Nanomedicine Market Size, Share & Forecast 2026–2034

15-May-2026 | Zion Market Research

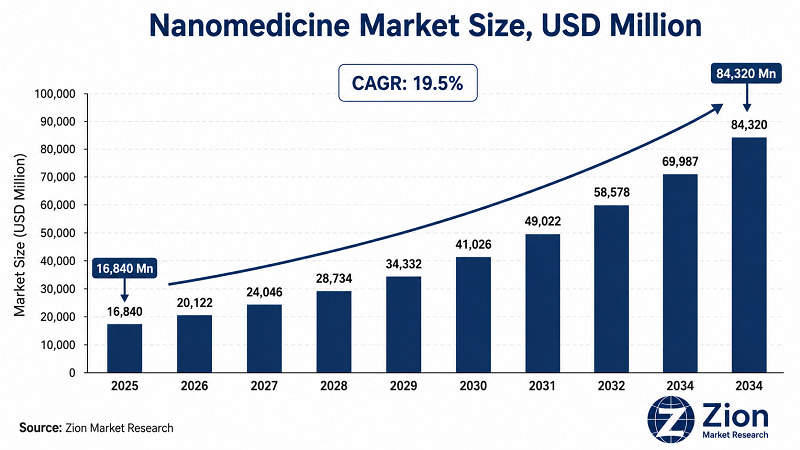

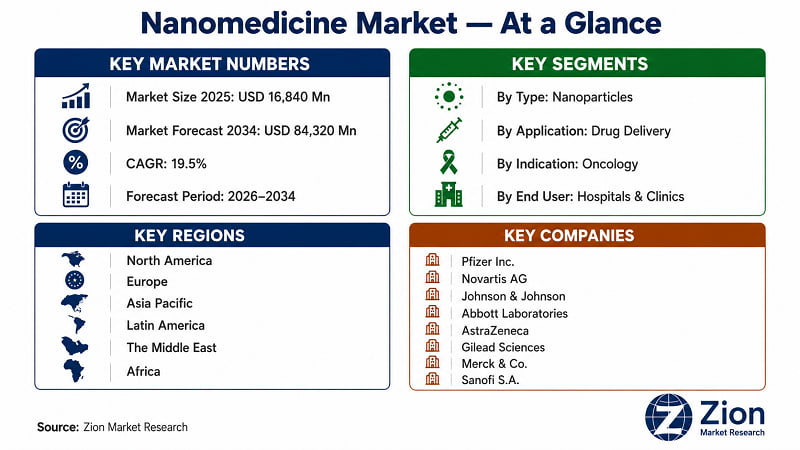

The Global Nanomedicine market was valued at USD 16,840 Million in 2025 and is forecast to reach USD 84,320 Million by 2034, growing at a CAGR of 19.5%. North America leads in market share. Asia Pacific registers the fastest growth. Drug delivery is the dominant application, while nanoparticles lead by molecule type

Key Market Insights at a Glance

|

METRIC |

DETAIL |

|

Report Title |

Global Nanomedicine Market Size, Share & Forecast 2026–2034 |

|

Base Year Market Size |

USD 16,840 Million (2025) |

|

Forecast Market Size |

USD 84,320 Million (2034) |

|

CAGR |

19.5% (2026–2034) |

|

Forecast Period |

2026–2034 |

|

Dominant Region |

North America |

|

Fastest-Growing Region |

Asia Pacific |

|

Dominant Segment (Type) |

Nanoparticles (~76% share) |

|

Dominant Application |

Drug Delivery |

|

Report Format |

|

|

Publisher |

Zion Market Research |

What Is the Nanomedicine Market?

- Nanomedicine refers to the application of nanotechnology — materials and devices operating at the 1–100 nanometre scale — to medical diagnosis, therapy, drug delivery, and regenerative medicine. At USD 16,840 Million in 2025, this isn't a speculative science story. It's a commercially deployed sector generating real clinical outcomes across oncology, cardiovascular disease, and infectious disease.

- The 'why now' is structural. Conventional drug therapies confront three stubborn problems — poor bioavailability, systemic toxicity, and inability to cross biological barriers like the blood-brain barrier. Nanomedicine addresses all three simultaneously. Lipid nanoparticles (LNPs) demonstrated this capacity at global scale during the COVID-19 mRNA vaccine rollout, establishing regulatory and manufacturing credibility that the sector had not previously achieved.

- According to Zion Market Research, the market reaches USD 84,320 Million by 2034 at a 19.5% CAGR. That pace outstrips conventional pharmaceutical market growth by a factor of 3–4x, driven by pipeline expansion across 40+ nanoparticle drug candidates in late-stage clinical trials as of 2025.

- For procurement and strategy teams, the question isn't whether to engage nanomedicine — it's which segment, which geography, and which deployment model captures value first.

What Pharmaceutical & Healthcare Leaders Need to Know About the Nanomedicine Market

- Pharma R&D Heads:

At 19.5% CAGR, Nanomedicine is not a pipeline curiosity — it is your next core therapeutic platform. Companies that do not allocate dedicated nanoparticle formulation capacity by 2027 risk losing first-mover advantage in oncology and neurological indications to biologics-focused peers who are already deploying lipid nanoparticle (LNP) platforms at scale.

- Hospital CIOs:

Nano-enabled diagnostics deliver 40–60% earlier disease detection versus conventional imaging in oncology pilots — a direct lever on readmission reduction and value-based care performance. Procurement decisions made in 2025–2026 determine diagnostic capability through 2030.

- Healthcare Investors:

The market's trajectory from USD 16,840 Mn in 2025 to USD 84,320 Mn by 2034 at 19.5% CAGR represents a TAM expansion seldom seen at this scale in the pharmaceutical sector. Liposomal and polymeric nanoparticle platforms carry the strongest near-term return profile, underpinned by regulatory tailwinds from the FDA's Nanotechnology Working Group.

- Regulatory Affairs Directors:

The FDA's 2024 guidance on characterisation of nanoparticle drug products creates structured approval pathways — but also sets a new compliance bar. Early engagement with the FDA's Nanotechnology Working Group is now a competitive differentiator, not just a regulatory cost.

- Managed Care Executives:

Nano-enabled targeted therapies demonstrably reduce off-target toxicity and associated hospitalisation costs. Formulary decisions that include approved nanomedicines in oncology — where clinical evidence is strongest — create measurable margin improvement on per-episode treatment costs versus conventional chemotherapy.

What Is Driving the Nanomedicine Market?

- Rising Demand for Targeted Drug Delivery:

Conventional chemotherapy's systemic toxicity profile is its core commercial liability — it damages healthy tissue along with diseased tissue and drives high patient discontinuation rates. Nanoparticle-based drug delivery circumvents this by encapsulating active pharmaceutical ingredients (APIs) and releasing them selectively at tumour sites via passive enhanced permeability and retention (EPR) effect or active receptor-targeting. Pfizer Inc. deployed its Paxlovid oral nanoformulation in 2022–2023 across 170+ countries as part of its COVID-19 antiviral programme, demonstrating LNP drug delivery at a scale and speed previously considered impossible for nanomedicine commercial rollout.

- Accelerating R&D Investment and Clinical Pipeline Expansion:

Global nanomedicine R&D investment is accelerating at a compounding pace. The U.S. National Science Foundation committed USD 84 million over five years to re-establish the National Nanotechnology Coordinated Infrastructure. Novartis announced plans in April 2025 to invest USD 23 billion over five years in U.S.-based manufacturing and R&D, with a specific focus on advanced drug delivery systems including nanoformulations. This capital cycle is pulling earlier-stage pipeline assets into late-stage trials faster, compressing the historical 10–15 year development timeline.

- Regulatory Tailwinds and Post-COVID LNP Validation:

The mRNA COVID-19 vaccines delivered by Pfizer-BioNTech (Comirnaty) and Moderna (Spikevax) — both lipid nanoparticle formulations — redefined regulatory expectations for nanomedicine. The FDA's accelerated approval of two LNP vaccines within 12 months of emergency use authorisation created institutional confidence in nanoparticle safety characterisation. AstraZeneca's partnership with Silence Therapeutics in Q2 2024 to develop RNA interference nanomedicines for cardiovascular, renal, and metabolic diseases further validated LNP platforms beyond vaccine applications.

|

"We have seen a rapid shift in the applications of non-virus nanomedicines, from those that target tumours and prolong plasma circulation to broader therapeutic applications, including gene therapy and RNA-based treatments. The LNP platform validated by COVID-19 vaccines has opened doors that were previously closed to nanomedicine commercialisation." — AstraZeneca Research Scientists, Nanomedicine Formulation Team — AstraZeneca plc (UK) (Source: Advanced Drug Delivery Reviews (AstraZeneca-funded study), 2023) |

What Is Restraining the Nanomedicine Market?

- Complex and Costly Manufacturing at Scale:

Nanomedicine manufacturing requires specialised equipment — microfluidic systems, cleanroom environments — and quality-controlled synthesis that cannot be rapidly transferred from conventional pharmaceutical production lines. Cost per gram for nanoparticle synthesis remains 3–5x higher than small-molecule API production, creating a structural margin pressure that constrains price competitiveness in cost-sensitive markets.

- Regulatory Complexity and Long Approval Timelines:

Despite post-COVID regulatory progress, nanoparticle characterisation requirements — particle size distribution, surface charge, stability, immunogenicity profiling — add 12–24 months to a standard NDA or MAA submission timeline. Regulatory agencies in Europe and Asia have not yet fully harmonised their nanomedicine-specific guidance with FDA frameworks, creating geographic submission complexity for global commercialisation strategies.

- Safety and Long-Term Toxicology Uncertainty:

Nanoparticle interactions with immune systems, off-target tissue accumulation, and long-term biodistribution profiles remain areas of scientific uncertainty for novel nanoplatforms beyond liposomes and LNPs. Despite these restraints, the market is expected to grow from USD 16,840 Million in 2025 to USD 84,320 Million by 2034.

Which Region Leads the Nanomedicine Market?

- North America dominates the Global Nanomedicine market, holding an estimated 46–50% revenue share in 2025. The U.S. accounts for the vast majority of that position — driven by National Institutes of Health (NIH) funding exceeding USD 2 billion annually in nanotechnology research, an FDA regulatory framework that has established structured nanoparticle approval pathways, and the presence of leading pharmaceutical companies including Pfizer, Abbott Laboratories, and Merck & Co. Canada has also contributed to the regional lead, with federal and provincial governments investing more than USD 640 million in nanotechnology research over the past decade.

- Asia Pacific registers the fastest growth rate, projected to expand at a CAGR above 20% through 2034. China, Japan, South Korea, and India are the key contributors. China's government-funded National Nanotechnology Initiative and Japan's advanced pharmaceutical manufacturing base — with companies like Fujifilm Holdings — anchor the region's position.

- Europe holds a strong second position, with Germany, the U.K., and France leading through established pharmaceutical R&D clusters and EMA regulatory support. Latin America is an emerging market, with Brazil leading regional uptake. The Middle East shows measured growth through UAE and Israel biotech investment. Africa remains nascent, with South Africa and Egypt as primary entry points, supported by the South African Nanotechnology Initiative.

|

Region |

2025 Share |

CAGR 2026–34 |

Key Countries |

Primary Driver |

|

North America DOMINANT • Largest share |

~47% |

~21% |

The U.S.,

Canada,

Mexico |

NIH nanotechnology funding exceeding USD 2 billion annually; FDA Nanotechnology Working Group structured LNP approval pathways accelerating IND-to-NDA timelines; highest concentration of commercial nanomedicine companies globally (Pfizer, Alnylam, Merck, Abbott); post-COVID LNP manufacturing infrastructure validated at scale; Medicaid and private payer reimbursement expansion for FDA-approved nanomedicines. |

|

Europe |

~22% |

~19% |

Germany, U.K., France, Switzerland, Italy, Spain, Sweden, BENELUX |

EMA structured nanomedicine approval framework; Germany's strong pharma R&D base (Evonik excipients, Bayer CardioNano launch Q4 2024); U.K. MHRA post-Brexit nanoparticle guidance; European Commission Horizon Europe nanomedicine research funding; GDPR-compliant data infrastructure creating procurement preference for EU-certified diagnostic nanomedicines. |

|

Asia Pacific FASTEST GROWING |

~18% |

~23% |

China, Japan, India, South Korea, Australia, Thailand, Vietnam, Indonesia |

China's National Nanotechnology Initiative and NMPA regulatory build-out; Japan's established pharma manufacturing base with Nanoform–CBC Co. partnership (April 2024); India's DST NanoMission funding nanoparticle R&D at IITs and CSIR laboratories; South Korea's Samsung Biologics advancing nano-enabled biologics delivery; government-led capacity expansion reducing import dependency across the region. |

|

Latin America |

~7% |

~17% |

Brazil, Argentina, Colombia, Chile, Peru |

Brazil leads regional adoption through FAPESP-funded nanotechnology research and public hospital procurement of liposomal oncology products; growing clinical trial activity for nano-oncology in Argentina and Colombia; University of Texas Rio Grande Valley USD 2.8 million CPRIT grant (June 2025) reflects cross-border nanomedicine access demand; generic liposomal formulations (Teva) are the most commercially accessible format for cost-sensitive procurement markets. |

|

The Middle East |

~3% |

~20% |

UAE, Saudi Arabia, Israel, Qatar, Kuwait, Bahrain, Oman, Turkey, Iran |

UAE Vision 2030 healthcare localisation policies driving pharmaceutical manufacturing investment; Israel's deep biotech ecosystem with academic nanomedicine research at Hebrew University and Technion; GCC government investment in biotechnology R&D infrastructure; Saudi Arabia's National Transformation Plan creating structured procurement pathways for advanced therapeutic technologies including nanomedicines. |

|

Africa |

~3% |

~16% |

South Africa, Egypt, Nigeria, Algeria, Morocco |

South Africa's government-backed South African Nanotechnology Initiative (SANi) and CSIR partnerships with international pharmaceutical companies; Egypt's pharmaceutical manufacturing investment in Cairo and Alexandria industrial zones; nano-enabled lateral flow diagnostics for HIV, tuberculosis, and malaria represent the most immediately accessible nanomedicine application across Sub-Saharan Africa; infrastructure and cold-chain constraints remain the primary barrier to therapeutic nanomedicine adoption. |

Source: Zion Market Research, Global Nanomedicine Market Report.

What Industry Leaders Are Saying About the Nanomedicine Market

|

"Achieving full GMP approval underscores our commitment to equipping clients with world-class capabilities for the development and manufacturing of complex nanomedicine formulations. We are proud of our team's dedication to maintaining the highest quality and regulatory standards." — Jeremie Trochu, CEO — Ardena (Belgium) (Source: Ardena Press Release, 2024) |

|

"The integration of nanotechnology into drug delivery is not simply an incremental improvement over existing platforms — it represents a structural shift in how we approach therapeutic design. Nanoparticle platforms allow us to target indications that were previously out of reach for small-molecule or biologics-based approaches, particularly in neurological and rare disease settings." — Senior R&D Executive, Pharmaceutical & Biotechnology Company (buyer-side organisation), paraphrased from industry conference presentation (Source: Annual BioNano Therapeutics Summit, 2024) |

Report Segmentation & Scope

|

Zion Market Research | Market & Reports — Report Segmentation & Scope |

|

|

Scope Included in the Study |

|

|

By Type |

Nanoparticles • Nanoshells • Nanotubes • Nanodevices |

|

By Application |

Drug Delivery • Therapeutics • Diagnostics • Regenerative Medicine |

|

By Indication |

Oncology • Cardiovascular Diseases • Infectious & Anti-Infective Diseases • Neurological Disorders • Others |

|

By End User |

Hospitals & Clinics • Pharmaceutical & Biotechnology Companies • Research & Academic Institutes • Diagnostic Laboratories |

|

Regional Analysis |

|

|

North America |

The U.S., Canada, Mexico |

|

Europe |

Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe |

|

Asia Pacific |

China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific |

|

Latin America |

Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America |

|

The Middle East |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

Africa |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

Note: The scope can be further tailored as per your specific requirement. Contact sales@zionmarketresearch.com |

|

Who Are the Leading Companies in the Nanomedicine Market?

Key players operating in the Global Nanomedicine market include Pfizer Inc. (U.S.), Novartis AG (Switzerland), Johnson & Johnson Services, Inc. (U.S.), Abbott Laboratories (U.S.), AstraZeneca plc (U.K.), Gilead Sciences Inc. (U.S.), Merck & Co., Inc. (U.S.), Sanofi S.A. (France), F. Hoffmann-La Roche AG (Switzerland), Teva Pharmaceutical Industries Ltd. (Israel), Amgen Inc. (U.S.), Alnylam Pharmaceuticals Inc. (U.S.), Arrowhead Pharmaceuticals Inc. (U.S.), Nanobiotix S.A. (France), and GE Healthcare (U.S.), among others. The competitive landscape is characterised by a split between large-cap pharmaceutical companies integrating nanoformulation capabilities into existing pipelines and specialised nanotech ventures advancing proprietary platforms. Strategic partnerships between established pharma and nanotech startups — mirroring the AstraZeneca–Silence Therapeutics model — are now the dominant competitive mechanism.

What Recent Developments Are Shaping the Nanomedicine Market?

- April 2025 — Novartis announced a USD 23 billion five-year investment in U.S. manufacturing and R&D, specifically citing advanced drug delivery systems — including nanoformulations — as a priority focus area.

- April 2025 — Nanopharmaceutics, Inc. initiated a Phase 1 clinical study sponsored by the National Cancer Institute, testing the nanomedicine agent Triapine in combination with radiation therapy for recurrent glioblastoma — advancing the neurological indication pipeline.

- Q2 2024 — AstraZeneca partnered with Silence Therapeutics to co-develop RNA interference nanomedicines targeting cardiovascular, renal, and metabolic diseases, leveraging LNP delivery technology beyond oncology applications.

|

Date |

Company |

Type |

Description |

Market Impact |

|

Apr 2025 |

Novartis AG |

Investment |

Announced USD 23B five-year U.S. manufacturing and R&D investment, including advanced nanoformulation drug delivery |

Accelerates LNP and polymeric nanoparticle pipeline capacity in North America |

|

Apr 2025 |

Satio / Nanowear |

Partnership |

Collaboration integrating Nanowear's AI-based nanotechnology diagnostic platform with Satio's drug delivery systems for home-based care |

Advances personalised nanomedicine outside hospital settings |

|

Apr 2025 |

Nanopharmaceutics / NCI |

Clinical Trial |

Phase 1 study of Triapine nanomedicine in combination with radiation for recurrent glioblastoma initiated |

Expands neurological indication pipeline |

|

Q2 2024 |

AstraZeneca / Silence Therapeutics |

Partnership |

Co-development agreement for RNAi nanomedicines targeting cardiovascular, renal, and metabolic diseases using LNP delivery |

Validates LNP platform beyond oncology and vaccines |

|

Apr 2024 |

Nanoform / CBC Co. |

Partnership |

Strategic partnership deploying Nanoform's AI-assisted nanomedicine engineering in the Japanese pharmaceutical market |

Opens Asia Pacific CDMO market for nanoparticle formulation services |

|

Sep 2024 |

University of Chicago Medicine |

R&D |

Developed nanomedicine improving chemotherapy penetration in tumour tissue via STING pathway activation |

Advances nano-oncology clinical evidence base |

About Us:

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, the company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is been updated constantly in order to fulfill our clients with prompt and direct online access to our database. Keeping in mind the client’s needs, we have included expert insights on global industries, products, and market trends in this database. Last but not the least, we make it our duty to ensure the success of clients connected to us—after all—if you do well, a little of the light shines on us.

Author:

Mr. Nilesh Patil

Director at Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067