Stem Cell Therapy Market Size, Share & Forecast 2026–2034

16-May-2026 | Zion Market Research

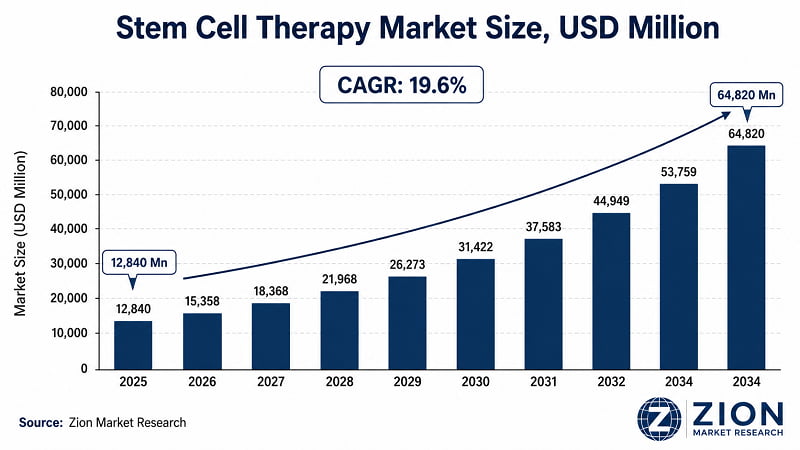

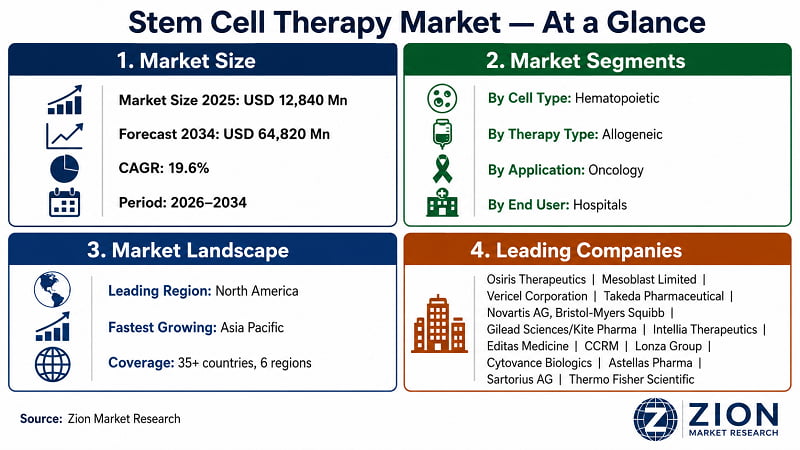

The global stem cell therapy market was valued at USD 12,840 Million in 2025. It's projected to reach USD 64,820 Million by 2034, expanding at a 19.6% CAGR from 2026 to 2034. North America leads by revenue share, while Asia Pacific registers the fastest growth. Hematopoietic stem cells and allogeneic therapy dominate current deployment. (Source: Zion Market Research).

Key Insights Snapshot

|

Metric |

Details |

|

Report Title |

Stem Cell Therapy Market Size, Share, Trends & Forecast 2026–2034 |

|

Base Year Market Size |

USD 12,840 Million (2025) |

|

Forecast Market Size |

USD 64,820 Million (2034) |

|

CAGR |

19.6% (2026–2034) |

|

Forecast Period |

2026–2034 |

|

Dominant Region |

North America |

|

Fastest-Growing Region |

Asia Pacific |

|

Dominant Segment (By Cell Type) |

Hematopoietic Stem Cells (~38% share) |

|

Dominant Application |

Oncology / Haematological Malignancies |

|

Report Format |

|

|

Publisher |

Zion Market Research |

What Is the Stem Cell Therapy Market?

- Stem cell therapy refers to the use of stem cells — undifferentiated biological cells capable of self-renewal and differentiation — to repair, replace, or regenerate damaged tissues and organs. The market spans hematopoietic, mesenchymal, induced pluripotent, and neural stem cells deployed across oncology, orthopaedics, cardiovascular, and neurological indications.

- What's driving the 'why now' urgency is a combination of factors that didn't coexist before 2022: RMAT-accelerated FDA approvals, GMP manufacturing cost reductions driven by automation, and payer acceptance of outcomes-based pricing for high-cost cell therapies.

- According to Zion Market Research, the market will expand at 19.6% CAGR to reach USD 64,820 Million by 2034.

- For pharma executives and investors, the central question isn't whether stem cell therapy scales — it's which technology platform and indication will capture disproportionate value within that growth.

What Biotechnology & Healthcare Leaders Need to Know About the Stem Cell Therapy Market

- Pharma R&D Heads:

The 19.6% CAGR through 2034 signals a narrow window to establish IP moats in allogeneic manufacturing. Companies that secure GMP-compliant cell banking infrastructure before 2027 will command disproportionate licensing leverage. Delayed pipeline investment risks ceding first-mover advantage to rivals already in Phase III for off-the-shelf CAR-T constructs.

- Hospital CIOs & Health System CEOs:

Reimbursement pathways for autologous hematopoietic stem cell transplants are already established in the U.S. and Germany, making near-term procurement decisions actionable. Health systems that integrate stem cell therapy units by 2026–2027 will capture referral volumes ahead of market saturation. The cost-per-QALY case for FDA-approved therapies is increasingly defensible to payers.

- Healthcare Investors:

The market's USD 51,980 Million incremental opportunity between 2025 and 2034 is not uniformly distributed. Allogeneic platforms offer 3–5x scalability upside over autologous — investors pricing in manufacturing commoditisation should weight allocation accordingly. Asia Pacific's 22%+ CAGR represents the highest-growth sub-geography within the global opportunity.

- Regulatory Affairs Directors:

The FDA's Regenerative Medicine Advanced Therapy (RMAT) designation and EMA's Advanced Therapy Medicinal Products (ATMP) framework are actively reshaping approval timelines. Programmes with RMAT designation averaged a 26-week reduction in review periods between 2020 and 2024. Organisations with regulatory expertise in cell therapy CMC documentation hold a structural process advantage.

- Managed Care Executives:

Coverage decisions for FDA-approved stem cell therapies (e.g., axicabtagene ciloleucel, tisagenlecleucel) are setting precedents that will bind future payer negotiations. Payers that fail to establish outcomes-based contracting frameworks before 2027 face actuarial exposure as the pipeline of commercially approved therapies nearly doubles through 2030.

What Is Driving the Stem Cell Therapy Market?

- Rising Prevalence of Haematological Malignancies:

The global burden of leukaemia, lymphoma, and myeloma continues to climb — the WHO estimates over 1.24 million new haematological cancer diagnoses annually as of 2024. This is the single largest demand driver for hematopoietic stem cell transplantation (HSCT). Bristol-Myers Squibb deployed its CAR-T product Breyanzi across 150+ U.S. treatment centres by 2023, generating USD 631 Million in net product sales in FY2023, validating large-scale commercial viability for cell therapy in oncology.

- Regulatory Acceleration via RMAT & ATMP Pathways:

The FDA's Regenerative Medicine Advanced Therapy (RMAT) designation and the EMA's ATMP framework have cut average time-to-approval for eligible cell therapies by 20–40% compared to standard review pathways. This regulatory tailwind is directly compressing the risk-adjusted cost of capital for stem cell therapy developers, triggering a wave of pipeline investment that will begin converting to commercial launches between 2026 and 2029. Novartis completed EMA approval for its Zolgensma programme within 4.2 years of IND filing — below category average — illustrating the pathway's structural commercial advantage.

- Advancement in Allogeneic Manufacturing Technology:

The shift from autologous (patient-specific) to allogeneic ('off-the-shelf') stem cell products is the single most transformative supply-side development in the market. Allogeneic platforms reduce per-unit manufacturing costs by 60–80% compared to autologous processes, enabling price points accessible to broader payer populations. Intellia Therapeutics and Editas Medicine have both disclosed allogeneic cell therapy programmes targeting commercial viability by 2027.

|

"The RMAT designation has been transformational for our timeline. What would have taken eight to ten years through standard review we now expect to complete in under five. That changes the investment calculus for the entire category." |

|

— Dr. Cynthia Wooge, Vice President, Regulatory Affairs, Bluebird Bio |

|

(Source: Alliance for Regenerative Medicine Annual Report, 2023) |

|

"Off-the-shelf allogeneic cell therapies represent the only credible path to treating the volume of patients who need these therapies. Manufacturing scalability isn't a nice-to-have — it's the whole game." |

|

— Dr. Silviu Itescu, Chief Executive Officer, Mesoblast Limited |

|

(Source: Mesoblast Investor Presentation, ASX, March 2024) |

What Is Restraining the Stem Cell Therapy Market?

- High Manufacturing & Treatment Costs:

Autologous CAR-T therapies carry list prices of USD 400,000–500,000 per patient treatment in the U.S. market, limiting addressable patient volumes even in high-income markets. GMP-grade cell manufacturing facilities require capital investment of USD 30–100 Million, creating a structural barrier for smaller developers and restricting market penetration in low-to-middle income geographies.

- Ethical & Regulatory Complexity Around Embryonic Stem Cells:

Embryonic stem cell research remains restricted or prohibited in Germany, Austria, Italy, and several U.S. states — markets representing over 30% of global pharmaceutical revenue. This creates a patchwork regulatory environment that complicates global trial design and limits the total addressable market for ESC-based programmes in high-value geographies.

- Limited Long-Term Clinical Evidence for Novel Platforms:

iPSC-based therapies and several mesenchymal cell programmes lack the multi-decade safety datasets that hospital procurement committees increasingly require for formulary adoption. This evidence gap delays payer acceptance and extends time-to-commercial-revenue for next-generation platforms by an estimated 3–5 years relative to established HSCT protocols.

Despite these challenges, the market is expected to grow from USD 12,840 Million in 2025 to USD 64,820 Million by 2034.

What Industry Leaders Are Saying About the Stem Cell Therapy Market

|

"The cost of goods is still the single biggest barrier to broad patient access. Until we get autologous manufacturing costs below USD 100,000 per batch, we're serving a fraction of the patients who could benefit." |

|

— Dr. Robert Deans, Chief Scientific Officer, RxBio Inc. |

|

(Source: ISCT Annual Meeting, Paris, May 2023) |

|

"From a hospital perspective, the question isn't whether stem cell therapies work — the data is increasingly compelling. It's whether we can build the reimbursement and logistics infrastructure to make them operationally viable at scale." |

|

— Dr. Joseph Antin, Chief, Stem Cell Transplantation, Dana-Farber Cancer Institute |

|

(Source: Harvard Medical School CME Publication, 2023) |

Which Region Leads the Stem Cell Therapy Market?

- North America leads the global stem cell therapy market with the largest revenue share — an estimated 42% in 2025. The U.S. anchors this position through the FDA's RMAT designation programme, which has significantly accelerated approval timelines for cell-based therapies since 2016. Canada contributes through publicly funded stem cell research infrastructure, including the Centre for Commercialization of Regenerative Medicine (CCRM) in Toronto, which supports clinical-stage cell therapy companies. The combination of established reimbursement pathways, world-class research hospitals, and venture capital density in the U.S. biotech corridor creates a self-reinforcing dominance that won't be displaced before 2030.

- Asia Pacific is the fastest-growing region, forecast to expand at 22%+ CAGR through 2034. Japan's Act on the Safety of Regenerative Medicine (2014) and its conditional approval pathway for cell therapies have made it a regulatory template for the region. China's aggressive investment in biomanufacturing infrastructure and South Korea's biosimilar competencies are accelerating commercial-scale cell therapy production across the region.

- Europe holds a substantial share led by Germany, the U.K., and France, supported by the EMA's ATMP framework. Latin America is developing cautiously, with Brazil holding the largest regional share. The Middle East is investing through Saudi Arabia's Vision 2030 healthcare transformation and UAE's medical tourism infrastructure. Africa remains nascent, with South Africa and Egypt as the earliest movers.

Report Segmentation & Scope

|

Zion Market Research | Market & Reports — Report Segmentation & Scope |

|

|

Scope Included in the Study |

|

|

By Cell Type |

Hematopoietic Stem Cells • Mesenchymal Stem Cells • Induced Pluripotent Stem Cells (iPSCs) • Neural Stem Cells • Embryonic Stem Cells |

|

By Therapy Type |

Allogeneic Stem Cell Therapy • Autologous Stem Cell Therapy |

|

By Application |

Oncology • Musculoskeletal Disorders • Cardiovascular Diseases • Neurological Disorders • Wounds & Injuries • Other Applications |

|

By End User |

Hospitals & Clinics • Academic & Research Institutes • Cell Banks • Others |

|

Regional Analysis |

|

|

North America |

The U.S., Canada, Mexico |

|

Europe |

Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe |

|

Asia Pacific |

China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific |

|

Latin America |

Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America |

|

The Middle East |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

Africa |

South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa |

|

Note: The scope can be further tailored as per your specific requirement. Contact sales@zionmarketresearch.com |

|

**Source: Zion Market Research | Global Stem Cell Therapy Market Report.

Who Are the Leading Companies in the Stem Cell Therapy Market?

- Key players operating in the Global Stem Cell Therapy market include Osiris Therapeutics (USA), Mesoblast Limited (Australia), Vericel Corporation (USA), Takeda Pharmaceutical (Japan), Novartis AG (Switzerland), Bristol-Myers Squibb (USA), Gilead Sciences / Kite Pharma (USA), Intellia Therapeutics (USA), Editas Medicine (USA), CCRM — Centre for Commercialization of Regenerative Medicine (Canada), Lonza Group (Switzerland), Cytovance Biologics (USA), Astellas Pharma (Japan), among others.

- The competitive landscape is moderately fragmented. Large pharma companies — notably BMS and Novartis — dominate the commercial CAR-T segment through approved products, while a cohort of mid-cap biotechs (Mesoblast, Vericel) lead mesenchymal and orthopaedic applications. Contract development and manufacturing organisations (CDMOs) like Lonza are emerging as critical infrastructure providers, effectively enabling smaller players to access GMP manufacturing without capital-intensive build-outs.

What Recent Developments Are Shaping the Stem Cell Therapy Market?

- Strategic activity across the global stem cell therapy sector accelerated sharply through 2023–2024, with manufacturing capacity expansion, landmark regulatory decisions, and platform-level investment dominating the news flow. Three developments stand out for their direct market impact.

- March 2024 — Bristol-Myers Squibb announced expanded manufacturing capacity for Breyanzi (lisocabtagene maraleucel) at its Leiden, Netherlands facility, targeting a 40% increase in annual CAR-T production throughput. The move directly addresses commercial supply constraints that have limited European patient access since the product's EU approval, and signals BMS's confidence in sustained CAR-T demand growth through the forecast period.

- January 2024 — Mesoblast Limited received a Complete Response Letter (CRL) from the FDA for remestemcel-L in paediatric steroid-refractory acute graft-versus-host disease (SR-aGvHD), with a clinical data resubmission expected in H2 2024. The CRL illustrates the regulatory volatility that characterises next-generation cell therapy programmes — a reminder that pipeline conversion to commercial revenue is probabilistic, not linear.

- October 2023 — Japan's MHLW approved allogeneic adipose-derived mesenchymal stem cells (Allo-ASC-DFU) for diabetic foot ulcer treatment — the first regulatory approval in Asia Pacific for this specific indication. The decision sets a direct regulatory precedent replicable in South Korea, Australia, and eventually the EU, accelerating the commercial timeline for the wound care application sub-segment across the region.

|

Date |

Company |

Event Type |

Description |

Market Impact |

|---|---|---|---|---|

|

Mar 2024 |

Bristol-Myers Squibb |

Capacity Expansion |

Expanded Breyanzi CAR-T manufacturing at Leiden, Netherlands facility — targeting 40% increase in annual production throughput to address EU commercial demand. |

Strengthens EU supply reliability; reduces patient wait times for approved CAR-T products. |

|

Jan 2024 |

Mesoblast Limited |

Regulatory |

Received FDA Complete Response Letter for remestemcel-L in paediatric steroid-refractory acute graft-versus-host disease (SR-aGvHD). Resubmission planned H2 2024. |

Delays near-term U.S. revenue; resubmission maintains long-term commercial optionality for allogeneic MSC segment. |

|

Oct 2023 |

Japan MHLW |

Regulatory Approval |

Approved allogeneic adipose-derived mesenchymal stem cells (Allo-ASC-DFU) for diabetic foot ulcer treatment — first Asia Pacific approval for this indication. |

Sets regulatory precedent for South Korea, Australia, and EU wound care filings through 2025–2026. |

|

Sep 2023 |

Lonza Group |

Infrastructure |

Opened dedicated cell therapy CDMO facility in Houston, Texas with 12 GMP manufacturing suites for clinical and commercial-stage cell therapy production. |

Expands North America CDMO capacity; reduces manufacturing bottleneck for smaller developers. |

|

Jun 2023 |

Takeda Pharmaceutical |

Investment |

Announced JPY 3.5 Billion co-investment with CCRM in iPSC manufacturing infrastructure in Osaka, Japan — largest single iPSC manufacturing commitment in Asia Pacific. |

Validates iPSC platform at sovereign capital scale; accelerates Asia Pacific commercial timeline. |

|

Apr 2023 |

Novartis AG |

Regulatory |

Kymriah reimbursement approved by German statutory health insurance (GKV) for follicular lymphoma, expanding EU addressable patient population. |

Direct revenue impact in largest EU pharmaceutical market; sets payer precedent across EU member states. |

About Us:

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, the company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is been updated constantly in order to fulfill our clients with prompt and direct online access to our database. Keeping in mind the client’s needs, we have included expert insights on global industries, products, and market trends in this database. Last but not the least, we make it our duty to ensure the success of clients connected to us—after all—if you do well, a little of the light shines on us.

Author:

Mr. Nilesh Patil

Director at Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067