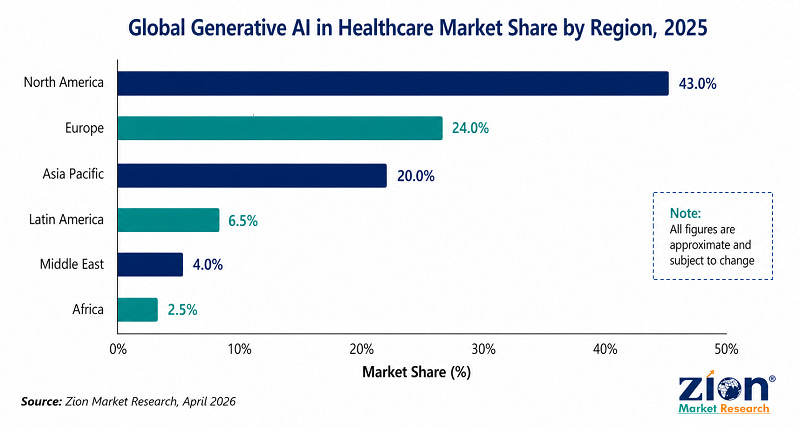

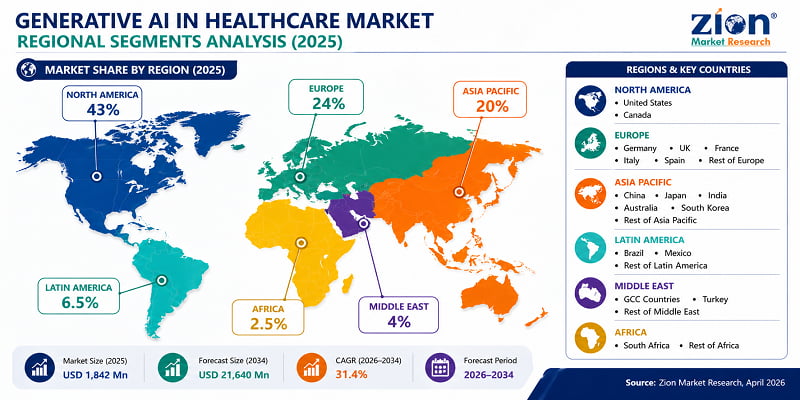

- North America leads with ~43% global revenue share in 2025; Asia Pacific is the fastest-growing region at ~38% CAGR, driven by China, Japan, India, and South Korea government AI investment

- The market has produced 8 healthcare AI unicorns — more than any other vertical AI segment including legal, financial services, and media — signalling deep commercial conviction

- Regulatory complexity (FDA SaMD pathways, EU AI Act high-risk classification, HIPAA/GDPR constraints) remains the primary adoption barrier across all regions — but compliance frameworks are maturing faster than sceptics predicted

WHY THIS REPORT?

Decision-makers evaluating market intelligence reports on generative AI in healthcare will find significant variation in depth, forecast horizon, and segmentation granularity across available options. The Zion Market Research report is differentiated on the following dimensions:

|

Dimension |

ZMR Report |

Industry Average |

|

Report Pages |

300 pages |

~120 pages |

|

Forecast Horizon |

9 years (2026–2034) |

7 years (2026–2033) |

|

Segmentation Dimensions |

6 (Component, Function, Application, End-Use, Deployment, Technology) |

4–5 dimensions |

|

Historical Data Coverage |

2020–2025 (6 years) |

2021–2025 (4–5 years) |

|

Country-Level Forecasts |

18 countries |

15–18 countries |

|

Companies Profiled |

15 companies with strategic analysis |

10–12 company profiles |

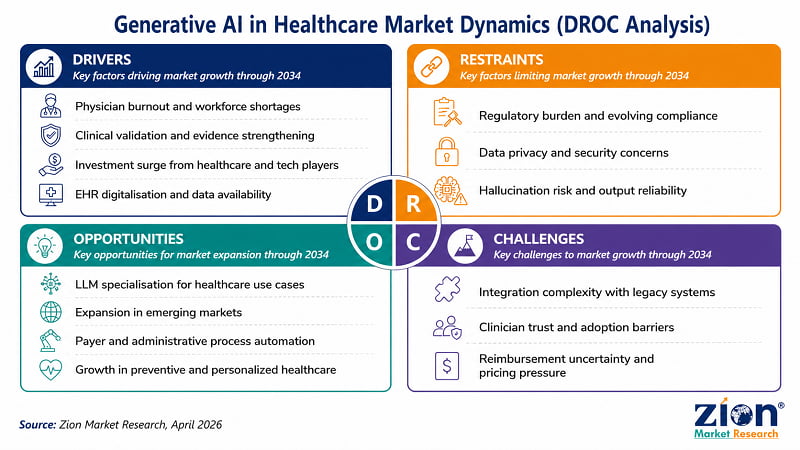

Generative AI in Healthcare Market: Dynamics (Drivers, Restraints, Opportunities, Challenges)

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

What Is Driving the Global Generative AI in Healthcare Market?

Driver 1: Physician Burnout and Clinical Administrative Automation Imperative

- The documentation burden on clinicians has reached a systemic crisis point — and the financial and human cost is driving procurement decisions at a pace that regulatory caution alone cannot contain.

- According to Medscape's 2024 Physician Burnout and Depression Report, 49% of U.S. physicians reported burnout — with 62% citing administrative tasks and documentation requirements as the primary cause. Physicians spend approximately one hour on documentation for every five hours of patient care, a ratio that generates what industry professionals term 'pajama time': evenings spent completing notes rather than delivering care or recovering from clinical workload. The American Hospital Association estimates that administrative complexity costs the U.S. healthcare system USD 265 billion annually. Ambient AI scribing — generative AI tools that listen to doctor-patient conversations and automatically generate structured clinical notes in EHR format — addresses this problem directly, with documented ROI visible within 90 days of deployment. Nuance DAX Copilot, Abridge, and Ambience collectively generated approximately USD 600 million in U.S. revenue in 2025. That is not a market — that is a validated enterprise software category growing at 2.4x annually.

Driver 2: Clinically Validated Performance in Medical Imaging and Drug Discovery

- Two functional areas have cleared the clinical validation threshold that separates experimental AI from enterprise procurement: medical imaging and drug discovery.

- In medical imaging, FDA-cleared AI tools from companies including Aidoc, Viz.ai, iCAD, and Paige AI now outperform human specialists on specific diagnostic tasks — detecting pulmonary embolism in CT scans, identifying diabetic retinopathy in fundus images, flagging suspicious lesions in mammograms — with documented reductions in false negatives and report turnaround times. The clinical evidence base that underpins these clearances is now robust enough to satisfy hospital medical committees and insurance reimbursement requirements. In drug discovery, Insilico Medicine's AI-designed drug candidate INS018_055 reached Phase II clinical trials in 2024, validating the end-to-end generative AI drug discovery pipeline at institutional level. Eli Lilly's June 2024 partnership with OpenAI to use generative AI for antimicrobial drug discovery, and AstraZeneca's investment in generative AI molecular design, confirm that Big Pharma has moved past pilot programmes into strategic R&D commitment.

Driver 3: Surge in Healthcare AI Investment and Ecosystem Infrastructure Maturation

- The investment environment funding generative AI in healthcare in 2025 bears no resemblance to the speculative healthcare AI investments of 2018–2020.

- Healthcare AI spending reached USD 1.4 billion in 2025 — nearly tripling 2024's investment — and according to Menlo Ventures, only horizontal chatbots and coding assistants are expanding faster across the entire enterprise AI landscape. Eight healthcare AI unicorns exist as of 2025, more than any other vertical AI segment. The ecosystem infrastructure that early AI deployments lacked — HIPAA-compliant cloud infrastructure (AWS HealthLake, Azure Health Data Services, Google Cloud Healthcare API), pre-built EHR integration layers (Epic's AI App Marketplace, Oracle Cerner SMART on FHIR), and validated LLMs purpose-built for clinical language (Google Med-PaLM 2, Microsoft BiomedCLIP, NVIDIA BioNeMo) — is now commercially available. The technical barrier to AI deployment in healthcare has fallen dramatically from 2021 to 2025.

Driver 4: Accelerating Healthcare Digitalisation and EHR Data Availability

- Generative AI systems require large, structured datasets of clinical data to achieve performance levels that justify deployment — and for the first time, that data infrastructure exists at scale.

- In the U.S., EHR adoption rates among hospitals now exceed 96%, creating the standardised structured clinical data repositories that AI training and inference require. The 21st Century Cures Act and ONC's interoperability regulations have opened API-based access to patient data across health systems, enabling AI systems to access longitudinal patient records that were previously siloed. In Europe, the European Health Data Space (EHDS) initiative is creating a regulatory framework for cross-border health data access that will further expand the training dataset available to generative AI developers. This data infrastructure maturation is a prerequisite for the medical imaging, personalised medicine, and drug discovery applications that are driving the market's highest CAGR segments.

What Is Restraining the Global Generative AI in Healthcare Market?

Restraint 1: Regulatory Validation Burden for Clinical AI Applications

- The regulatory pathway for generative AI in clinical settings remains one of the most complex technology approval processes in any industry — and it is slowing the commercial deployment of clinically validated AI systems.

- The FDA's AI/ML-based Software as a Medical Device (SaMD) framework requires clinical AI systems to demonstrate safety and efficacy through pre-market submissions — 510(k) clearance for devices with predicate devices, De Novo classification for novel AI functions. As of 2024, the FDA had cleared over 950 AI/ML-enabled medical devices, but the review timeline averages 12–24 months, creating a deployment lag between AI capability development and market availability. The EU AI Act, which came into force in August 2024, classifies healthcare AI systems as high-risk under Annex III, imposing conformity assessment obligations, mandatory transparency and explainability documentation, and post-market monitoring requirements that increase regulatory compliance costs by an estimated USD 50,000–500,000 per AI system per market. For AI startups targeting European hospitals, this cost creates a market entry barrier that disproportionately favours well-capitalised incumbents.

Restraint 2: Healthcare Data Privacy Regulations and AI Training Constraints

- Access to the large-scale, high-quality clinical training datasets that generative AI systems require is constrained by the most comprehensive data privacy regulatory framework of any industry.

- HIPAA's minimum necessary standard and de-identification requirements place strict constraints on the use of PHI in AI training — hospitals must use Business Associate Agreements (BAAs) with AI vendors, implement strict access controls, and document data flows that satisfy HIPAA's audit requirements. In Europe, GDPR Article 9's special category protections for health data, combined with national supervisory authority enforcement actions (the French CNIL's EUR 1.5 million fine of Doctissimo for health data processing violations in 2023), have created a climate of regulatory risk aversion that slows AI vendor contracting timelines. Health systems that have attempted to build proprietary training datasets from their patient populations have faced institutional review board (IRB) scrutiny and patient advocacy challenges that delay timeline by 12–18 months.

Restraint 3: AI Hallucination Risk in Clinical Settings and Clinician Trust Deficit

- The technical limitation that defines generative AI — the tendency to produce plausible-sounding but factually incorrect outputs, known as hallucination — is uniquely dangerous in clinical settings and is slowing deployment beyond administrative functions.

- A 2024 study published in JAMA showed that GPT-4 produced clinically significant errors in approximately 8% of clinical reasoning tasks when used without physician oversight. For ambient scribing and administrative automation applications, hallucination rates are manageable with human review. For clinical decision support, diagnostic AI, and treatment planning applications — where an incorrect AI output could directly harm a patient — hallucination risk is a significant barrier to deployment without physician verification workflows that negate much of the efficiency gain the AI was intended to deliver.

What Opportunities Exist in the Global Generative AI in Healthcare Market?

Opportunity 1: Healthcare-Specific LLM Development and Clinical Foundation Models

- The most immediate and defensible opportunity in generative AI in healthcare is not building general AI that happens to work in healthcare — it is building AI that was designed specifically for clinical language, clinical reasoning, and clinical evidence standards from the ground up.

- Google's Med-PaLM 2, trained on medical licensing exam content and clinical literature, achieved expert-level performance on U.S. Medical Licensing Examination (USMLE) questions in 2023 — the first AI system to do so. Microsoft's BiomedCLIP is specifically trained on biomedical image-text pairs from PubMed and clinical archives, enabling multimodal clinical reasoning that general-purpose models cannot match. The opportunity is substantial: healthcare-specific models command a significant pricing premium over general LLMs in enterprise procurement, because they reduce the fine-tuning and validation investment required to achieve clinical accuracy thresholds. The vendors who establish clinical foundation model benchmarks in specific specialties — radiology, pathology, oncology, cardiology — will create the healthcare AI equivalent of platform lock-in.

Opportunity 2: Healthcare Payer and Administrative Workflow Automation

- The healthcare payer segment — health insurance companies, government payers (Medicare, Medicaid, NHS), and managed care organisations — represents a large, structurally underserved generative AI opportunity.

- Prior authorisation, utilisation management, claims processing, and payment integrity together cost the U.S. healthcare system an estimated USD 35 billion annually in administrative labour. The payer segment's multi-year enterprise sales cycles and complex IT procurement requirements have made it a slower adopter of generative AI than provider organisations — but the organisations that navigate this sales complexity successfully are capturing contracts worth USD 10–50 million annually from single payers. AI agents that interface directly with provider AI agents to process prior authorisations — eliminating the phone and fax workflows that currently dominate this process — are expected to become the standard payer-provider interface within the forecast period.

Opportunity 3: Emerging Market Healthcare AI Deployment

- Asia Pacific, Latin America, The Middle East, and Africa represent generative AI in healthcare markets that are structurally different from North America and Europe — and may leapfrog Western adoption patterns in specific applications.

- India's All India Institute of Medical Sciences (AIIMS) deployed an AI system trained on 500,000 radiological and histopathological images in February 2024, targeting diagnostics in underserved Indian rural healthcare settings where specialist physician access is severely limited. Saudi Arabia's Vision 2030 digital health programme is investing billions in AI-enabled hospital infrastructure that will not be constrained by the legacy EHR systems that slow AI integration in U.S. and European hospitals. Brazil's rapidly expanding telemedicine infrastructure — COVID-19 accelerated telehealth adoption from 1.4% to 47% of outpatient consultations — creates a cloud-native AI deployment environment in which generative AI patient engagement tools can scale without the enterprise integration complexity that slows deployment in traditional hospital settings.

Opportunity 4: Preventive Health, Remote Patient Monitoring, and Chronic Disease Management

- The fastest-growing application of generative AI in healthcare globally is not hospital-based clinical AI — it is consumer-facing and remote patient monitoring AI that operates outside the hospital setting.

- Chronic disease management — diabetes, cardiovascular conditions, COPD, mental health — accounts for 90% of U.S. healthcare costs, yet is managed predominantly through reactive episodic care rather than proactive continuous monitoring. Generative AI-powered remote patient monitoring platforms that analyse continuous glucose monitor data, cardiac rhythm patterns, sleep data, and medication adherence signals to generate personalised health coaching, early warning alerts, and care team summaries represent the largest greenfield opportunity in the market. The global remote patient monitoring market, projected to reach USD 175 billion by 2034, is the primary adjacent demand pool for healthcare generative AI applications that are not subject to FDA Class II medical device approval pathways.

What Challenges Does the Global Generative AI in Healthcare Market Face?

Challenge 1: EHR Integration Complexity and Healthcare IT Legacy Infrastructure

- The healthcare IT infrastructure that generative AI systems must integrate with was not designed for AI — and retrofitting AI capabilities onto legacy EHR architectures is expensive, slow, and technically fragile.

- Epic Systems — which runs approximately 38% of U.S. hospital EHR infrastructure — has built an AI App Marketplace that standardises third-party AI integration, but vendors must pass Epic's certification process before reaching hospital customers. Cerner and Meditech have similar but differently structured integration requirements. For AI companies targeting multi-system hospital networks with heterogeneous EHR environments, integration can consume 40–60% of implementation project budgets before the AI application itself generates any clinical value. This integration complexity disproportionately disadvantages AI startups relative to incumbents who already have existing EHR partnerships, and creates sticky, long-term relationships for vendors who successfully complete integration — the competitive moat is in the integration, not in the AI model.

Challenge 2: Clinical AI Reimbursement Uncertainty

- The absence of clear, consistent reimbursement pathways for AI-assisted clinical services is one of the most significant structural barriers to widespread healthcare provider AI deployment in the U.S. and Europe.

- The Centers for Medicare and Medicaid Services (CMS) has created a New Technology Add-on Payment (NTAP) pathway for AI-enabled medical devices, but the process is cumbersome and has approved only a fraction of submitted AI applications. Commercial insurance reimbursement for AI-assisted procedures varies dramatically by payer, procedure code, and geography — creating revenue uncertainty for hospitals that invest in AI but cannot reliably predict whether AI-enhanced procedures will be reimbursed at a premium relative to standard care. In Europe, healthcare AI reimbursement frameworks are even less developed, with most national health systems still in pilot evaluation phases for AI-assisted clinical services.

Challenge 3: Clinician Adoption, Change Management, and Trust Building

- The technology procurement decision for clinical AI and the clinical adoption decision are fundamentally different problems — and the gap between the two is one of the most commonly underestimated challenges in healthcare AI implementation.

- Hospital CIOs and IT procurement teams can sign contracts for clinical AI tools; they cannot force clinicians to use them. Studies of AI-assisted clinical decision support tools consistently show adoption rates of 20–50% among eligible clinician users even after full deployment, reflecting physician concerns about AI accountability, liability, explainability, and workload disruption during transition periods. Clinicians who are already burned out resist learning new technology workflows — the tool intended to reduce burden can initially create it. Successful generative AI deployments in healthcare systematically invest in clinical champion programmes, mandatory training with practical case simulation, change management infrastructure, and real-time feedback loops between AI vendors and clinical users — investment that is rarely reflected in AI vendor pricing and is almost never budgeted by hospital IT teams at the outset.

Generative AI in Healthcare Market: Report Scope

|

REPORT ATTRIBUTE |

REPORT DETAILS |

|---|---|

|

Report Name |

Generative AI in Healthcare Market — Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2026–2034 |

|

Market Size in 2025 |

USD 1,842 Million |

|

Market Forecast in 2034 |

USD 21,640 Million |

|

Growth Rate (CAGR) |

31.4% (2026–2034) |

|

Historical Data Period |

2019–2024 |

|

Base Year |

2025 |

|

Forecast Period |

2026–2034 |

|

Number of Pages |

300+ |

|

Tables & Figures |

120 tables, 90 figures (AI-determined: complex market) |

|

Report Code |

ZMR-10546 |

|

Report Format |

|

|

Delivery Format |

PDF | Excel (confirm per report) |

|

Published Date |

May 2026 |

|

Research Methodology |

Primary Research (interviews with hospital CIOs, AI vendors, pharma R&D directors, regulatory experts, health insurers) + Secondary Research (FDA clearance databases, clinical trials registries, annual reports, peer-reviewed journals, government health IT publications) |

|

Key Companies Covered |

Microsoft Corporation (USA), NVIDIA Corporation (USA), Google LLC — DeepMind Health (USA), IBM Corporation — Watson Health (USA), Oracle Corporation (USA), Epic Systems Corporation (USA), Amazon Web Services — AWS HealthLake (USA), Nuance Communications — DAX Copilot (USA), GE HealthCare Technologies (USA), Siemens Healthineers AG (Germany), Insilico Medicine (Hong Kong / USA), Abridge AI Inc. (USA), Tempus AI Inc. (USA), Recursion Pharmaceuticals Inc. (USA), Hippocratic AI Inc. (USA) |

|

Segments Covered |

By Component, By Function, By Application, By End-Use, By Deployment, By Technology, By Region |

|

Regions Covered |

North America | Europe | Asia Pacific | Latin America | The Middle East | Africa (6 separate regions — never combined) |

|

Customization Scope |

Customized purchase options available. Contact sales@zionmarketresearch.com |

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Generative AI in Healthcare Market: Segmentation

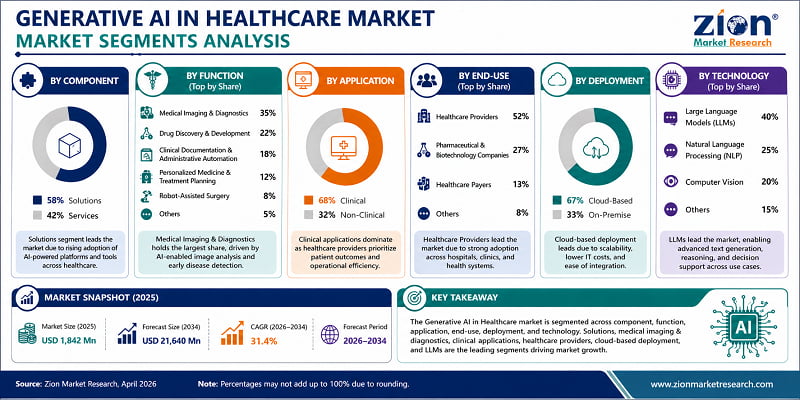

- The global Generative AI in Healthcare market is segmented by component, function, application, end-use, deployment mode, and technology. Each segmentation dimension reveals distinct dynamics that are critical for vendors targeting specific market entry points, investors assessing segment-level return profiles, and health system procurement teams evaluating capability breadth.

By Component

- The Solutions segment dominates with approximately 58% of market revenue in 2025, reflecting healthcare organisations' preference for integrated AI platforms over managed service engagements.

- Healthcare AI solutions — software platforms that embed generative AI into existing clinical and administrative workflows — offer complete EHR-compatible implementation with controllable data governance. Epic's AI-integrated platform, Oracle Cerner's generative AI features, and Microsoft Azure Health AI are all Solutions segment products that account for large per-contract revenue values. The Services segment — consulting, implementation, training, and managed AI service provision — is growing faster as healthcare organisations without internal AI expertise outsource deployment and ongoing management of AI systems. Cognizant, Accenture Health, and Deloitte Digital are among the fastest-growing Services segment players.

By Function

- Medical Imaging & Diagnostics leads the functional segment with the largest revenue share in 2025, driven by the high density of FDA-cleared AI imaging tools and the documented ROI of radiology AI in high-throughput diagnostic workflows.

- Clinical Documentation & Administrative Automation is the fastest-growing functional segment — ambient scribing tools (Nuance DAX Copilot: 33% market share, Abridge: 30%, Ambience: 13%) generated USD 600 million in 2025 U.S. revenue growing 2.4x year-on-year. Drug Discovery & Development is the highest-value segment on a per-contract basis, with pharma companies investing USD 50–200 million multi-year AI partnerships. Robot-Assisted Surgery is projected to be the fastest-growing segment through 2034, driven by the integration of generative AI into robotic surgical platforms including Intuitive Surgical's da Vinci 5 system, which incorporates AI-assisted surgical planning and real-time guidance features.

By Application

- Clinical applications account for approximately 70% of total market revenue — AI systems that directly support diagnosis, treatment planning, patient monitoring, and clinical documentation.

- Non-clinical applications — administrative automation (prior authorisation, billing, coding, scheduling), patient engagement, healthcare marketing, and compliance management — account for the remaining 30% but are growing faster due to the lower regulatory burden compared to clinical AI applications. The administrative AI category's growth is being driven by the USD 265 billion annual administrative cost burden in U.S. healthcare — a target addressable market that is larger than the entire current generative AI in healthcare market by a factor of 140.

By End-Use

- Healthcare Providers — hospital networks, integrated delivery networks (IDNs), clinics, and independent physician practices — are the dominant end-use segment with approximately 47% of market revenue in 2025.

- Pharmaceutical & Biotechnology Companies are the fastest-growing end-use segment, driven by the extraordinary ROI potential of AI-accelerated drug discovery: reducing a single drug from pre-clinical stage to Phase I clinical trial from USD 300–500 million and 4–6 years to USD 50–100 million and 18 months would create value that dwarfs any per-licence AI platform cost. Healthcare Payers are a nascent but rapidly emerging end-use segment as AI-enabled prior authorisation and utilisation management tools demonstrate ROI in commercial deployments.

By Deployment

- Cloud-Based deployment accounts for approximately 68% of market revenue, with Microsoft Azure, AWS, and Google Cloud Health APIs providing the dominant infrastructure platforms.

- Cloud deployment's dominance reflects the computational requirements of generative AI inference — LLM inference workloads are not economically feasible on most hospital on-premise infrastructure — and the maturation of HIPAA-compliant cloud environments that address health data residency requirements. On-premise deployment retains relevance for health systems with specific data sovereignty requirements (defence healthcare, government health systems), ultra-low-latency clinical applications (surgical robotics AI), and organisations operating under regulatory environments that restrict health data from leaving national borders.

By Technology

- Large Language Models (LLMs) are the dominant technology segment, underpinning the ambient scribing, clinical documentation, drug discovery, patient communication, and clinical decision support applications that drive the market's highest-volume adoption.

- Natural Language Processing (NLP) remains the foundational technology layer for EHR data extraction, clinical note analysis, and medical literature processing — LLMs are, in effect, a new generation of NLP built on transformer architectures. Computer Vision is the technology underpinning the medical imaging and pathology AI segment — convolutional neural networks and vision transformers analyse radiological images, histopathology slides, and ophthalmology scans at scale. Multimodal AI systems that combine LLM and Computer Vision capabilities — analysing both clinical notes and imaging data simultaneously — are the fastest-growing technology sub-segment and are expected to become the dominant architecture for clinical AI by 2030.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Key Market Segments Analysis Takeaway:

COMPONENT INSIGHTS

- Solutions Segment: 58% Revenue Share — The Dominant Component

The solutions segment dominated the global generative AI in healthcare market, accounting for approximately 58% of revenue in 2025. Healthcare providers' procurement preference for end-to-end AI platforms with native EHR integration drives this concentration. Organisations that have invested in EHR platform standardisation over the past decade are not willing to introduce AI point solutions that require custom API development and create parallel data governance obligations. End-to-end solutions from vendors with established EHR partnerships — Epic's AI App Marketplace, Oracle Cerner's SMART on FHIR integration layer, Microsoft's Azure Health Data Services — command the deployment pipeline for the most clinically significant AI functions.

In July 2025, Mayo Clinic deployed NVIDIA Blackwell-powered DGX SuperPOD infrastructure to accelerate generative AI and foundation model development for digital pathology and precision medicine initiatives — a deployment scale that signals enterprise conviction at one of the world's most credentialed medical institutions.

"This compute power, coupled with Mayo's unparalleled clinical expertise and platform data of over 20 million digitised pathology slides, will allow us to build on existing foundation models. We are transforming healthcare by quickly and safely developing AI solutions that improve patient outcomes and enable clinicians to dedicate more time to patient care."

— Jim Rogers, CEO, Digital Pathology Division, Mayo Clinic

- Services Segment: Fastest-Growing Component

The services segment is growing at the fastest rate within the component category. The complexity of clinical AI deployment — regulatory compliance documentation, EHR integration validation, ongoing model monitoring, and clinician change management — has created sustained demand for implementation, training, and managed services that AI software vendors cannot provide unilaterally. Healthcare organisations that lack in-house AI engineering capability, which includes the majority of health systems outside the top 50 by revenue, are dependent on services partners to convert software procurement into clinical deployment.

FUNCTION INSIGHTS

- Administrative Process Optimisation: 32.9% Share — the Largest Functional Segment

Administrative process optimisation accounts for approximately 32.9% of functional segment revenue in 2025, making it the single largest generative AI function in healthcare by commercial deployment. This category encompasses prior authorisation automation, clinical documentation, revenue cycle management, and patient scheduling — non-clinical workflows where AI accuracy requirements are lower than in diagnostic applications, enabling faster deployment and clearer ROI measurement. The American Hospital Association estimates that administrative complexity costs the U.S. healthcare system USD 265 billion annually — and AI automation of even 20% of this cost base represents a USD 53 billion revenue opportunity for AI vendors.

In October 2025, Microsoft expanded Dragon Copilot with ambient and generative AI capabilities for nursing workflows and partner integrations, extending clinical documentation automation beyond physician use cases to nursing staff — a segment that represents a larger headcount and documentation volume than physician-facing tools.

- Medical Imaging Analysis: Fastest-Growing Function

The AI in medical imaging analysis segment is growing at the fastest CAGR within the function category. AI models analysing radiology, pathology, and cardiology images have achieved or exceeded specialist performance benchmarks on specific diagnostic tasks, and the FDA's clearance of over 950 AI/ML-enabled medical devices through 2024 provides the regulatory validation that hospital procurement committees require. Rad AI's USD 60 million Series C at a USD 525 million valuation in January 2025 confirms that investors view clinical imaging AI as the most commercially mature generative AI application in healthcare.

END-USE INSIGHTS

- Healthcare Providers: Dominant End-Use at ~47% Market Share

Healthcare providers — hospital networks, integrated delivery networks, ambulatory care organisations, and outpatient clinic groups — accounted for approximately 47% of total market revenue in 2025. Enterprise AI procurement at major health systems is now a board-level strategic initiative rather than an IT department evaluation. Northwestern Medicine's full enterprise rollout of DAX Copilot across its EHR system in August 2024 — covering all physician workflows across the network — represents the scale of commitment that is now defining the deployment standard for health systems in the top quartile of AI adoption.

In February 2026, Japan Community Healthcare Organization Osaka Hospital, in collaboration with Fujitsu Japan and Microsoft Japan, launched a generative AI programme to enhance clinical documentation, workforce efficiency, and governance frameworks across hospital operations — signalling that enterprise AI deployment is no longer a U.S.-only phenomenon.

- Pharmaceutical & Biotechnology Companies: Fastest-Growing End-Use

Pharmaceutical and biotechnology companies are the fastest-growing end-use segment, driven by the intersection of AI capability maturation and pharmaceutical R&D productivity pressure. The Drug Discovery Informatics market and broader AI in Drug Discovery market are expanding in direct response to pharmaceutical organisations' need to reduce time-to-candidate and preclinical failure rates. In March 2024, NVIDIA Healthcare launched over 25 generative AI microservices — including NIM and CUDA-X tools — enabling pharmaceutical, biotech, and healthcare organisations to accelerate drug discovery, genomics, imaging, and digital health workflows.

Generative AI in Healthcare Market: Regional Analysis

- North America leads the global generative AI in healthcare market in revenue terms, while Asia Pacific is the fastest-growing region with the most dynamic government AI investment programme. These two regions together account for approximately 63% of global demand. The remaining four ZMR regions — Europe, Latin America, The Middle East, and Africa — each exhibit distinct adoption patterns shaped by regulatory environments, healthcare system structure, and digital infrastructure maturity.

North America Generative AI in Healthcare Market

- North America is the world's most mature generative AI in healthcare market — and it got there not primarily through government mandate but through the convergence of physician burnout, advanced EHR infrastructure, and a venture capital ecosystem that funded the fastest-growing health AI company formation wave in history.

- The United States accounts for approximately 90% of North American market revenue. The country's 96%+ EHR adoption rate among hospitals, the interoperability mandates of the 21st Century Cures Act, and the presence of the world's leading AI research institutions and technology companies (Microsoft, Google, NVIDIA, Amazon) have created conditions for generative AI deployment that no other geography can fully replicate in the short term. Eight healthcare AI unicorns exist in the U.S. as of 2025. Canada's universal healthcare system is beginning to adopt AI-assisted clinical documentation and diagnostic imaging tools, with AI procurement accelerating in Ontario and British Columbia. Mexico's private hospital sector is emerging as an early AI adopter, supported by cross-border technology partnerships.

Europe Generative AI in Healthcare Market

- Europe is the world's second-largest generative AI in healthcare market, defined by a complex regulatory environment that simultaneously mandates data-driven healthcare innovation and constrains the data flows that AI training requires.

- Germany leads European adoption, with hospital AI procurement accelerating through the Hospital Future Act (Krankenhauszukunftsgesetz — KHZG), which allocated EUR 4.5 billion to hospital digitalisation including AI-compatible IT infrastructure. The U.K.'s NHS AI Lab and NHSX digital transformation programme have produced some of the most advanced AI clinical trial datasets in Europe, with the NHS's de-identified patient data reaching 55 million records — a training dataset advantage that is driving domestic AI company development. France and the Netherlands are significant markets for pharmaceutical R&D AI. Sweden and Denmark are notable for precision medicine AI investment aligned with national genomics research programmes. Poland and Czech Republic are emerging markets for hospital administrative AI.

Asia Pacific Generative AI in Healthcare Market

- Asia Pacific is the fastest-growing region in the global generative AI in healthcare market — and the diversity of adoption patterns across its constituent economies is one of the market's most analytically interesting dynamics.

- China's government has designated AI in healthcare as a strategic national technology priority, with the Ministry of Science and Technology's national AI plan committing USD 15+ billion in AI R&D funding that includes substantial healthcare applications. China's AI healthcare market benefits from a massive patient population, relatively centralised hospital data governance, and domestic AI champions including Alibaba Health AI and Tencent Doctorwork. Japan's ageing population — projected to be 33% over 65 by 2030 — creates structural demand for AI-assisted diagnostics, robot-assisted care, and elderly care management solutions that no other healthcare system faces at the same scale. India's AIIMS system deployment of AI diagnostic tools, South Korea's AI medical device regulatory acceleration programme, and Australia's digital health strategy are all expanding the region's AI healthcare market.

Latin America Generative AI in Healthcare Market

- Latin America is in the early-adoption phase of generative AI in healthcare, with Brazil and Colombia leading a market that is being built on the telemedicine infrastructure established during COVID-19.

- Brazil's telemedicine adoption increased from 1.4% to 47% of outpatient consultations during the pandemic — creating a cloud-native digital health infrastructure that AI applications can deploy on without the EHR integration complexity that slows adoption in traditional hospital settings. Brazil's pharma market — the 8th largest globally — is also driving AI adoption in clinical trial management, regulatory affairs automation, and post-market pharmacovigilance. Colombia and Argentina are emerging markets for AI-powered clinical documentation. Chile and Peru have smaller healthcare AI markets but are showing early adoption in radiology AI through private hospital groups.

The Middle East Generative AI in Healthcare Market

- The Middle East is one of the most ambitious generative AI in healthcare markets globally in policy terms — with GCC governments investing in AI-enabled healthcare infrastructure at a pace that is expected to accelerate through 2034.

- The UAE's National AI Strategy 2031 specifically targets healthcare as a primary AI application sector, with Dubai Health Authority and Abu Dhabi Department of Health running advanced AI pilots in diagnostic imaging, patient triage, and hospital operations management. Saudi Arabia's Vision 2030 includes a digital health strategy that incorporates AI-powered preventive health screening across its expanded primary care network. Israel is a disproportionately significant player in the global healthcare AI ecosystem relative to its market size — with companies including Aidoc (radiology AI triage), Medial EarlySign (preventive health AI), and Binah.ai (remote vital sign monitoring) exporting AI solutions globally from an Israeli R&D base. Turkey is developing an AI-enabled national health record system with diagnostic AI integration.

Africa Generative AI in Healthcare Market

- Africa represents the smallest ZMR regional market for generative AI in healthcare, but its fundamental healthcare challenges — severe physician shortages, high infectious disease burden, and limited specialist access in rural settings — create a compelling use case for AI-enabled diagnostic and patient care tools.

- South Africa leads the continent with private hospital AI procurement — Mediclinic and Netcare are evaluating AI-assisted radiology and clinical documentation tools. Egypt is investing in AI integration within its universal health insurance programme. Nigeria's healthcare system, constrained by a physician-to-patient ratio of 0.4 per 1,000 (compared to 2.6 in the U.S.), represents a structural use case for AI diagnostic tools that can extend limited clinical capacity — and early-stage companies including Ubenwa (neonatal health AI) and Omomi (child health AI) are building Africa-native healthcare AI products. Algeria and Morocco are receiving increasing attention from European AI healthcare companies as North African distribution channel expansion targets.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Key Regional Analysis Takeaway:

- North America: ~43% Global Revenue Share, ~29% CAGR

North America dominates the global generative AI in healthcare market, accounting for approximately 43% of revenue in 2025. The U.S. healthcare system's near-universal EHR adoption (exceeding 96% of hospitals), digitised clinical data infrastructure, and the deepest concentration of healthcare AI vendor development and deployment activity globally make it the primary commercial environment for generative AI. According to a study published in JAMA Network in December 2025, approximately 31.5% of U.S. hospitals had implemented generative AI integrated with EHR systems by 2024, with nearly 25% planning implementation within the following year.

Ambient scribing alone generated approximately USD 600 million in U.S. revenue in 2025, with more than 150 health systems documented as enterprise adopters. In November 2025, Sanofi's German operations confirmed systematic AI application across its drug discovery value chain at its German research sites — from target identification to clinical trial design — marking a decisive shift from pilot programmes to strategic R&D commitment in the European market.

- Asia Pacific: Fastest-Growing at ~38% CAGR

Asia Pacific is the fastest-growing region, projected to grow at approximately 38% CAGR through 2034. China's August 2025 national AI in healthcare guidelines target universal AI-enabled diagnostic and treatment assistance in primary care institutions by 2030, with mandatory AI integration in hospitals at or above the second tier to improve efficiency, accessibility, and patient outcomes. In February 2024, India's All India Institute of Medical Sciences deployed an AI platform trained on 500,000 radiological and histopathological images, targeting diagnostics in rural healthcare settings where specialist access is severely limited. South Korea's government AI investment programme and Japan's hospital digitalisation mandate are creating state-sponsored deployment pipelines that reduce the enterprise sales complexity that AI vendors face in market-driven healthcare systems.

Full Country Coverage: Zion Market Research Generative AI in Healthcare Market Report

The Zion Market Research Global Generative AI in Healthcare Market Report (2020–2034) provides country-level data, analysis, and forecasts for all of the following geographies.

|

REGION |

COUNTRIES COVERED IN THE ZMR REPORT |

|---|---|

|

North America |

The U.S., Canada, Mexico |

|

Europe |

Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe |

|

Asia Pacific |

China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific |

|

Latin America |

Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America |

|

The Middle East |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

Africa |

South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa |

|

NOTE: Country-level market sizing, historical data, and forecasts are available for all geographies listed. Custom regional add-ons available on request — contact sales@zionmarketresearch.com |

|

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Generative AI in Healthcare Market: Competitive Landscape

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

- The global generative AI in healthcare market is highly dynamic and spans three distinct competitive tiers that are rapidly converging through acquisition, partnership, and product expansion: foundational infrastructure providers, healthcare AI platform specialists, and clinical application startups.

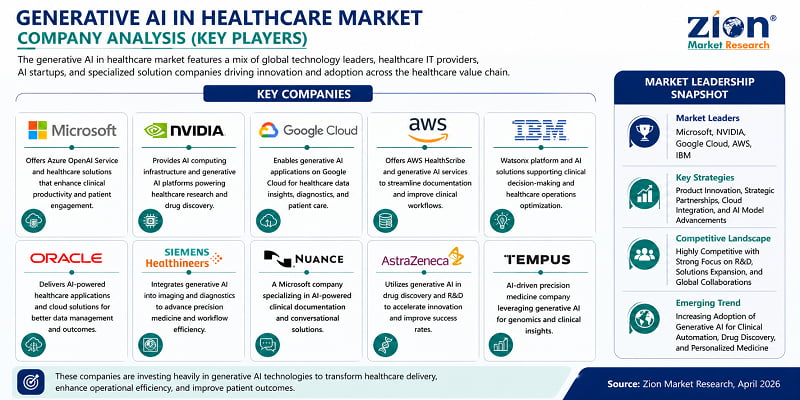

- Key players operating in the global Generative AI in Healthcare market include Microsoft Corporation (USA), NVIDIA Corporation (USA), Google LLC — DeepMind Health (USA), IBM Corporation — Watson Health (USA), Oracle Corporation (USA), Epic Systems Corporation (USA), Amazon Web Services — AWS HealthLake (USA), Nuance Communications — DAX Copilot (USA), GE HealthCare Technologies (USA), Siemens Healthineers AG (Germany), Insilico Medicine (Hong Kong / USA), Abridge AI Inc. (USA), Tempus AI Inc. (USA), Recursion Pharmaceuticals Inc. (USA), Hippocratic AI Inc. (USA), among others.

|

COMPANY |

HQ |

PRIMARY FOCUS |

KEY STRATEGY |

NOTABLE RECENT ACTION |

|---|---|---|---|---|

|

Microsoft (Nuance DAX Copilot) |

USA |

Ambient scribing, Clinical AI |

EHR integration + Azure Health |

Acquired Nuance USD 19.7 Bn; Copilot 33% scribe market |

|

NVIDIA |

USA |

AI Infrastructure / Drug Discovery |

BioNeMo + NVentures healthcare investments |

USD 137 Mn invested in Hippocratic AI, Oct 2024 |

|

Google LLC (DeepMind Health) |

USA |

Medical imaging, LLMs |

Med-PaLM 2, Vertex AI healthcare |

Roche partnership for oncology diagnostics, Mar 2024 |

|

IBM — Watson Health |

USA |

Clinical decision support, Admin AI |

Hybrid cloud + AI integration |

IQVIA AI assistant launch, Oct 2024 |

|

Oracle Corporation |

USA |

EHR + AI platform |

Oracle Cerner generative AI integration |

Health systems AI platform expansion |

|

Epic Systems |

USA |

EHR + AI workflow |

AI App Marketplace + DAX integration |

38% U.S. hospital EHR with AI layer |

|

AWS HealthLake |

USA |

Cloud AI infrastructure |

HIPAA-compliant AI health data lake |

GE HealthCare + Philips partnerships, 2024 |

|

GE HealthCare Technologies |

USA |

Medical imaging AI |

AWS GenAI partnership + diagnostics |

AWS partnership for medical foundation models, Jul 2024 |

|

Siemens Healthineers |

Germany |

Diagnostics AI, Radiology |

AI-Rad Companion + clinical workflow |

EU market leader in AI-assisted diagnostics |

|

Insilico Medicine |

Hong Kong/USA |

Drug Discovery AI |

Chemistry42 generative AI platform |

INS018_055 Phase II trials, 2024 |

|

Abridge AI Inc. |

USA |

Ambient scribing |

LLM clinical documentation |

30% scribe market share; USD 150 Mn raised |

|

Tempus AI Inc. |

USA |

Oncology AI |

Genomics + clinical trial matching |

Nasdaq IPO 2024; USD 1 Bn+ revenue |

|

Recursion Pharmaceuticals |

USA |

Drug Discovery AI |

AI-driven drug target identification |

Exabiosciences acquisition for AI drug discovery |

|

Hippocratic AI Inc. |

USA |

Patient engagement agents |

Long-context health LLMs |

USD 137 Mn NVIDIA investment Oct 2024 |

|

Nuance Communications — DAX |

USA |

Ambient scribing |

EHR-integrated voice AI |

33% U.S. ambient scribe market; Microsoft subsidiary |

- The competitive dynamics through 2034 will be shaped by three forces: platform consolidation (EHR vendors integrating AI removes standalone AI app market share), clinical validation differentiation (FDA-cleared tools command premium pricing over uncleared alternatives), and data moat building (companies with the largest proprietary clinical training datasets — Epic, NHS, VA — will build AI capabilities that external vendors cannot replicate).

Recent Developments in the Generative AI in Healthcare Market

- The generative AI in healthcare market is recording the highest pace of strategic M&A, partnership formation, and product launch activity of any healthcare technology sub-segment. Six developments from 2024–2025 illustrate where competitive investment is being directed.

|

DATE |

COMPANY |

TYPE |

DESCRIPTION |

IMPACT |

|---|---|---|---|---|

|

Jan 2025 |

NVIDIA + Partners |

Partnership |

NVIDIA partnered with IQVIA, Illumina, Mayo Clinic, and Arc Institute to advance drug discovery, genomic research, and agentic AI in healthcare |

Establishes NVIDIA as foundational infrastructure for pharma AI |

|

Jan 2025 |

Rad AI |

Funding |

Raised USD 60 million Series C at USD 525 million valuation for generative AI radiology solutions |

Signals investor conviction; expands AI radiology deployment |

|

Nov 2024 |

Philips + AWS |

Partnership |

Expanded collaboration to advance HealthSuite cloud services and generative AI across radiology, pathology, cardiology |

Accelerates cloud-native clinical AI across Philips global customer base |

|

Oct 2024 |

Hippocratic AI + NVIDIA |

Investment |

USD 137 million investment from NVentures to develop healthcare AI agents with long-context conversational capabilities |

Positions Hippocratic as leading patient engagement AI platform |

|

Sep 2024 |

Insilico + Inimmune |

Partnership |

Insilico Medicine's Chemistry42 AI platform partnered to expedite immunotherapy discovery and development |

Extends generative AI drug discovery into immunotherapy pipeline |

|

Jun 2024 |

Cognizant + Google Cloud |

Product Launch |

Healthcare-specific LLM solutions integrating Vertex AI and Gemini models to automate administrative processes and improve care experiences |

Brings enterprise generative AI to mid-market healthcare admin workflows |

Related ZMR Market Intelligence Reports:

Healthcare IT Market | AI in Medical Imaging Market | AI in Drug Discovery Market | Electronic Health Records Market | AI in Diagnostics Market | Drug Discovery Informatics Market | Patient Management Market | Medical Image Analysis Software Market

Author:

Mr. Nilesh Patil

Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067

Table Of Content

Methodology

FrequentlyAsked Questions

The ZMR Global Generative AI in Healthcare Market Report contains 300+ pages covering: base year market sizing (USD 1,842 million, 2025), historical data from 2019–2024, forecasts through 2034, six segmentation dimensions with full sub-segment depth, country-level data for 35+ geographies across 6 regions, competitive profiles of 15 key players with strategy analysis, comprehensive DROC framework, 120 data tables and 90 figures, a detailed research methodology, and recent strategic developments.

The global Generative AI in Healthcare market was valued at USD 1,842 million in 2025 and is predicted to reach USD 21,640 million by 2034, registering a CAGR of 31.4% during 2026–2034, according to Zion Market Research. This represents an absolute value addition of approximately USD 19,798 million over the forecast period.

The ZMR report covers six dimensions: Component (Solutions, Services), Function (Medical Imaging & Diagnostics, Drug Discovery & Development, Clinical Documentation & Administrative Automation, Personalised Medicine, Robot-Assisted Surgery, Others), Application (Clinical, Non-Clinical), End-Use (Healthcare Providers, Pharma & Biotech, Healthcare Payers, Others), Deployment (Cloud-Based, On-Premise), and Technology (LLMs, NLP, Computer Vision, Others).

35+ countries across 6 ZMR regions: North America (The U.S., Canada, Mexico), Europe (Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific), Latin America (Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America), The Middle East (GCC, Israel, Turkey, Iran, Rest of Middle East), and Africa (South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa). The Middle East and Africa are reported as two separate regions.

Zion Market Research offers: additional country or regional analysis, specific competitor profiles, extended forecast periods, segment deep-dives, and primary interview data from specific healthcare stakeholder types.

(1) Free sample: https://www.zionmarketresearch.com/report/generative-ai-in-healthcare-market (2) Full PDF purchase: https://www.zionmarketresearch.com/buynow/su/generative-ai-in-healthcare-market (3) Inquiry: sales@zionmarketresearch.com | +1 (302) 444-0166 | Toll Free: +1 (855) 465-4651.

List of Contents

INDUSTRY PERSPECTIVEKey InsightsWHY THIS REPORT?Dynamics (Drivers, Restraints, Opportunities, Challenges)What Is Driving the Global Market?What Is Restraining the Global Market?What Opportunities Exist in the Global Market?Report ScopeSegmentationKey Market Segments Analysis Takeaway:Regional AnalysisKey Regional Analysis Takeaway:Full Country Coverage: Zion Market Research Market ReportCompetitive LandscapeRecent Developments in the MarketRelated ZMR Market Intelligence Reports:HappyClients