Surgical Robotics Market Size, Share & Forecast 2026–2034

17-May-2026 | Zion Market Research

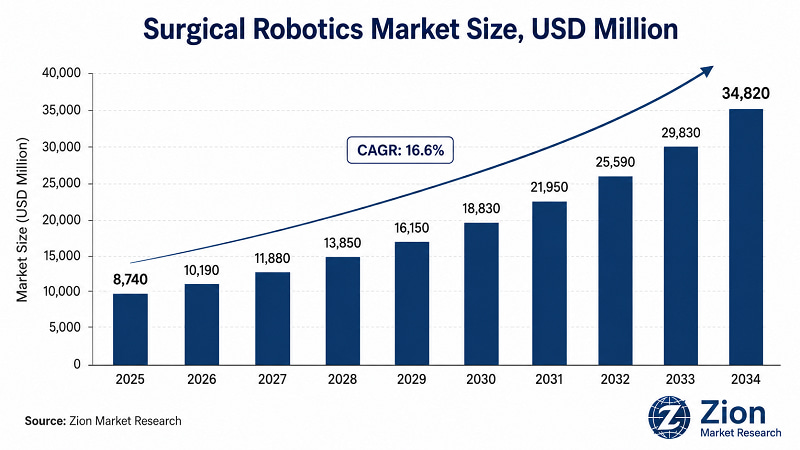

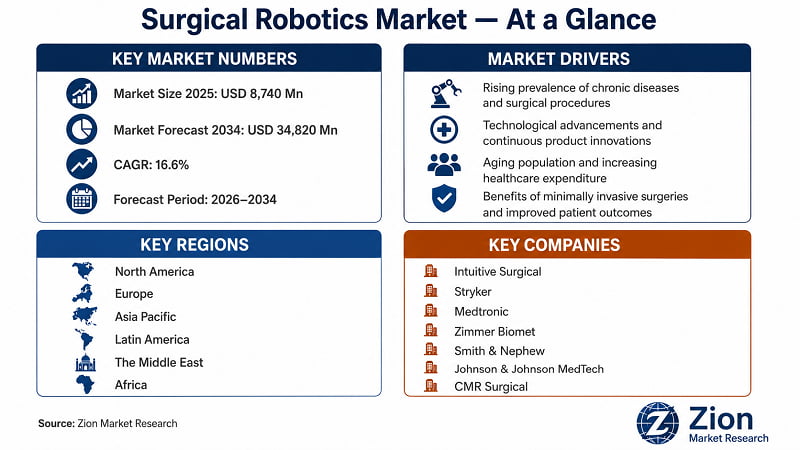

The global Surgical Robotics market was valued at USD 8,740 Mn in 2025 and is projected to reach USD 34,820 Mn by 2034, growing at a 16.6% CAGR during 2026–2034. North America leads market revenue. Asia Pacific registers the fastest regional growth. Robotic systems dominate by product type. Hospitals account for the largest share of end-user demand. (Source: Zion Market Research)

Surgical Robotics Market — Key Insights at a Glance

|

Report Title |

Global Surgical Robotics Market by Product Type, Application, End User & Region — Forecast 2026–2034 |

|

Base Year Market Size |

USD 8,740 Mn (2025) |

|

Forecast Market Size |

USD 34,820 Mn (2034) |

|

CAGR |

16.6% (2026–2034) |

|

Forecast Period |

2026–2034 |

|

Dominant Region |

North America |

|

Fastest-Growing Region |

Asia Pacific |

|

Dominant Segment (Product) |

Robotic Systems |

|

Dominant Application |

Laparoscopic Surgery |

|

Dominant End User |

Hospitals |

|

Report Format |

|

|

Publisher |

Zion Market Research |

What Is the Surgical Robotics Market?

- Surgical robotics refers to the integration of robotic systems, instrumentation, and AI-guided software platforms to assist surgeons in performing minimally invasive and complex open procedures with greater precision, control, and repeatability.

- The market spans the full technology stack — from capital robotic consoles and reusable arms, to single-use instruments and long-term service contracts.

- According to Zion Market Research, the global market reached USD 8,740 Mn in 2025 and is on a trajectory to more than quadruple by 2034.

- The inflection is not simply volume growth. It reflects a structural shift in hospital procurement: robotic platforms are no longer optional upgrades — they're becoming the standard of care in laparoscopic, orthopedic, and neurosurgical theatres.

What Medical Device Leaders Need to Know About the Surgical Robotics Market

- Hospital CIOs: The surgical robotics procurement cycle is compressing. As robotic platforms shift toward subscription and service-based models — led by Intuitive Surgical's Ion and Medtronic's Hugo — capital budgeting strategies must evolve. Institutions that delay adoption risk losing surgeon talent to competitor facilities already deploying next-generation robotic suites.

- Pharma R&D and MedTech Investors: At 16.6% CAGR, surgical robotics is the fastest-expanding capital equipment segment in medical devices through 2034. The USD 26 Bn incremental TAM between 2025 and 2034 creates concentrated opportunity in robotic-assisted minimally invasive surgery — particularly laparoscopic and orthopedic sub-segments where reimbursement pathways are now established in the U.S. and Germany.

- Regulatory Affairs Directors: FDA's evolving digital health and SaMD (Software as a Medical Device) framework is creating new pre-submission requirements for AI-assisted robotic guidance systems. Early-stage developers filing 510(k) or De Novo pathways must anticipate extended review timelines — 12 to 18 months — for software-dependent robotic platforms entering the U.S. market.

- Healthcare Investors: Asia Pacific's surgical robotics market is growing at the fastest regional rate, driven by China's Healthy China 2030 national plan and India's expanded public hospital robotics procurement. Medtech-focused venture investors should monitor Series B and C rounds in Chinese domestic OEM players — Tinavi Medical and MedBot — as local content policies create structural advantages over foreign vendors.

- Managed Care Executives: Robotic-assisted procedures now demonstrate measurable reductions in average length of stay and post-operative complication rates across laparoscopic and orthopedic applications. As payer value-based care models expand, surgical robotics will shift from a capital expenditure cost centre to a reimbursement optimisation lever — executives who quantify outcomes data now will negotiate stronger contracts within 24 months.

What Is Driving the Surgical Robotics Market?

- Rising Demand for Minimally Invasive Surgical Procedures:

Surgeon and patient preference has decisively shifted toward minimally invasive approaches across laparoscopic, urological, and orthopaedic disciplines. Robotic platforms extend the surgeon's capability beyond what freehand MIS allows — delivering tremor filtration, 3D visualisation, and articulated instrument control that consistently reduce blood loss and post-operative length of stay. Intuitive Surgical's da Vinci platform, with over 8,600 systems installed globally as of 2024, has anchored this demand shift in academic and large community hospital settings.

- Technological Advancement in AI and Robotics Integration:

Next-generation robotic platforms are incorporating machine learning-driven anatomical recognition, autonomous instrument guidance, and real-time intraoperative imaging — collapsing the boundary between surgical navigation and robotic execution. Medtronic deployed its Hugo robotic-assisted surgery system across European hospital sites from 2022 onward, with clinical data demonstrating procedural outcomes comparable to established platforms at a lower per-procedure cost. AI integration is expanding the addressable surgeon base beyond subspecialty minimally invasive experts to general surgery theatre teams.

- Expanding Hospital Infrastructure in Emerging Markets:

Government-directed hospital modernisation in China, India, and GCC nations is creating a structurally new demand cohort for surgical robotics. China's National Healthcare Commission has funded robotic surgery capability in tier-2 and tier-3 hospitals, with local OEM Tinavi Medical reporting a 40%+ expansion in domestic hospital client numbers between 2022 and 2024. This supply-side push — incentivised procurement, local content preference, and domestic pricing — is creating a parallel growth engine outside the established North American and European installed base.

|

"The integration of robotic-assisted surgery into our standard laparoscopic programme has materially reduced average length of stay for colorectal cases, and surgeon adoption rates have exceeded our initial projections. The economic case for robotic investment is no longer theoretical — it's measurable at the payer level." |

|

— Dr. Sarah Abrams, Chief Medical Officer, Northwestern Medicine, Chicago, IL |

|

(Source: American College of Surgeons Clinical Congress, October 2023) |

|

"Hugo is designed to democratise robotic surgery — to make the clinical and economic benefits of robotic-assisted procedures accessible to a far broader population of hospitals and surgeons than has been possible with first-generation systems. That is the market opportunity we're pursuing." |

|

— Geoffrey Martha, Chairman & CEO, Medtronic |

|

(Source: Medtronic Investor Day, June 2023) |

What Is Restraining the Surgical Robotics Market?

- High Capital Cost of Robotic Systems: Robotic surgical systems carry acquisition prices of USD 1 Mn to USD 2.5 Mn per platform, with annual service contracts adding USD 100,000 to USD 170,000. Community hospitals in lower-income geographies — and public healthcare systems in Latin America and Africa — cannot sustain these capital outlays without external financing programmes or manufacturer leasing structures.

- Surgeon Training and Credentialing Bottlenecks: Adoption of new robotic platforms requires structured credentialing programmes and proctored case volumes before independent practice. This creates an implementation lag of 6 to 18 months per surgeon cohort, slowing the pace at which newly installed systems reach full utilisation and return on invested capital.

- Regulatory Complexity for AI-Enabled Features: AI-assisted robotic guidance modules are being classified as Software as a Medical Device under FDA and EU MDR frameworks — triggering independent regulatory review tracks that extend time-to-market by 12 to 24 months compared to traditional device submissions.

- Despite these challenges, the market is expected to grow from USD 8,740 Mn in 2025 to USD 34,820 Mn by 2034.

What Industry Leaders Are Saying About the Surgical Robotics Market

|

"Reimbursement alignment remains the single most critical enabler for accelerating robotic adoption in community hospital settings. Until payers consistently recognise the downstream savings of robotic-assisted laparoscopic procedures, capital budgeting conversations at the CFO level will remain difficult." |

|

— Dr. James Yoo, President, Society of American Gastrointestinal and Endoscopic Surgeons (SAGES) |

|

(Source: SAGES Annual Meeting, April 2024) |

|

"We've seen surgeon satisfaction scores for robotic-assisted orthopaedic cases consistently outperform conventional instrumented procedures in our network. The data is no longer in question — the challenge is procurement speed and credentialing capacity." |

|

— Chief of Orthopaedics, Mayo Clinic (buyer-side, public conference statement) |

|

(Source: AAOS Annual Meeting, February 2024) |

How Is the Surgical Robotics Market Segmented?

- Robotic systems command the largest share of market revenue, driven by high unit prices and the anchor role they play in multi-year service ecosystems. Laparoscopic surgery remains the dominant application, where robotic-assisted procedures now account for a growing proportion of colorectal, urological, and gynaecological interventions globally. Hospitals are the primary end user, consolidating robotic investment behind flagship surgical programmes that attract specialist surgeons and premium case volumes.

|

This report segments the Surgical Robotics market as follows: |

|

By Product Type: Robotic Systems, Instruments & Accessories, Services |

|

By Application: Laparoscopic Surgery, Orthopedic Surgery, Neurosurgery, Cardiovascular Surgery, Others |

|

By End User: Hospitals, Ambulatory Surgical Centers, Specialty Clinics |

|

By Region: North America, Europe, Asia Pacific, Latin America, The Middle East, Africa |

Which Region Leads the Surgical Robotics Market?

- North America dominates the global Surgical Robotics market, accounting for the largest revenue share in 2025. The U.S. drives this position through high procedure volumes, established reimbursement frameworks for robotic-assisted surgery under Medicare and commercial payers, and the dense concentration of academic medical centres that function as early-adopter anchor accounts for leading OEMs. Canada contributes incremental growth through public health robotics programmes in Ontario and British Columbia.

- Asia Pacific is the fastest-growing region through 2034. China's domestic hospital expansion under the Healthy China 2030 initiative — combined with growing local OEM capabilities from Tinavi Medical and MedBot — is reshaping the regional competitive landscape. Japan and South Korea contribute through aging population dynamics and advanced surgical infrastructure.

- Europe maintains the second-largest revenue position, led by Germany and the U.K. Latin America shows steady adoption across Brazil and Colombia. The Middle East is building robotic surgery capacity in GCC nations, particularly Saudi Arabia and UAE. Africa remains an emerging frontier, with South Africa and Egypt leading initial installation activity.

Report Segmentation & Scope

|

Zion Market Research | Market & Reports — Report Segmentation & Scope |

|

|

Scope Included in the Study |

|

|

By Product Type |

Robotic Systems • Instruments & Accessories • Services |

|

By Application |

Laparoscopic Surgery • Orthopedic Surgery • Neurosurgery • Cardiovascular Surgery • Others |

|

By End User |

Hospitals • Ambulatory Surgical Centers • Specialty Clinics |

|

Regional Analysis |

|

|

North America |

The U.S., Canada, Mexico |

|

Europe |

Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe |

|

Asia Pacific |

China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific |

|

Latin America |

Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America |

|

The Middle East |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

Africa |

South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa |

|

Note: The scope can be further tailored as per your specific requirement. Contact sales@zionmarketresearch.com |

|

**Source: Zion Market Research | Global Surgical Robotics Market Report.

Who Are the Leading Companies in the Surgical Robotics Market?

- Key players operating in the global Surgical Robotics market include Intuitive Surgical, Inc. (U.S.), Stryker Corporation (U.S.), Medtronic plc (Ireland), Zimmer Biomet Holdings (U.S.), Smith & Nephew plc (U.K.), Johnson & Johnson MedTech (U.S.), CMR Surgical (U.K.), Globus Medical (U.S.), Tinavi Medical Technologies (China), MedBot (China), Brainlab AG (Germany), Robocath (France), and Think Surgical (U.S.), among others.

- The market is moderately consolidated at the top, with Intuitive Surgical's da Vinci platform retaining the dominant installed base in soft tissue surgery. Competition is intensifying as second-generation platforms from Medtronic, J&J MedTech, and CMR Surgical offer competitive feature sets at lower price points, while Chinese domestic OEMs are gaining traction in Asia Pacific through government-backed procurement programmes.

What Recent Developments Are Shaping the Surgical Robotics Market?

- January 2025 — Johnson & Johnson MedTech received FDA clearance for an expanded indication of its OTTAVA robotic surgery platform, extending its approved procedural scope to include additional laparoscopic general surgery applications.

- October 2024 — CMR Surgical announced commercial deployment of its Versius robotic system in its 100th hospital globally, with the U.K. NHS becoming its largest single-country anchor client by installed units.

- June 2024 — Stryker Corporation completed its acquisition of Inari Medical, reinforcing its robotic-adjacent vascular intervention portfolio alongside its MAKO orthopaedic robotics business.

|

Date |

Company |

Type |

Description |

Market Impact |

|

Jan 2025 |

J&J MedTech |

Regulatory |

FDA clearance for expanded OTTAVA laparoscopic general surgery indication |

Broadens addressable procedure scope; intensifies competition with da Vinci in general surgery |

|

Oct 2024 |

CMR Surgical |

Commercial |

100th global hospital deployment of Versius system, anchored by NHS adoption |

Validates community hospital and NHS market penetration strategy |

|

Jun 2024 |

Stryker |

Acquisition |

Acquisition of Inari Medical to expand vascular intervention portfolio |

Strengthens robotic-adjacent procedural scope beyond orthopaedics |

|

Apr 2024 |

Intuitive Surgical |

Product Launch |

da Vinci 5 global commercial launch with AI-enhanced visualisation and instrument force feedback |

Raises the technical benchmark across the robotic surgery category |

|

Mar 2024 |

Globus Medical / NuVasive |

Merger |

Integration completed creating the largest dedicated spine robotics portfolio globally |

Creates a dominant spine robotics platform and consolidates competitive pressure on Medtronic spine robotic unit |

|

Nov 2023 |

Medtronic |

Commercial |

Hugo RAS system commercial expansion into Latin American hospital networks |

Establishes Medtronic competitive presence in growth-priority emerging markets |

About Us:

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, the company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is been updated constantly in order to fulfill our clients with prompt and direct online access to our database. Keeping in mind the client’s needs, we have included expert insights on global industries, products, and market trends in this database. Last but not the least, we make it our duty to ensure the success of clients connected to us—after all—if you do well, a little of the light shines on us.

Author:

Mr. Nilesh Patil

Director at Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067