Wearable Medical Device Market Size, Share & Forecast 2026–2034

17-May-2026 | Zion Market Research

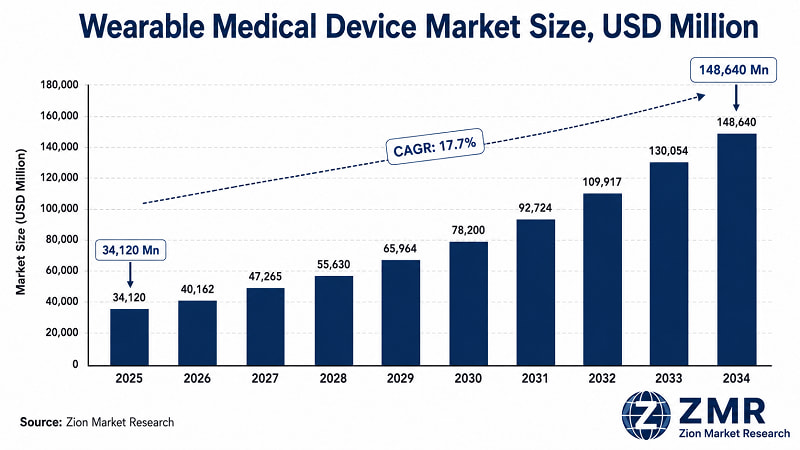

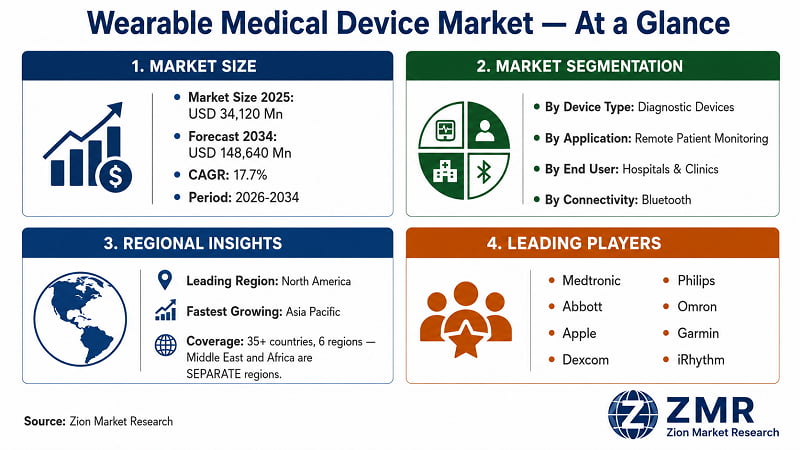

The global Wearable Medical Device market was valued at USD 34,120 Million in 2025. It is projected to reach USD 148,640 Million by 2034, growing at a 17.7% CAGR from 2026 to 2034. North America dominates with approximately 38% revenue share; Asia Pacific registers the fastest growth. Diagnostic wearables hold the largest segment share, driven by remote patient monitoring adoption and rising chronic disease prevalence globally.

Key Insights Snapshot

|

Metric |

Detail |

|

Report Title |

Global Wearable Medical Device Market Size, Share, Trends & Forecast 2026–2034 |

|

Base Year Market Size |

USD 34,120 Million (2025) |

|

Forecast Market Size |

USD 148,640 Million (2034) |

|

CAGR |

17.7% (2026–2034) |

|

Forecast Period |

2026–2034 |

|

Dominant Region |

North America (~38% share, 2025) |

|

Fastest-Growing Region |

Asia Pacific (~19.8% CAGR) |

|

Dominant Device Type |

Diagnostic Devices (~43% share, 2025) |

|

Dominant Application |

Remote Patient Monitoring |

|

Report Format |

|

|

Publisher |

Zion Market Research |

What Is the Wearable Medical Device Market?

- The wearable medical device market refers to the global industry encompassing body-worn electronic devices designed to monitor, diagnose, treat, or manage health conditions — distinguished from general consumer wellness wearables by clinical-grade accuracy, regulatory clearance, and integration into formal care pathways.

- At USD 34,120 Million in 2025, this market has crossed the inflection point where hospital procurement, pharma clinical trials, and payer reimbursement structures are actively pulling demand — not just consumer curiosity. ZMR forecasts this dynamic will drive the market to USD 148,640 Million by 2034.

- The structural driver isn't technology alone — it's the convergence of chronic disease burden, ageing demographics, and health systems under cost pressure that makes continuous remote monitoring economically unavoidable.

What Healthcare Leaders Need to Know About the Wearable Medical Device Market

- Hospital CIOs:

Wearable remote monitoring is shifting from pilot to enterprise-scale. U.S. hospitals integrating FDA-cleared wearable ECG and CGM devices into EHR workflows report up to 30% reductions in unplanned readmissions. Budget allocation for connected care infrastructure must accelerate ahead of the 2027 CMS reimbursement expansion window.

- Pharma R&D Heads:

Wearable sensors are reshaping Phase II/III trial design. Continuous biometric capture from FDA-validated wearables reduces site visit frequency and per-patient trial costs while producing richer endpoint datasets. Organisations not integrating wearables into trial protocols by 2026 face a measurable competitive disadvantage in recruitment speed and data quality.

- Healthcare Investors:

Market expands from USD 34,120 Mn to USD 148,640 Mn by 2034 — a 4.4x absolute value increase. Diagnostic wearables dominate on volume; therapeutic wearables (neurostimulation, drug delivery) grow fastest at ~21% CAGR. Early-stage positions in AI-analytics platforms layered on wearable data streams represent the highest risk-adjusted return profile through 2028.

- Regulatory Affairs Directors:

FDA's Digital Health Centre of Excellence and EU MDR are converging on stricter post-market surveillance requirements. Manufacturers without robust real-world evidence collection built into device architecture face growing regulatory risk and potential market access delays in key European markets through 2026–2027.

- Managed Care Executives:

Remote therapeutic monitoring reimbursement codes introduced in 2023 create direct revenue capture opportunities for health systems deploying wearable monitoring at scale. Payers in North America are shifting toward value-based contracts rewarding early-warning capability — a concrete commercial case for wearable adoption.

What Is Driving the Wearable Medical Device Market?

- Rising Chronic Disease Burden:

Over 537 million adults have diabetes globally (IDF, 2025) and 1.28 billion have hypertension (WHO, 2025). Abbott Laboratories deployed FreeStyle Libre across 58 countries, reaching 5+ million users and generating USD 5.3 billion+ in annual CGM revenue by 2024 — demonstrating the commercial scale achievable when reimbursement infrastructure meets clinical need. Regulatory agencies in the U.S., EU, Japan, and Australia are updating guidelines to recommend CGMs as first-line monitoring tools.

- CMS Reimbursement Expansion:

CMS expanded remote physiologic monitoring (CPT 99453–99458) and remote therapeutic monitoring (CPT 98975–98980) codes from 2022 onward, converting wearable monitoring from a cost centre into a revenue-generating care service. Germany's DiGA pathway — approving 50+ digital health applications by 2024 — creates a parallel EU commercial runway.

- Consumer Technology Achieving Clinical Clearance:

Apple received FDA clearance for AFib detection on Apple Watch with clearance in 50+ countries. iRhythm Technologies processed over 4 million Zio Patch cardiac analyses by 2024. This convergence expands the TAM beyond traditional hospital procurement channels at sub-USD 500 per device.

|

"Remote monitoring is no longer a peripheral capability — it is the future architecture of chronic disease management. Payers are actively requesting wearable integration as a condition of preferred network status." |

|

— Dr. Karen DeSalvo, Chief Health Officer, Google Health |

|

(Source: HLTH Conference, October 2023) |

What Is Restraining the Wearable Medical Device Market?

- Data Privacy and Cybersecurity Risk:

Wearable devices continuously transmit sensitive biometric data, creating acute HIPAA and GDPR compliance obligations. FDA cybersecurity advisories have extended enterprise hospital procurement cycles by 6–12 months.

- EU MDR Regulatory Approval Delays:

The EU MDR transition has extended CE marking timelines by 12–18 months. Over 600 manufacturers reported compliance challenges in 2024 surveys, creating a market access gap for mid-market players.

- Clinical Accuracy Gaps and Clinician Hesitancy:

Independent studies have found accuracy gaps in consumer wearable SpO2 and blood pressure sensors across demographic groups, slowing formulary adoption and creating trust deficits requiring peer-reviewed clinical validation to overcome.

Despite these challenges, the market is expected to grow from USD 34,120 Million in 2025 to USD 148,640 Million by 2034.

What Industry Leaders Are Saying About the Wearable Medical Device Market

|

"The integration of wearable devices into our cardiac care pathways has transformed how we manage post-discharge patients. We have reduced 30-day readmission rates for heart failure patients by tracking daily biometric data in near real-time." |

|

— Dr. Richard Kovacs, Former President, American College of Cardiology |

|

(Source: ACC Scientific Sessions, March 2023) |

|

"Continuous glucose monitoring is becoming the standard of care. The data density from CGMs allows medication adjustments that were simply impossible with finger-stick testing — it is a clinical step-change, not an incremental improvement." |

|

— Dr. Anne Peters, Director, USC Westside Center for Diabetes, University of Southern California Keck School of Medicine |

|

(Source: ADA Scientific Sessions, June 2023) |

How Is the Wearable Medical Device Market Segmented?

- Diagnostic devices dominate, capturing approximately 43% of 2025 revenue, led by continuous glucose monitors, cardiac monitors, and pulse oximeters. Remote patient monitoring is the leading application, reflecting health systems' strategic pivot toward hospital-at-home models. Bluetooth leads the connectivity layer as the preferred low-power, standards-compatible protocol for clinical device integration.

|

By Device Type: Diagnostic Devices, Therapeutic Devices, Drug Delivery Devices |

|

By Application: Remote Patient Monitoring, Sports & Fitness, Home Healthcare, Chronic Disease Management |

|

By End User: Hospitals & Clinics, Homecare Settings, Sports & Fitness Centres, Research Institutions |

|

By Connectivity Technology: Bluetooth, Wi-Fi, NFC, Cellular |

|

By Region: North America, Europe, Asia Pacific, Latin America, The Middle East, Africa |

Which Region Leads the Wearable Medical Device Market?

- North America leads the global market with an estimated 38% revenue share in 2025. The U.S. drives this position through FDA regulatory infrastructure, high clinical adoption of CGMs and cardiac monitors, CMS remote monitoring reimbursement, and concentrated R&D investment. Canada contributes through expanding home-care programmes; Mexico through growing private hospital sector procurement.

- Asia Pacific registers the fastest regional CAGR, propelled by China's national digital health initiatives, India's expanding private healthcare sector, and South Korea and Japan's advanced electronics manufacturing capabilities. Europe maintains strong growth through Germany's DiGA reimbursement framework and the U.K.'s NHS digital transformation agenda. Latin America, The Middle East, and Africa represent emerging growth pockets driven by healthcare access expansion and rising smartphone penetration enabling connected care.

Report Segmentation & Scope

|

Zion Market Research | Market & Reports — Report Segmentation & Scope |

|

|

Scope Included in the Study |

|

|

By Device Type |

Diagnostic Devices • Therapeutic Devices • Drug Delivery Devices |

|

By Application |

Remote Patient Monitoring • Sports & Fitness • Home Healthcare • Chronic Disease Management |

|

By End User |

Hospitals & Clinics • Homecare Settings • Sports & Fitness Centres • Research Institutions |

|

By Connectivity Technology |

Bluetooth • Wi-Fi • NFC • Cellular |

|

Regional Analysis |

|

|

North America |

The U.S., Canada, Mexico |

|

Europe |

Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe |

|

Asia Pacific |

China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific |

|

Latin America |

Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America |

|

The Middle East |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

Africa |

South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa |

|

Note: The scope can be further tailored as per your specific requirement. Contact sales@zionmarketresearch.com |

|

**Source: Zion Market Research | Global Wearable Medical Device Market Report.

Who Are the Leading Companies in the Wearable Medical Device Market?

- Key players operating in the Global Wearable Medical Device market include Medtronic plc (Ireland), Abbott Laboratories (U.S.), Philips Healthcare (Netherlands), Apple Inc. (U.S.), Dexcom Inc. (U.S.), Garmin Ltd. (Switzerland), Omron Healthcare (Japan), Fitbit Inc. — Google LLC (U.S.), Samsung Electronics (South Korea), Withings (France), iRhythm Technologies (U.S.), Insulet Corporation (U.S.), BioTelemetry Inc. (U.S.), Polar Electro (Finland), and LifeScan Inc. (U.S.), among others.

- The market is bifurcated between legacy medical device manufacturers with deep clinical and regulatory capability, and technology-led entrants competing on AI analytics, EHR integration, and direct-to-consumer distribution. FDA clearance speed and AI analytics depth are the primary competitive battlegrounds through 2027.

What Recent Developments Are Shaping the Wearable Medical Device Market?

- Jan 2025 — Dexcom Inc. received FDA clearance for Stelo, its over-the-counter CGM, opening continuous glucose monitoring to an estimated 25 million U.S. adults with Type 2 diabetes not on insulin — the largest single TAM expansion in CGM history.

- Sep 2024 — Apple launched Apple Watch Series 10 with enhanced AFib detection and Sleep Apnoea FDA clearance, reinforcing its position as the leading consumer-clinical hybrid wearable platform globally.

- Mar 2025 — Medtronic announced a strategic partnership with Google Cloud to integrate AI-driven predictive analytics across its wearable cardiac and diabetes monitoring device ecosystem.

|

Date |

Company |

Type |

Description |

Market Impact |

|

Mar 2025 |

Medtronic / Google Cloud |

Strategic Partnership |

AI predictive analytics across wearable cardiac and diabetes platforms |

Elevates clinical decision-support; raises AI benchmark for competitors |

|

Jan 2025 |

Dexcom Inc. |

Regulatory Clearance |

Stelo OTC CGM FDA cleared for T2D non-insulin users |

Opens ~25M U.S. adult TAM; accelerates CGM commoditisation |

|

Sep 2024 |

Apple Inc. |

Product Launch |

Watch Series 10 — enhanced AFib + Sleep Apnoea FDA clearance |

Expands consumer-clinical installed base globally |

|

Jul 2024 |

Insulet Corporation |

Product Expansion |

OmniPod 5 AID system expanded to 20+ additional EU countries |

Strengthens insulin pump leadership in Europe |

|

Apr 2024 |

Samsung Electronics |

Regulatory Clearance |

Galaxy Watch 7 FDA clearance for AFib detection |

Second consumer-clinical smartwatch with clinical cardiac credentials |

About Us:

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, the company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is been updated constantly in order to fulfill our clients with prompt and direct online access to our database. Keeping in mind the client’s needs, we have included expert insights on global industries, products, and market trends in this database. Last but not the least, we make it our duty to ensure the success of clients connected to us—after all—if you do well, a little of the light shines on us.

Author:

Mr. Nilesh Patil

Director at Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067