Generative AI in Healthcare Market Size, Share & Forecast 2026–2034

08-May-2026 | Zion Market Research

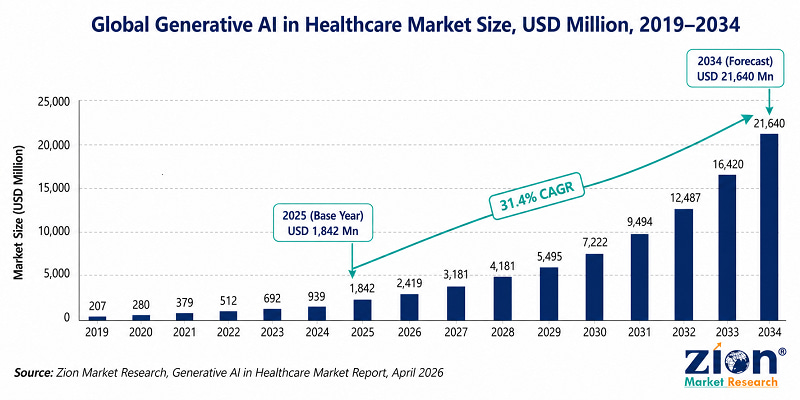

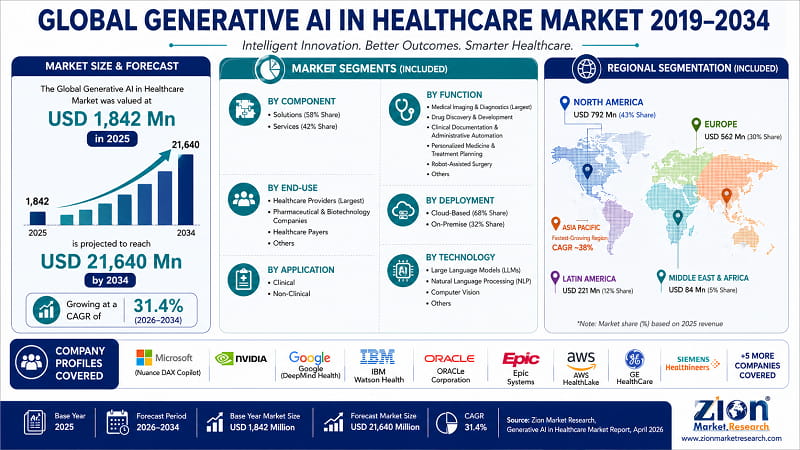

The global Generative AI in Healthcare market was valued at USD 1,842 million in 2025 and is forecast to reach USD 21,640 million by 2034, registering a CAGR of 31.4% from 2026 to 2034. Growth is driven by rising adoption of AI-powered medical imaging, drug discovery acceleration, clinical documentation automation, and mounting physician burnout creating demand for intelligent workflow tools across hospitals, pharma companies, and payers globally.

|

2025 Market Size |

2034 Projection |

CAGR |

Report Coverage |

|

USD 1,842 Million |

USD 21,640 Million |

31.4% |

2026–2034 |

|

Dominant Region |

Fastest-Growing Region |

Leading Segment |

Dominant Deployment |

|

North America (~43%) |

Asia Pacific (~38% CAGR) |

Solutions (~58%) |

Cloud-Based (~68%) |

MARKET OVERVIEW

- The global Generative AI in Healthcare market was valued at USD 1,842 million in 2025 and is forecast to reach USD 21,640 million by 2034, registering a compound annual growth rate (CAGR) of 31.4% over the forecast period 2026–2034, according to Zion Market Research. The absolute dollar growth of USD 19,798 million over nine years — an 11.75x expansion from the 2025 base — makes this one of the highest absolute-value growth trajectories in the global Healthcare IT market.

- Generative artificial intelligence (AI) in healthcare refers to the application of large language models (LLMs), natural language processing (NLP), computer vision, and diffusion-based architectures to clinical and administrative functions across the healthcare value chain. Unlike rule-based clinical decision support systems, generative AI produces new content — diagnostic reports, drug molecule candidates, clinical documentation, patient communication — from learned patterns across electronic health records (EHRs), medical imaging archives, genomic databases, and biomedical literature. This content-generation capability separates generative AI from traditional predictive analytics and from earlier generations of machine learning deployed in healthcare.

- Clinical validation has moved faster than most industry observers expected. AI-powered radiology tools have achieved parity with specialist performance on specific diagnostic tasks, ambient scribing platforms have cleared enterprise deployment thresholds at major health systems, and AI-designed drug candidates have entered Phase II clinical trials. The transition from pilot-stage experimentation to production-scale enterprise deployment — across hospital networks, pharmaceutical R&D organisations, and health insurance operations — defines the current phase of the market. Organisations evaluating AI procurement strategy should also reference ZMR's coverage of the broader Artificial Intelligence in Diagnostics market and the Electronic Health Records market for adjacent context.

Key Insights: Global Generative AI in Healthcare Market

|

METRIC |

VALUE |

|---|---|

|

Report Title |

Generative AI in Healthcare Market By Component (Solutions and Services), By Function (Medical Imaging & Diagnostics, Drug Discovery & Development, Clinical Documentation & Administrative Automation, Personalized Medicine & Treatment Planning, Robot-Assisted Surgery, and Others), By Application (Clinical and Non-Clinical), By End-Use (Healthcare Providers, Pharmaceutical & Biotechnology Companies, Healthcare Payers, and Others), By Deployment (Cloud-Based and On-Premise), By Technology (Large Language Models (LLMs), Natural Language Processing (NLP), Computer Vision, and Others), and By Region — Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2026–2034 |

|

Base Year Market Size |

USD 1,842 Million (2025) |

|

Forecast Market Size |

USD 21,640 Million (2034) |

|

CAGR |

31.4% (Forecast Period: 2026–2034) |

|

Dominant Region |

North America (~43% share) |

|

Fastest-Growing Region |

Asia Pacific |

|

Dominant Component |

Solutions (~58% share) |

|

Dominant Function |

Medical Imaging & Diagnostics |

|

Dominant End-Use |

Healthcare Providers |

|

Dominant Deployment |

Cloud-Based |

|

Report Format |

|

|

Publisher |

Zion Market Research | www.zionmarketresearch.com |

- For healthcare executives, pharma R&D leaders, and investors evaluating AI strategy, the data above represents one of the largest structural investment opportunities in healthcare technology since the EHR adoption wave of 2009–2015.

What Is the Global Generative AI in Healthcare Market?

- Generative artificial intelligence (AI) in healthcare refers to the application of large language models (LLMs), natural language processing (NLP), computer vision, and other generative AI technologies to clinical and administrative functions across the healthcare value chain — including medical imaging analysis, drug discovery and development, clinical documentation automation, personalized treatment planning, robot-assisted surgery, and patient engagement.

- Unlike earlier generations of rule-based clinical decision support tools, generative AI systems learn from vast datasets of electronic health records (EHR), medical literature, imaging archives, and genomic databases to generate new content — diagnostic reports, drug molecule candidates, clinical documentation, patient communication drafts — rather than simply classifying or predicting from existing inputs. This generative capability is what differentiates the technology from traditional AI in healthcare and what drives its accelerating adoption across hospitals, pharmaceutical manufacturers, health insurers, and clinical research organisations globally.

- The global Generative AI in Healthcare market was valued at USD 1,842 million in 2025 and is predicted to reach USD 21,640 million by 2034 at a CAGR of 31.4%. (Source: Zion Market Research, Global Generative AI in Healthcare Market Report, April 2026, https://www.zionmarketresearch.com/

- Healthcare systems, pharmaceutical R&D teams, and health technology investors evaluating AI procurement strategy should note that generative AI adoption in healthcare is no longer experimental — it has cleared clinical validation thresholds in medical imaging, ambient scribing, and drug discovery, and is transitioning into enterprise production deployment across major hospital networks and pharmaceutical corporations globally.

WHAT C-SUITE LEADERS NEED TO KNOW

- Hospital CIOs & Health System CTOs: Organisations that have not initiated an ambient AI scribing evaluation are accumulating a 30–40% clinical documentation productivity gap against early-adopter health systems — a deficit that compounds monthly as enterprise deployments scale. The window for competitive parity is narrowing faster than most technology adoption curves; health systems that delayed EHR adoption in 2010–2012 spent the following five years in catch-up mode. The same dynamic is now playing out with clinical AI.

- Pharmaceutical & Biotech R&D Heads: AI-designed drug candidates have entered Phase II human trials. AI-driven lead identification is documented to reduce preclinical timelines by up to 50% in peer-reviewed studies. Organisations that have not embedded generative AI into their discovery pipeline are accumulating a compounding R&D cost disadvantage — every quarter of delay is a quarter in which AI-native competitors are running more candidates, faster, at lower cost.

- Healthcare Payers & Managed Care Executives: Prior authorisation and utilisation management represent a USD 35 billion annual administrative cost burden in the U.S. alone. AI agents capable of processing authorisations end-to-end — interfacing directly with provider systems — are moving from pilot to production deployment. Payers that standardise on AI-native administrative workflows in 2025–2026 will define the operational cost baseline against which all competitors are measured for the next decade.

- Investors & Board-Level Decision-Makers: Eight healthcare AI unicorns existed as of 2025 — more than any other vertical AI segment, including legal tech, financial services, and enterprise software. Healthcare AI spending reached USD 1.4 billion in 2025, nearly tripling 2024 investment levels (Source: Menlo Ventures, 2025 State of Generative AI in the Enterprise). One in four dollars invested in healthcare now flows to AI-enabled companies (Source: Silicon Valley Bank, 2025 Healthcare Investments & Exits Report). The institutional capital conviction is no longer speculative — it is deployment-stage.

- Asia Pacific Strategy & Regional Expansion Teams: Asia Pacific is the fastest-growing region at a 38% CAGR — outpacing North America, Europe, and every other region by a significant margin. China's national AI in healthcare guidelines mandate universal AI-enabled diagnostic assistance in primary care institutions by 2030. Japan, India, and South Korea are deploying government-funded AI hospital infrastructure at institutional scale. Organisations without a formalised Asia Pacific AI strategy are not maintaining a neutral position — they are actively ceding first-mover advantage to regionally committed competitors.

KEY MARKET DRIVERS

- Driver 1: The Physician Burnout Crisis Is the Immediate Commercial Engine

The administrative burden on clinicians has reached a systemic breaking point — and market data confirms that generative AI adoption is accelerating in direct response. According to the Medscape 2024 Physician Burnout & Depression Report, 49% of U.S. physicians reported burnout, with 62% identifying administrative tasks and documentation requirements as the primary cause. Physicians spend approximately one hour on clinical documentation for every five hours of patient care — a ratio that has driven what healthcare operations professionals call 'pajama time': evenings spent completing records rather than recovering from clinical workloads.

Ambient AI scribing — generative AI systems that listen to physician-patient conversations and automatically generate structured clinical notes in EHR format — is the direct market response. Tools in this category generated approximately USD 600 million in U.S. revenue in 2025, growing at 2.4x year-on-year (Source: Zion Market Research, Global Generative AI in Healthcare Market Report, May 2026). Hospitals deploying ambient scribing at enterprise scale have reported 30–40% reductions in clinical documentation time within 90 days of full rollout.

"The documentation burden on our physicians is not a workflow inconvenience — it is a patient safety issue and a talent retention crisis. Tools that give clinicians back even 30 minutes per day have an immediate, measurable impact on physician satisfaction scores and, by extension, on care quality."

— Dr. David Rhew, Chief Medical Officer, Microsoft

- Driver 2: Clinically Validated Performance in Medical Imaging and Drug Discovery

Generative AI has crossed the clinical validation threshold in two high-value healthcare functions — and those clearances are driving enterprise procurement decisions that would have been impossible two years ago. In medical imaging and diagnostics, FDA-cleared AI tools from Aidoc, Viz.ai, iCAD, and Paige AI now match or exceed specialist performance in detecting pulmonary embolism in CT scans, identifying diabetic retinopathy in fundus images, and flagging suspicious lesions in mammography — reducing false negative rates and report turnaround times by 40–60% in controlled hospital deployments. The clinical evidence base underpinning these clearances is now robust enough to satisfy hospital medical committees and commercial insurance reimbursement requirements.

In drug discovery and development, Insilico Medicine's AI-designed drug candidate INS018_055 for idiopathic pulmonary fibrosis reached Phase II clinical trials in 2024, establishing the first institutional validation of a complete generative AI drug discovery pipeline. Eli Lilly's partnership with OpenAI for antimicrobial drug discovery and AstraZeneca's investment in generative AI molecular design confirm that major pharmaceutical organisations have moved beyond R&D pilots into strategic commitment. AI-driven drug design is documented to reduce time-to-candidate by up to 50% in peer-reviewed studies (Source: Nature Reviews Drug Discovery, 2024).

"Generative AI is transforming drug discovery by allowing us to build sophisticated models and seamlessly integrate AI into the antibody design process. What previously took years in the laboratory can now be compressed into months using AI-generated molecular candidates."

— David M. Reese, Executive Vice President & Chief Technology Officer, Amgen

- Driver 3: Unprecedented Capital Deployment and Healthcare AI Infrastructure Maturation

The investment environment supporting generative AI in healthcare in 2025 is structurally different from the speculative healthcare AI investments of 2018–2021. Healthcare AI spending reached USD 1.4 billion in 2025 — nearly tripling 2024 investment levels — and according to Silicon Valley Bank's 2025 Healthcare Investments & Exits report, one in four dollars invested in healthcare now flows to AI-enabled companies. Eight healthcare AI unicorns existed as of 2025, more than any other vertical AI segment globally.

The infrastructure deficit that constrained earlier AI deployments — HIPAA-compliant cloud architecture, pre-integrated EHR connectivity, and purpose-built clinical language models — has been resolved at commercial scale. AWS HealthLake, Microsoft Azure Health Data Services, and Google Cloud Healthcare API now provide validated HIPAA-compliant AI infrastructure that reduces healthcare organisations' deployment complexity from 18-month integration projects to 90-day enterprise rollouts. NVIDIA's BioNeMo, Google's Med-PaLM 2, and Microsoft's BiomedCLIP provide clinical foundation models that reduce the fine-tuning investment required to achieve production-ready accuracy thresholds in specific specialties.

""Two years ago, we had about 160 applications. Now we have about 230 AI applications that are live. We're probably generating north of $100 million in annual savings using AI and RPA tools in a number of different areas."

— Daniel Barchi, Senior Executive Vice President & CIO, CommonSpirit Health (Source: Becker's Hospital Review, September 2025)

KEY MARKET RESTRAINTS

- Restraint 1: Regulatory Validation Burden for Clinical AI

The regulatory pathway for generative AI in clinical applications remains the most complex technology approval process in any industry. The FDA's AI/ML-based Software as a Medical Device (SaMD) framework requires 510(k) clearance or De Novo classification for novel AI functions — processes that average 12–24 months. As of 2024, the FDA had cleared over 950 AI/ML-enabled medical devices, but the volume of submissions has grown faster than review capacity, creating deployment lag between demonstrated AI capability and commercial availability.

The EU AI Act, effective August 2024, classifies healthcare AI systems as high-risk under Annex III, imposing conformity assessment obligations, mandatory explainability documentation, and post-market monitoring requirements estimated to cost USD 50,000–500,000 per AI system per market. For AI startups targeting European health systems, this compliance cost creates a market entry barrier that systematically favours large, well-capitalised incumbents over specialist innovators.

- Restraint 2: Healthcare Data Privacy Regulations and AI Training Constraints

Generative AI systems require access to large volumes of structured patient data for training and inference — and this creates direct tension with the most comprehensive data privacy regulatory framework of any industry. In the U.S., HIPAA's minimum necessary standard and de-identification requirements constrain the use of protected health information (PHI) in AI training pipelines. Health systems that have attempted to build proprietary training datasets from patient populations have faced Institutional Review Board scrutiny and patient advocacy challenges that delay timelines by 12–18 months.

In Europe, GDPR Article 9's special category protections for health data — combined with national supervisory authority enforcement actions including the French CNIL's EUR 1.5 million fine of Doctissimo in 2023 for health data processing violations — have created a climate of regulatory risk aversion that extends AI vendor contracting timelines by 6–9 months in enterprise hospital procurement processes.

How Is the Global Generative AI in Healthcare Market Segmented?

- The global generative AI in healthcare market is segmented by component, function, application, end-use, deployment mode, and technology — with the solutions component, medical imaging and diagnostics function, and healthcare providers end-use segment each commanding the largest revenue shares globally.

- The solutions segment accounts for approximately 58% of total market revenue in 2025, driven by healthcare providers' preference for end-to-end AI platforms that integrate with existing EHR systems and clinical workflows rather than point-service implementations.

- Medical imaging and diagnostics is the leading functional segment — AI systems that analyse radiology, pathology, and cardiology images are among the most clinically validated and commercially deployed generative AI applications in healthcare today.

- Cloud-based deployment dominates at approximately 68% of market share, reflecting healthcare organisations' shift toward scalable, infrastructure-light AI delivery models that avoid the capital expenditure of on-premises deployment.

Component Insights: Solutions Segment Dominates at 58% Revenue Share

- The solutions segment accounted for approximately 58% of total market revenue in 2025, driven by healthcare providers' preference for end-to-end AI platforms with native electronic health record integration over point solutions that require custom API development. The services segment is growing at the fastest rate within the component category, as the complexity of AI deployment — regulatory compliance documentation, EHR integration validation, clinician training, and ongoing model monitoring — has created strong demand for implementation and managed services from both incumbent healthcare IT vendors and specialist AI deployment firms.

Function Insights: Medical Imaging Leads, Clinical Documentation Is the Fastest-Growing

- Medical imaging and diagnostics is the leading functional segment, with the highest commercial deployment rate of any generative AI application in clinical settings. AI radiology tools reducing report turnaround times by 40–60% have crossed the reimbursement validation threshold required for hospital procurement approval. The AI in Medical Imaging market represents the most commercially mature sub-segment of generative AI in healthcare.

- Clinical documentation and administrative automation is the fastest-growing functional segment, driven by the physician burnout crisis and the measurable ROI of ambient AI scribing. This function generated approximately USD 600 million in U.S. revenue in 2025, growing at 2.4x year-on-year — the highest growth rate of any defined functional segment.

- Drug discovery and development is the segment generating the highest institutional R&D investment. The Drug Discovery Informatics market and the broader AI in Drug Discovery market provide additional segmentation context for pharmaceutical and biotech organisations assessing AI-driven pipeline strategy.

Which Region Leads the Global Generative AI in Healthcare Market?

- North America held approximately 43% of global market revenue in 2025. The U.S. healthcare system's combination of near-universal EHR adoption (exceeding 96% among hospitals), digitised clinical data repositories, and the deepest concentration of healthcare AI vendors globally positions it as the world's primary generative AI in healthcare deployment environment. Ambient scribing alone generated approximately USD 600 million in U.S. revenue in 2025.

- Europe is the second-largest region, led by Germany, the U.K., and France, where AI integration in hospital administration, radiology, and drug discovery is accelerating under digital health strategies.

- Asia Pacific is the fastest-growing region at a 38% CAGR. China's August 2025 national AI in healthcare guidelines target universal AI-enabled diagnostic and treatment assistance in all primary care institutions by 2030. India's AIIMS system deployed an AI platform trained on 500,000 radiological and histopathological images in February 2024, targeting diagnostics in underserved rural healthcare settings where specialist physician access is severely limited. Japan, South Korea, and Australia are recording government-mandated AI healthcare infrastructure investment at institutional scale.

|

REGION |

2025 SHARE |

CAGR |

KEY COUNTRIES |

PRIMARY DRIVER |

|---|---|---|---|---|

|

North America |

~43% |

~29% |

The U.S., Canada |

Advanced EHR infrastructure, AI unicorn ecosystem, physician burnout crisis |

|

Europe |

~26% |

~28% |

Germany, U.K., France, Netherlands |

EU AI Act compliance wave, hospital digitalisation mandates |

|

Asia Pacific |

~20% |

~38% |

China, Japan, India, South Korea |

Govt AI investment, healthcare system digitalisation, imaging demand |

|

Latin America |

~5% |

~30% |

Brazil, Argentina, Colombia |

Telemedicine growth, pharma R&D expansion |

|

The Middle East |

~4% |

~33% |

GCC, Israel, Turkey |

Vision 2030 digital health, AI hospital pilots in UAE, Saudi Arabia |

|

Africa |

~2% |

~29% |

South Africa, Egypt, Nigeria |

Digital health infrastructure investment, telemedicine adoption |

WHAT HEALTHCARE LEADERS ARE SAYING

"Ambient AI documentation is not an incremental improvement to physician workflows — it is a structural reset. The health systems that deploy at enterprise scale in 2025 and 2026 will set the documentation efficiency baseline that defines competitive positioning for the next decade."

— Dr. Shiv Rao, Co-Founder & CEO, Abridge AI

"We are at an inflection point where AI in healthcare has moved from a research narrative to a procurement decision. The organisations that treat this as a technology experiment rather than a strategic capability investment will face a compounding disadvantage as clinical AI becomes the operational standard."

— Dr. Greg Moore, Chief Medical Officer, NVIDIA

"The integration of generative AI into clinical workflows at enterprise scale is no longer a question of whether — it is a question of which platforms, which vendors, and which deployment timelines. Health system executives who defer this decision by 12 to 18 months are not maintaining neutrality; they are making a choice to fall behind."

— Jim Rogers, CEO, Digital Pathology Division, Mayo Clinic

"If you don't have this technology, people on the front lines may not want to come to your facility."

— Amy Meister, Senior Vice President, UPMC & President, Community and Ambulatory Services (Source: Healthcare Dive, HLTH 2025 Conference, October 2025)

Report Segmentation & Scope:

|

Zion Market Research | Market & Reports Customized Research Scope Overview |

||||||||||||||||

Note: The scope can be further tailored as per your specific requirement. |

||||||||||||||||

Who Are the Leading Companies in the Global Generative AI in Healthcare Market?

- Key players operating in the global Generative AI in Healthcare market include Microsoft Corporation (USA), NVIDIA Corporation (USA), Google LLC — DeepMind Health (USA), IBM Corporation — Watson Health (USA), Oracle Corporation (USA), Epic Systems Corporation (USA), Amazon Web Services — AWS HealthLake (USA), Nuance Communications — DAX Copilot (USA), GE HealthCare Technologies (USA), Siemens Healthineers AG (Germany), Insilico Medicine (Hong Kong / USA), Abridge AI Inc. (USA), Tempus AI Inc. (USA), Recursion Pharmaceuticals Inc. (USA), Hippocratic AI Inc. (USA), among others.

- The competitive landscape is highly dynamic and spans three distinct player types: large technology platforms (Microsoft, Google, NVIDIA, Oracle, AWS) that provide foundational infrastructure and LLM capabilities; healthcare IT specialists (Epic Systems, Nuance, GE HealthCare, Siemens Healthineers) that integrate generative AI into clinical workflow platforms; and AI-native healthcare startups (Abridge, Tempus AI, Insilico Medicine, Hippocratic AI, Recursion Pharmaceuticals) that build vertical AI applications for specific clinical functions. The boundaries between these categories are collapsing rapidly through acquisition and partnership

What Recent Developments Are Shaping the Generative AI in Healthcare Market?

|

DATE |

COMPANY |

DEVELOPMENT |

IMPACT |

|---|---|---|---|

|

Jan 2025 |

NVIDIA |

Partnered with IQVIA, Illumina, Mayo Clinic, and Arc Institute to advance drug discovery, genomic research, and agentic AI in healthcare |

Positions NVIDIA as foundational infrastructure for pharma AI at institutional scale |

|

Jan 2025 |

Rad AI |

Raised USD 60 million Series C at USD 525 million valuation to expand generative AI radiology solutions for U.S. radiologists |

Signals strong investor conviction in clinical AI; expands imaging AI adoption |

|

Nov 2024 |

Royal Philips |

Expanded strategic collaboration with AWS to advance HealthSuite cloud services and power generative AI across radiology, pathology, and cardiology |

Accelerates cloud-native clinical AI deployment across Philips' global customer base |

|

Oct 2024 |

Hippocratic AI |

Raised USD 137 million from NVIDIA's NVentures to develop generative AI healthcare agents with long-context conversational capabilities |

Establishes Hippocratic AI as a leading patient engagement and care navigation AI platform |

|

Jun 2024 |

Cognizant + Google Cloud |

Launched healthcare-specific LLM solutions integrating Vertex AI and Gemini models to redesign healthcare administrative processes |

Brings enterprise-grade generative AI to mid-market healthcare administrative workflows |

About Us:

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, the company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is been updated constantly in order to fulfill our clients with prompt and direct online access to our database. Keeping in mind the client’s needs, we have included expert insights on global industries, products, and market trends in this database. Last but not the least, we make it our duty to ensure the success of clients connected to us—after all—if you do well, a little of the light shines on us.

Author:

Mr. Nilesh Patil

Director at Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067

Email- sales@zionmarketresearch.com